World markets have recently staged significant gyrations as Fed rate hikes draw ever closer. From 1/30/15-7/31/15, for example, rate sensitive sectors, such as 30-year Treasuries lost 10%, MLPs lost 7%, and REITs lost 6%.

What’s going on? Nearly 7 years of cheap money, consequence of a Fed Funds rate stagnating below 0.25%, has inflated the value of many asset classes. Higher rates—especially if they rise quickly—could therefore “pop the balloon”. How can advisors astutely position their client portfolios today for a rising rate environment not seen since 2006? What investment products can advisors purchase that haven’t seen their value inflated? Are there any bargains in the markets? Are there any assets that are likely to make attractive cash distributions even if interest rates spike higher?

It turns out there may be a single answer to all these questions, buried right in the NYSE, under several layers of go-go growth stocks and internet IPOs: closed-end funds (“CEFs”).

Although CEFs have been around for over 100 years, only a few investors are familiar with them, in part because they are so incredibly boring. After all, they are just mutual funds trading like a stock. There are about 600 US CEFs—some invest in bonds, some in US or foreign stocks. Most CEFs pay regular cash distributions (monthly or quarterly), currently averaging just over 7%.

What makes CEFs unique? Unlike other funds (like ETFs or open-end funds), a CEF can often be purchased for less than it is worth. Every day, CEFs calculate and publish a number called “Net Asset Value” [NAV], which represents the market value of their portfolios. However, it is the market that sets a CEF trading price, and most of the time, CEFs trade for less than that published NAV, due in part to the fact that assets in the CEF are “captive”---investors have no mechanism to demand their investment back at NAV.

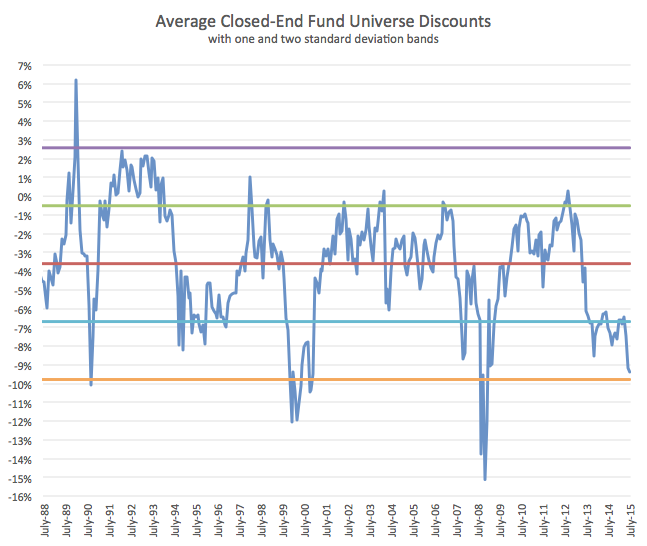

What’s happening with CEFs today? There is an attractive Bargain Basement sale in progress. Historically, the average CEF usually trades at $.96-.97 per dollar of assets (see chart). Today, instead, the average CEF trades at only $.90 per dollar of assets. This has only happened three other times during the past 30 years.

Why is this happening and why should an advisor care about it? The most likely cause of today’s bargains is the same interest rate fear that is causing investors to sell other rate-sensitive sectors. Advisors should realize that when buying highly discounted closed-end funds today they enjoy two distinctive bargains: one on the underlying rate-sensitive asset classes (the holdings within the CEF) and the other on the CEF’s trading price relative to its NAV.

An example should help clarify. There are 12 CEFs that Morningstar includes into the “World Bond” category. These, on average, trade today at only $.86 per $1 of assets—a 14% discount. The same funds, over the past three years, have traded at an average $.92 per $1 of assets—an 8% discount. These funds also make monthly or quarterly cash distributions, which annualize at 9.7% on their depressed trading price. Suppose an investor buys a CEF at $.86 and that its NAV over the next year doesn’t appreciate while it continues to make cash distributions and reverts back to its more normal 8% discounts. That investor might make $.08 in cash distributions, plus $.06 on discount reduction, for a total return of $.14 on the original $.86 investment—more than a 16% return.

Average Closed-End Fund Universe Discounts

Would this be a reasonable expectation? The chart helps validate that this kind of discount reduction, starting from elevated discounts, is actually quite normal, historically. The reason for this is that multiple factors—including the threat that an investor group could buy up enough shares to force a CEF to liquidate or open-end, thereby eliminating the discount instantly—work against the continuation of extreme discounts. In fact, based on our research going back to 1988, prior instances when the CEF universe traded at more than an 8% discount were followed by 12-month returns of +18.5% for the average CEF, and +26.1% for highly discounted CEFs (those in the most discounted quintile of the universe). By comparison, the 12-month total return of the S&P 500 for those same time periods averaged only +1.3%. Ergo, purchasing CEFs at big discounts has been an excellent idea historically.

There is more to it. What about interest rates? Those historical “discount opportunities” may not have immediately preceded the kind of interest rate spike advisors fear today. Leaving discounts aside for a moment, how have CEFs performed in rising-rate environments?

To answer this question we might examine the last series of Fed Funds rate increases, from 1.03% on 6/30/04 to 5.24% on 7/31/06. How did CEFs do then? Really well. In fact, the average CEF returned +27% for that 2-year period, while highly discounted CEFs returned +50%, against the S&P 500 +16% and bonds +7%.

We should dig deeper, of course, since those two years may not be typical. Back to 1988, restricting our attention only to those rolling one-year periods where Fed Funds rose by at least 0.5%, and CEF discounts began at a level greater than 3%, we find:

Investing in CEFs produced:

- An average one-year return of +10.7%.

- Losses about 8% of the time.

Investing only in discounted CEFs gave:

- An average one-year return of +14.7%

- Losses about 6% of the time

Investing only in highly discounted (in the widest quintile of discounts) CEFs gave:

- An average one-year return of +24.4%

- No losses

To summarize, historically, even during periods of rising rates, investing in highly discounted closed-end funds has been a very intelligent move. Even advisors who correctly forecast an increase in interest rates might achieve excellent returns for their clients by shopping at the CEF Bargain Basement sale.

Eric Boughton, CFA, is Portfolio Manager and Chief Research Analyst for Deschutes Portfolio Strategies, and manages the Matisse Discounted Closed-End Fund Strategy (MDCEX), as well as separately managed closed-end fund accounts.

{kind=link}