In April the central bank of Cyprus announced it would sell off three-quarters of its gold reserves, some 10 metric tons, to fund the bailout of its financial system. That’s the largest bullion sale by a eurozone nation since France sold 17 metric tons in 2009.

Not surprisingly, gold investors were rattled by the Cypriot declaration and ominous remarks made by European Central Bank president Mario Draghi shook them even more. Holders of gold assets, worried about the potential for copycat sales by other debt-plagued countries such as Italy, Portugal, Spain and Greece, sent gold prices into a liquidation tailspin.

Up until then, central banks were more inclined to buy metal rather than sell it. The dedication of state reserves to bullion had kept a bid under the gold price. No wonder the Cyprus news was deemed bearish.

Overlay on this some feeble job growth, a downward move in the ISM Purchasing Managers Index and a significant drop in the wholesale inflation rate and some are fearing the specter of deflation.

Over the past decade, a plethora of exchange-traded products (ETPs) have been floated offering investors inflation hedges. Nearly two dozen funds and notes tied to inflation-protected securities alone have been launched since 2003 and more are on the way.

But funds providing portfolio protection against the ravages of deflation is smaller and not well understood. Given the recent sell-off, it’s worth taking a look at funds that can help investors circumnavigate the shoals of a disinflationary economy.

Playing the deflation game

We’ll start with the the one actually branded with the word “deflation.” The PowerShares DB US Deflation ETNs (NYSE Arca: DEFL). The fund is made ofsenior unsecured obligations issued by A+ rated Deutsche Bank AG and are based on the DBIQ Duration-Adjusted Deflation Index. The index tracks changes in market expectations of future inflation implied by the spread between Treasury Inflation-Protected Securities (TIPS) and U.S. Treasury bonds.

Unlike fixed-coupon Treasuries, TIPS offer investors a variable return tied to the Consumer Price Index (CPI). Interest is paid semi-annually in the same manner as conventional paper, but the TIPS principal value adjusts up and down based on the inflation metric. Thus, an investor’s actual yield is based on the TIPS’s adjusted principal.

When inflation is held in check, the TIPS return can be expressed negatively. At the end of March, for example, ten-year TIPS were priced at a discount to the prevailing inflation rate.

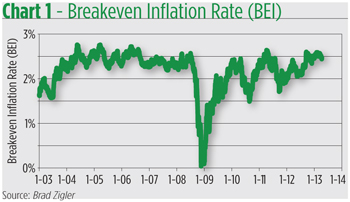

One way to gauge the relative worth of TIPS is to calculate the “breakeven inflation rate” (BEI). BEI is the spread between a TIPS yield and that of a Treasury note with a similar maturity. When inflation lingers above the BEI, TIPS are likely to outperform conventional T-notes, but when the CPI trends below BEI, traditional Treasuries will better TIPS.

BEI can be easily gamed by sophisticated traders. To play on an expectation of disinflation or deflation, for example, one could sell TIPS short against a long position in conventional Treasury bonds. The index driving DEFL’s value simulates this very trade by notionally selling TIPS and buying Treasury futures across the maturity spectrum.

BEI declines when Treasury yields decrease (and prices, as a consequence, increase) relative to the yield on TIPS. An exemplar is the market crash of 2008. In early July, ten-year Treasuries were offered at 3.99 percent while TIPS with a similar maturity yielded 1.42 percent, resulting in a BEI of 2.57 percent. By November, T-note rates had slipped to 3.20 percent and TIPS were at 3.15 percent. Thus the BEI came in more than 250 basis points (to 0.05 percent) as the U.S. economy scraped bottom following a deflationary nosedive (see Chart 1).

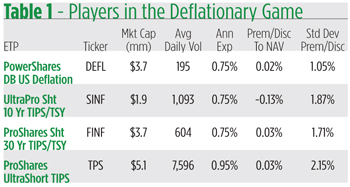

Unfortunately, DEFL wasn’t available as a hedge in 2008. The notes were floated late in 2011, well after BEI rebounded to the two percent level. Then a couple of ETFs, also designed to play BEI from the short side, debuted (see Table 1).

The ProShares UltraPro Short 10 Year TIPS/TSY Spread (NYSE Arca: SINF), launched in February 2012, is designed to provide owners with three times the inverse daily performance of the Dow Jones Credit Suisse 10-Year Inflation Breakeven Index. The index mirrors the performance of long positions in the most recently issued ten-year TIPS and duration-adjusted short positions in Treasury notes of similar maturity. Rather than using actual TIPS and bond futures, SINF obtains its exposures through swaps issued by money center banks such as Citibank and Credit Suisse.

Further upthe maturity ladder (and the duration risk spectrum), theProShares Short 30 Year TIPS/TSY Spread (NYSE Arca: FINF) tracks the inverse daily performance of the Dow Jones Credit Suisse 30-Year Inflation Breakeven Index. Like SINF, proxies for the most recently issued on-the-run 30-year TIPS and Treasury bonds populate the underlying portfolio.

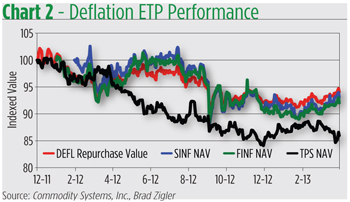

If you’re scratching your head wondering why the fund playing the ten-year spread is levered 3-to-1 while the 30-year product is not geared, it’s because of the difference in duration risk between the maturity buckets. Longer-dated paper is much more sensitive to interest rate risk. Cranking up the exposure of the ten-year spread allows it to deliver the same bang for the buck as the fund based on the trade in 30-year bonds (see Chart 2).

Spreads not required

Some investors might wonder why they should bet on deflation through a two-legged trade when they can just short TIPS themselves. For those who want to keep things simple, there’s the ProShares UltraShort TIPS (NYSE Arca: TPS) which attempts to provide two times the inverse daily performance of the Barclays U.S. Treasury Inflation Protected Securities Index.

Index constituents include all publicly issued TIPS with at least one year remaining maturity and more than $250 million par value outstanding. The index is weighted by relative market value.

As with the other ProShares products, TPS’s index exposure is obtained through swaps rather than physical replication.

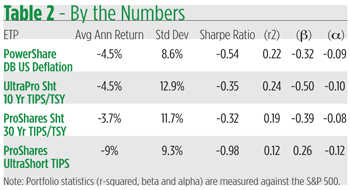

Investors should know about the costs of using TPS in lieu of the spread products. First, TPS is more expensive. Its annual expense ratio is 95 basis points, 20 bips more than the other ETPs. Then there’s the performance cost. Since inception, TPS’s value has eroded at a nine percent annual clip, double the loss sustained by the spread products. Is it then more likely that TPS will outperform to the upside in a deflationary environment? Given the fund’s relatively low standard deviation, it doesn’t seem likely.

The spread products, in fact, appear to be bottoming off a base established in February (see Chart 2). TPS hasn’t yet signaled an end to its downtrend.

No matter what product you consider, one thing is clear. They’ve all been, to date, very lightly traded. As a group, their average daily volume barely amounts to 2,400 shares, with most of the business flowing to TPS. The light volume, no doubt, contributes to some wide discounts and premiums to the ETPs’ repurchase or net asset values. While the discount/premium for each product seems relatively mild (SINF is the worst with a median discount of 13 basis points) the day-to-day range can be quite wide. DEFL’s benign two-bip premium belies the fact that the closing price has skewed as much as 3.4 percent on either side of the ETN’s daily repurchase value. You get a better sense of these premiums and discounts by keeping an eye on their standard deviations. By this measure, the widest variance is found in TPS pricing.

Overall these funds seem to have built a base and are poised to deliver some degree of hedge protection if the expectations of deflation rise. Whether or not an allocation to a deflation hedge is justified is, of course, a very personal decision based upon the sensitivity of one’s portfolio and the deflationary outlook. For these investors, it may be enough to know that the hedges are available if needed.