By Michael Kelly

How often do you feel overwhelmed by ever-growing investment choices? Market sentiment constantly changes based on global events, requiring more time to sift through an endless barrage of information to make educated decisions. Investors often look to their advisors to navigate this complexity and hope the best choices become obvious. We all want higher returns, and we would love to achieve those returns while taking less risk. But, when making investments decisions, there can be an opportunity cost – the cost of a missed opportunity, what you might have achieved if you had invested differently. Investors need to reflect on the most critical goals and outcomes they are looking to achieve.

Our experience indicates that many investors are looking for more income. Every day we face the reality of disappearing income returns when we check our bank deposit statements or observe global bond yields or money market funds. At the same time, we read stories about how we’re expected to live much longer than our parents and grandparents. That’s great news. Yet, it begs the question, how do we pay for it?

As any retiree will tell you, there is no substitute for a predictable monthly influx of cash. However, the average American retires today with only $16,000 of annual Social Security benefits.[1] That is daunting, especially if we expect to live 10, 20, or even 30 years in retirement. It places a premium on a critical element of any well-constructed investment portfolio: income. Income has long been a leading driver of historic portfolio returns. But given the low level of yields today, that driver is virtually disappearing. Consider the fascinating impact of coupon or dividend income on portfolio returns over the past 30 years.

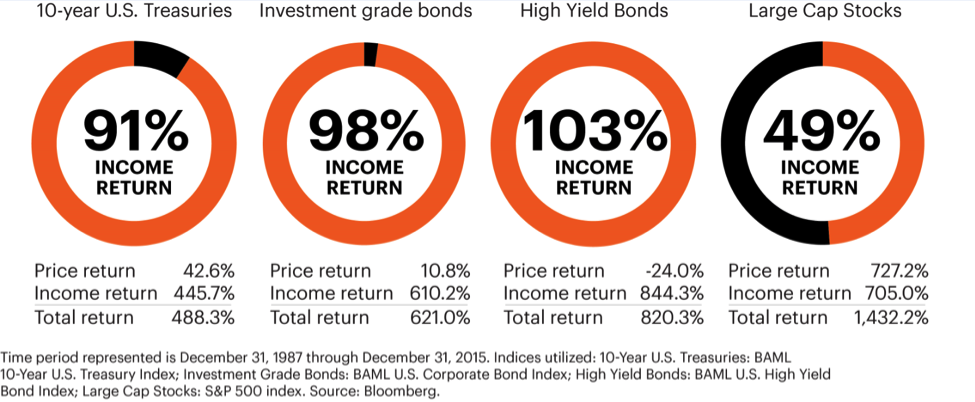

Percentage of total return derived by income

As this graphic shows, the coupon income of a traditional government or corporate bond represents 90% to 100% of its historical total return. Perhaps more surprisingly, the reinvested dividend income of the S&P 500 has represented almost half of that index’s historical total return. What can we take away from this example? Income is key.

A simple way to illustrate how various investment yields can affect an investment over the long term involves something called the rule of 72. The rule of 72 is a calculation used to estimate the number of years it would take to double your money at an expected annual rate of return. You divide 72 by the rate, expressed as a percentage, to estimate the number of years. For example, at a compound annual return of 8%, it would take 9 years to double your money (72 / 8 = 9).

The rule of 72 can be applied to determine the effectiveness of reinvesting income to achieve better portfolio outcomes. Let’s compare yields available for various sources of investment income in the market today and calculate how long at those compounded yields it would take to double the size of an investment.

Yields and time to double by investment category:

Clearly, we can appreciate why, when asked to name the greatest invention in human history, Albert Einstein replied simply, “compound interest.”

In addition to the compounding power of income investing on a portfolio’s return, the income derived from fixed income investments has historically been far less volatile and more predictable as a source of total return than growth derived from equity-oriented investments. And greater predictability means greater reliability for an investor’s future.[2]

In today’s rapidly disappearing yield environment, the hunt for income is on. As you search the market landscape for sources of income, you will likely find different options presenting varied risk and reward profiles. Depending on your personal financial goals, one or more may fit your needs.

It’s important to keep these considerations in mind when considering your income options.

- Consider your time horizon. Yields on longer-duration fixed income investments are typically higher than short-term investments. How comfortable are you in locking up your investment capital to receive higher potential yields and an “illiquidity premium”?

- Determine your tolerance for credit risk. Credit risk entails the likelihood your investment will be paid back in income and principal. The more credit risk you are willing to bear, the higher your potential return. But, with that higher potential return comes the trade-off of higher risk.

- Decide how much interest rate risk you want to take. Depending on the security, fixed income investment returns may fluctuate with the future path of interest rates. How comfortable are you in betting on the future direction of interest rates (both short term and long term)? The answer may help guide your investment decision.

For more on the challenges of finding income in today’s economy, read our commentary, “Iceberg, right ahead!” Also, visit our spectrum of alternatives to learn more about the benefits and objectives of various allocations.

Michael Kelly is Executive Vice President, Chief Investment Officer, FS Investments

[1] Source: Center on Budget and Policy Priorities and The Social Security Administration as of June 2016

[2] Source: Bloomberg. Compared the volatility of returns (measured by standard deviation) of the S&P 500 Index trailing 12 month dividend and earnings growth to the Bank of America Merrill Lynch U.S High Yield Index income return. Data was calculated for the period December 31, 1996 through December 31, 2015.

This article originally appeared on FS Investments' Perspectives blog.