A December 2013 study by Goldman Sachs predicted that the growth in the liquid alternative space would mimic the ETF market, soaring to $2.4 trillion in assets by 2020. (Assets are currently at about $222 billion, according to Morningstar.)

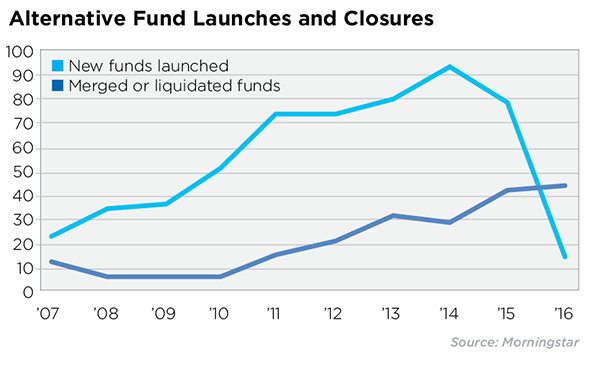

Goldman’s prediction was just one data point spurring a streak of new alternative mutual funds; indeed 2014 saw the highest number of new funds launched in the category, at 93, according to Morningstar data.

But that was two years ago—and while the number of new funds has dropped dramatically, closures and mergers are fast on the rise. Observers say the market became too saturated; many funds failed to deliver on performance; and money managers are finding that it’s difficult to distribute these products on the platforms of the big investment advisory firms.

In 2015, 42 funds were merged or liquidated, according to Morningstar. That number has already been surpassed in the first half of this year, where 43 funds have closed or been folded into others. That compares to 29 funds in 2014.

“It’s kind of like real estate—overbuilding, oversupply,” said Josh Charlson, director of manager research, alternative strategies at Morningstar. “And I think we’re seeing a little bit of the aftereffects of that. A lot of fund companies developed products or translated institutional or hedge fund products to the liquid alts space hoping they would pick up assets like some of the most successful funds have done. But it’s not so easy to do that and it’s pretty competitive.”

Several managers that jumped on the liquid alts bandwagon, then quickly jumped off, include hedge fund firm Whitebox Advisors, Pioneer Investments, Virtus Investment Partners, Gottex Fund Management, Collins Capital, Blackstone and Brinker Capital, to name a few.

Many funds just could not gain traction with investors. When Pioneer recently liquidated its alternative funds, the three had less than $100 million in assets. Whitebox Advisors had about $300 million in assets in the three mutual funds it liquidated earlier this year.

“It’s typical for a firm to prune their lineup when the assets aren’t flowing in, and in particular, in light of the overall challenges the active management space faces, due to pressure from index-based mutual funds and ETFs,” said Todd Rosenbluth, director of ETF and mutual fund research at S&P Global Market Intelligence. “Keeping products on the shelf that aren’t gathering assets isn’t necessarily prudent.”

Investors withdrew nearly $38 billion from liquid alternative funds (including ETFs) last year, and almost $23 billion year-to-date through June, according to Lipper.

It also hasn’t been a very favorable market for a lot of these strategies, Charlson said. In 2015, liquid alternative funds declined 2 percent in value; these funds have lost 0.07 percent this year through June, according to Lipper. Dedicated short bias funds have been the worst performing so far this year, declining nearly 14 percent.

“These products in general were supposed to offer diversification away from traditional stock and bond strategies, and perform better when the market lagged, and what we’ve seen in the last couple of years, when the market’s been flat or down, these products have lost money also, on average,” Rosenbluth said.

Thomas Florence, president and CEO of 361 Capital in Denver, said the performance dispersion is quite wide among alternative funds, even those that use similar strategies, and that can confuse investors. Still, he is confident investors, and assets, will find the best ones.

But for many managers, figuring out the distribution puzzle is a real challenge, he said.

“If you aren’t organized properly, you don’t have the right commitment financially and you don’t understand the distribution side of selling mutual funds, you’re even more challenged,” Florence said.

In addition, some of the mediocre funds that have been launched are being sold by salespeople that can’t really explain what these products do.

“How good are they at really explaining these more complex products, frankly, to advisors? Which is critical,” Florence said.

So who’s left standing?

“From what I’ve seen, established mutual fund companies that have taken a thoughtful, strategic approach to how they’re going to build an alternatives business have done better than either firms that have come in from the hedge fund world and thought, ‘Hey, let’s try to make a go of it as a mutual fund,’ or the firms that may have had a fairly basic fund lineup and said, ‘Hey, let’s try this alternatives thing and see if we can build something there,’” Charlson said.

“We’re probably in the second inning of a nine-inning game, and I think some people think, ‘Oh well, alternatives haven’t delivered,’ and they’re looking at it as if we’re in the sixth inning,” Florence said. “But the market really hasn’t provided the opportunity for alternatives to do what they do best, and that’s because we’ve had such a good equity market. But now we’re in more challenging environments, and we’ll see.”

{kind=link}