Experiencing 10 percent swings in equity markets can hardly be a good sign, even though portfolio values were somewhat “restored” just in time for the August month-end statement. The absent (or vacationing) investor may not even know or fully appreciate what happened, but there is nothing to add that has not been stated on our end before: current markets are characterized by too much confidence, rich valuations, and deep-rooted trust that policy makers will “fix it.” These conditions, in a single or aggregate view, may not give reason for the “party” to be over, and yet significant damage has been done, especially from a technical perspective. Investors, more than ever, are advised to follow a disciplined approach to asset allocation, based on a personal financial planning paradigm, in combination with value considerations and technical analysis.

We have found that clients who are actively involved in planning and stating their financial objectives, paired with a critical view (often grounded in common sense), tend to achieve better investment results. Personally, I like to think of this process as entering into “a contract with myself,” allowing for the proper placement of assets related to spending-based needs and goals, instead of numeric return aspirations that are often simply derived from feelings of what the right number “should be,” rather than facts. In retrospect, investors should critically review their emotional state during last week’s sell-off, and the inherent urge “to do something”— whether selling or buying. As no one can predict market outcomes, these actions in one way or another can be counterproductive.

Valuations, or the “right” price paid, will ultimately determine investment outcomes in the long run; this will never change. To the contrary, market developments in recent months (the “short term”) could be better summarized as a “momentum game.” Next to the reasons stated in our opening paragraph, a persistent zero-interest-rate-policy (ZIRP) framework applied by global central banks has led “yield-starved” investors to riskier investment choices (mainly equities), despite elevated valuations. Mainstream media and collective delusion does the rest, “masking” the lasting impact of a debt super cycle, which still has to be fully resolved. Bonds (mainly government issues) that provided “hedging” quality vs. equity exposure during previous correction cycles are also breaking down as market participants figure that these prices may be too rich as well.

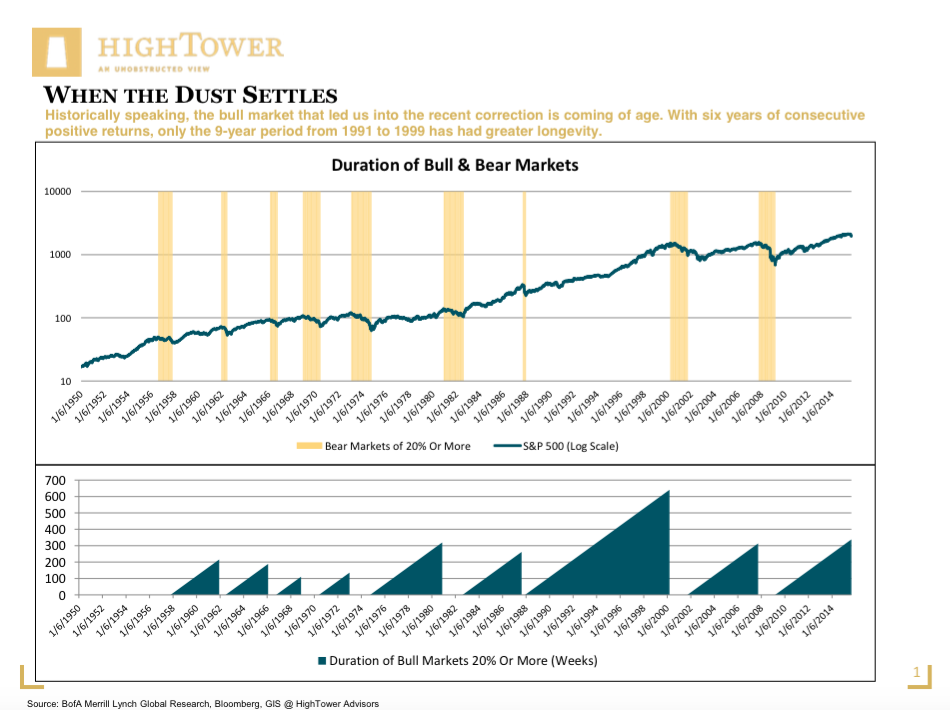

When in doubt, technical analysis can be used to assess the strength and “health” of a momentum-driven market that is not necessarily supported by valuations. Last week’s price formation, put in perspective, was rather unusual (also described as a V-shaped recovery, considering the sharp drop paired with a sharp rebound), and likely the result of short-covering, corporate buy-backs, and the combined actions of a few hopeful investors committed to bargain hunting. All in all, these actions are characteristically more aligned with a bear market (or beginning of it), and likely unsustainable. Historically speaking, the bull market that led us into the recent correction is coming of age. With six years of consecutive positive returns, only the nine-year period from 1991 to 1999 has had greater longevity.

In revisiting our outlook for 2015, From Wall Street to Main Street, we concluded that global central banks, sooner or later, will have to disappoint. The decadal “overhang” of credit expansion and related speculation, especially in real estate, is so substantial that policymakers will continue to seek the right balance of restructuring, recapitalization, and monetization. However, the right mix is far from accomplished, especially in Europe; it is for this reason that market participants will continue to experience “black swan-like” events. Now is the time to plan for the long term, prepare portfolios for more volatile times to come, and remain disciplined.

{kind=link}

Matthias Paul Kuhlmey is a Partner and Head of Global Investment Solutions (GIS) at HighTower Advisors. He serves as wealth manager to High Net Worth and Ultra-High Net Worth Individuals, Family Offices, and Institutions.