In her testimony before Congress last week, Federal Reserve Chair Janet Yellen was keen to escape the bonds of nuance and innuendo the market attaches to Fed language. Her emphasis was clear—the Fed will raise the federal funds rate when economic data support the move, a decision I foresee taking place during its Sept. 16-17 meeting. In the meantime, the period before the Federal Reserve raises rates is historically a great time to invest.

Over the past six tightening periods since 1980, the S&P 500 has returned 23.5 percent on average in the nine months prior to the first rate increase. Assuming the next tightening cycle begins at the Fed’s meeting in September, the nine-month period this time around began in mid-December. Since that time, the S&P 500 is already up more than 7 percent. Currently, a number of indicators, including my favorite, the New York Stock Exchange Cumulative Advance/Decline Line, show that the stock market is improving and can sustain its upward momentum.

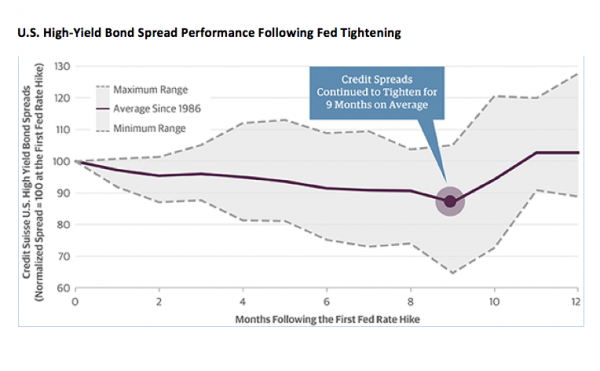

The period prior to a rate hike has also been a favorable environment for corporate credit. High-yield bonds and bank loans have outperformed investment-grade bonds on average by 4.0 percent and 1.6 percent, respectively, in the nine months leading up to the start of the last three tightening cycles. Even after the Fed begins to raise rates, tightening of monetary policy does not necessarily lead to an immediate widening of credit spreads. During four of the last five tightening cycles (1983, 1986, 1994 and 2004), default rates continued to fall for nearly the entire tightening period and ultimately ended lower than they were when the Fed started to tighten. In the past four instances where the Fed began raising rates following an extended period of monetary accommodation, high-yield spreads tightened on three occasions. On average, high-yield spreads tightened for nine months after the first Fed rate hike in a cycle.

All of this, combined with positive historical performance prior to past rate hikes, leads me to believe that a positive environment for U.S. equities and credit will continue between now and the first Fed rate hike. Even after the Fed commences on what I expect will be a slow and steady march of tightening, fundamentals can remain constructive, especially for high yield, for some time.

Eventual Monetary Tightening Is Potential Positive for U.S. High Yield

Since 1986, of the four instances when the Fed began raising rates following an extended period of monetary accommodation, high-yield bond spreads continued to tighten on three occasions. Tightening of monetary policy does not necessarily lead to an immediate widening of credit spreads.

{kind=link}

Source: Credit Suisse, Bloomberg, Guggenheim Investments. Data as of 2/25/2015. The range is generated by calculating the maximum and minimum values for all four previous cycles.

This material is distributed for informational purposes only and should not be considered as investing advice or a recommendation of any particular security, strategy or investment product. This article contains opinions of the author but not necessarily those of Guggenheim Partners or its subsidiaries. The author’s opinions are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC. ©2015, Guggenheim Partners. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information.

Scott Minerd is Chairman of Investments and Global Chief Investment Officer at Guggenheim Partners.