We have racked our brains regarding what valuation metrics to apply in the current investment environment, especially as natural price formation is still being largely influenced by accommodative policies around the globe. In our “Summer Charts” series published during August, we made the case that, aside from traditional ways to justify and assess market levels, a technical overlay should be applied to guide investors in their decision-making. We continue to discover notable formations, creating basis to conclude that fundamentals and markets are not so rosy when viewed in combination.

U.S. companies have accumulated record levels of cash on their balance sheets: approximately $1.43 trillion (June 2015 data), which is close to 10 percent of 2014 U.S. GDP, and the second highest level of the past 10 years (with the record having been set in Q4 of last year at $1.45 trillion; data sourced via FactSet). One argument to explain this extraordinary occurrence is that our domestic companies are just “killing it,” and stocking the rewards of their extraordinary business activities. However, we don’t think this is the only (or even a) plausible explanation.

If we consider that margin expansion, rather than sustained revenue growth, has driven corporate earnings, then we are given insight into practices of corporate executives managing results (rather than growing them), especially having taken advantage of preferable price points (cost) in capital and labor markets. For listed companies, this trend is underlined by an extraordinary uptick in corporate share buybacks - the third pillar of active earnings management. It should not come as a surprise that buybacks have been considered Wall Street’s new drug, particularly in an attempt to manage stock prices to higher levels in the absence of QE.

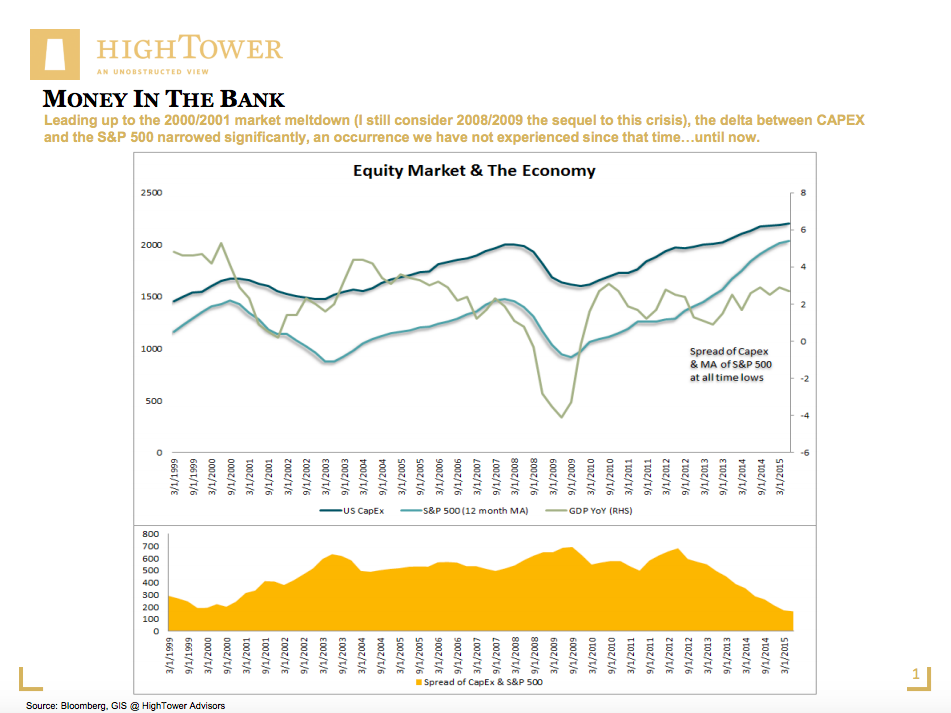

Further proof that stock prices are actively managed in today’s corporate world can be based on the comparison of stock prices (levels) and capital expenditures (CAPEX): money spent to buy fixed assets or add value to existing fixed assets, typically with an objective to manage a company’s future position. Leading up to the 2000/2001 market meltdown (I still consider 2008/2009 the sequel to this crisis), the delta between CAPEX and the S&P 500 narrowed significantly, an occurrence we have not experienced since that time…until now. Notably, both environments are marked by historically low rates.

There are several conclusions to our findings: 1) As long as corporate executives’ and CEOs’ compensation is tied to the stock prices of their respective companies, earnings will be managed; 2) Investors need to identify “true growers” and meet the current environment with an active selection process, rather than a passive beta approach to asset allocation 3) Based on historical data, when the delta between corporate expenditures and stock prices narrows significantly (currently the lowest since 1999) a “drop-off” in corporate investment and respective stock levels should be expected.

{kind=link}

Matthias Paul Kuhlmey is a Partner and Head of Global Investment Solutions (GIS) at HighTower Advisors. He serves as wealth manager to High Net Worth and Ultra-High Net Worth Individuals, Family Offices, and Institutions.