With an understanding that Fed policy has been a substantial driver of asset markets, there is value in considering the rate environment and stance of our policymakers going forward. Recently, policy indecision unsettled market participants and contributed to significant volatility. Judging Fed policy has been akin to “reading tea leaves,” with too many of us postulating strong opinions, which, so far, have not come to materialize—even for the best. Today, we wish to offer a potentially different, more quantitative approach to this issue.

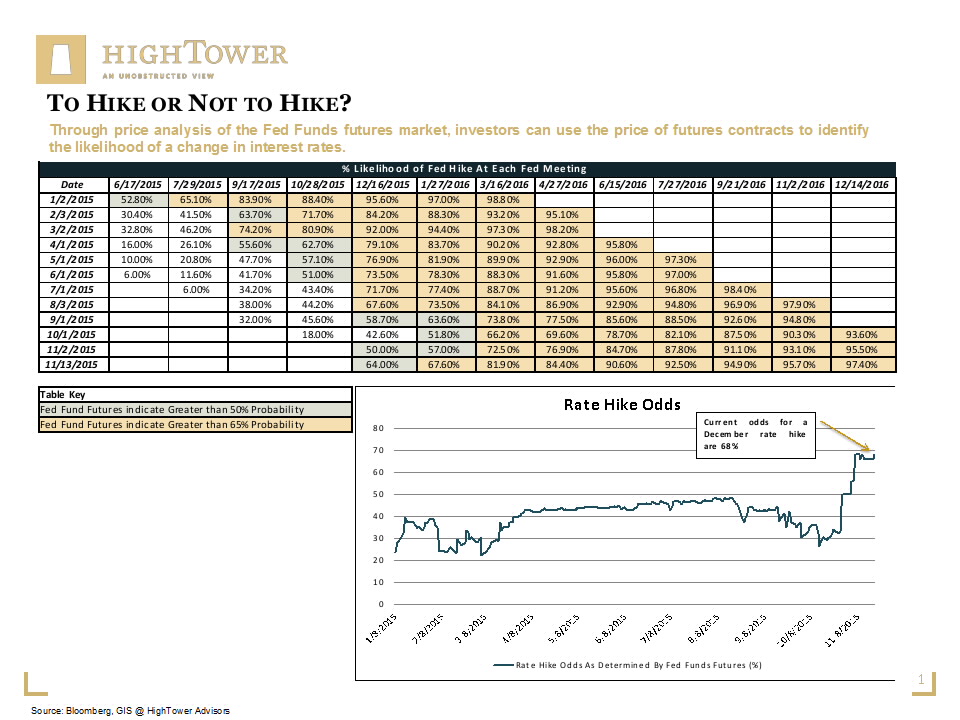

Through price analysis of the Fed Funds futures market, investors can use the price of futures contracts to identify the likelihood of a change in interest rates. Based on the price of the contract, number of days until the futures contract expires, and time until the next Fed meeting, a complex formula derives the probability of a rate hike. As the model is binary, the likelihood of no rate hike is 100 percent minus the probability of a rate hike. Here are our findings:

- Since the beginning of this year, at no point were expectations for a rate hike at an immediately upcoming FOMC meeting as high as they currently are for the next FOMC meeting. Expectations “traded” as low as six percent probability prior to the July meeting, and have since risen to 64 percent for the December meeting.

- Even the widely anticipated first hike for the September FOMC meeting had a relatively low probability, at only 32 percent to begin with. The highest probability for a September hike was noted in January at 83 percent, and then declined somewhat consistently over the following months. In other words, the Fed did not surprise with indecision, at least based on our data.

- Although the probability for higher rates at year-end 2015 declined from 90 percent to just over 40 percent during the course of this year, this trend turned at the beginning of November, moving to favor a rate hike in December; such a trend reversal has not occurred in anticipation of any other 2015 FOMC meeting.

As cryptic as some of the old Shakespeare works are, so is today’s investment environment; if left to my gut feeling when assessing the current opportunity set, then my conclusion would be that hardly anything seems to make sense. However, the real world, as we have demonstrated, is a different one—a testament to the need for disciplined investing through data analysis. And so, in the upcoming December FOMC meeting notes, let it be written, “to hike.”

“Though this be madness, yet there is method in’t.” -Shakespeare from Hamlet, Act II, Scene II

{kind=link}

Matthias Paul Kuhlmey is a Partner and Head of Global Investment Solutions (GIS) at HighTower Advisors. He serves as wealth manager to High Net Worth and Ultra-High Net Worth Individuals, Family Offices, and Institutions.