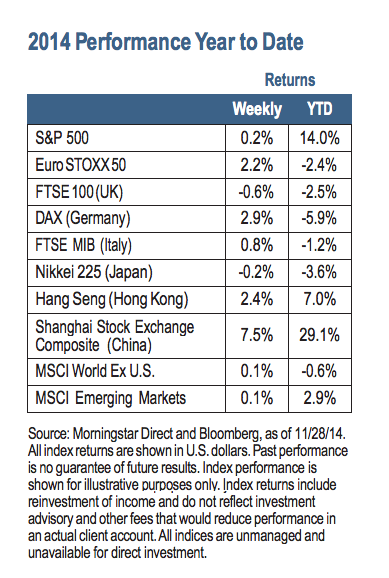

U.S. equities capped off the holiday-shortened trading week with a sixth consecutive week of gains. The S&P 500 Index advanced 0.2%, with the consumer discretionary sector leading the way and energy lagging.1 The main economic story last week was OPEC’s decision to leave production levels unchanged, resulting in yet another decline in oil prices. Both Brent Crude and West Texas Intermediate prices fell to their lowest levels in four years. (1)

Investing May Become More Difficult From Here

For some time now, investors have been well served by holding overweight positions in equities (particularly U.S. equities), taking long positions in the U.S. dollar and avoiding commodities (primarily oil). We think these trends will largely continue. However, the investing world is in the midst of a transition as the U.S. economic expansion moves into the second half of its cycle. In particular, we believe a number of economic and market factors may be changing:

In sum, we think this transition means that we will be moving from what was in hindsight a relatively easy investment environment to one that will be somewhat harder and that will require more difficult decisions.

Weekly Top Themes

- Stronger growth will make it more difficult for the Fed to keep rates low. The latest economic data shows that third-quarter GDP was revised higher from 3.5% to 3.9%. (2) Even with inflation still low, such robust growth makes it harder for the Fed to justify near-zero interest rates.

- U.S. consumers should benefit from lower oil prices. OPEC members last week failed to agree to cut oil production, putting further downward pressure on prices. This should lead to additional increases in consumer spending.

- Cheaper oil prices are hurting some areas of the global economy, but should be a net positive. Lower energy prices are reflective of lingering deflationary pressures, but should contribute to global growth. Within the United States, the combination of lower energy costs and still-low interest rates is benefiting the consumer sector and should act as a tailwind for economic growth.

The Macro Environment Remains Equity-Friendly

Over the coming year, we expect the global economy to gradually improve, led by a transition to a self-sustaining expansion in the United States and an eventual increase in global trade. Falling oil prices present deflationary risks, but should help promote growth in the U.S., the euro area, Japan and China. Monetary policy also remains pro-growth. The Bank of Japan has been ramping up its easing program and we expect to see further action from the European Central Bank. The Fed is poised to begin increasing interest rates, but will likely proceed cautiously. Geopolitical events remain a wildcard and could contribute to market turbulence, but would need to escalate to derail the global recovery.

At this point, equity valuations are no longer cheap, but at worst they are only mildly expensive compared to their own history and remain attractive compared to Treasuries and cash. Corporate earnings will need to continue to improve to allow prices to move higher, and we think the outlook for earnings remains solid. We do think volatility is likely to rise from what has been historic lows, but we also believe the table is set for a continued grinding higher of equity prices.

(1) Source: Morningstar Direct and Bloomberg as of 11/28/14

(2) Source: U.S. Department of Commerce

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Non-investment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

©2014 Nuveen Investments, Inc. All rights reserved.

Robert C. Doll, CFA is Chief Equity Strategist and Senior Portfolio Manager for Nuveen Asset Management. Follow @BobDollNuveen on Twitter.