Let’s connect the dots: in previous weeks, we made the argument that continuously rising markets, especially in the U.S., have been characterized by an over-bullish and overconfident sentiment, but mainly supported through accommodative policies. At the same time (since 2000/2001 particularly), investors have been losing purchasing power, despite stellar market returns, as official inflation readings have understated the true cost of living. Differently put, as long as the economy and the consumer remain in a “sluggish” state, the global accommodative reflation/inflation game is still on. The early conclusion of this blogpost, consequently, is an easy one: even with all warning signs to be considered these days, investors need to continue investing in equities, as cash and fixed income will not serve as permanent stores of value.

How to go about allocating money is a different challenge, with risk/reward constellations blurred, especially since artificially low interest rates have created the will for investors to reach for returns in riskier places. In my view, the basis for sound decision-making has never changed, and should be focused on attractive valuations and anticipated future growth.

Buying the BRICs (Brazil, Russia, India, China), as the original path to emerging markets (EM) investing, has been too narrow an approach—particularly when considering the commodity “meltdown” since 2011 that has had a severe impact on many of their economies. We know now that all EM simply cannot be treated equally. Nevertheless, developed markets will lose importance over the years to come. It is estimated that the contribution of EM to global GDP will account for more than 60 percent by 2020, while the U.S. and Europe’s combined contribution will decline to a mere 15 percent. The underlying core drivers and benefactors of these developments have not changed: young and dynamic economies and an emerging consumer class. Today, EM accounts for nearly 20 percent of global sales, with a projected 230 of the Fortune 500 companies based there by 2025, up from only 45 companies (5 percent), in 2000.

In the short term, EM should be subjected to continued volatility. As we discussed in It’s the Dollar, Stupid, the reversal of global capital flows and an inherent shortage of U.S. dollars in the financial system are the main drivers of the current consolidation; dollars needed to “balance the system” are simply not available. The IMF recently warned that EM corporations and banks have over-borrowed by $3.3 trillion in aggregate. The excess level of debt, especially in the private and commodity-producing sectors, will have to be reduced for financial health to be restored.

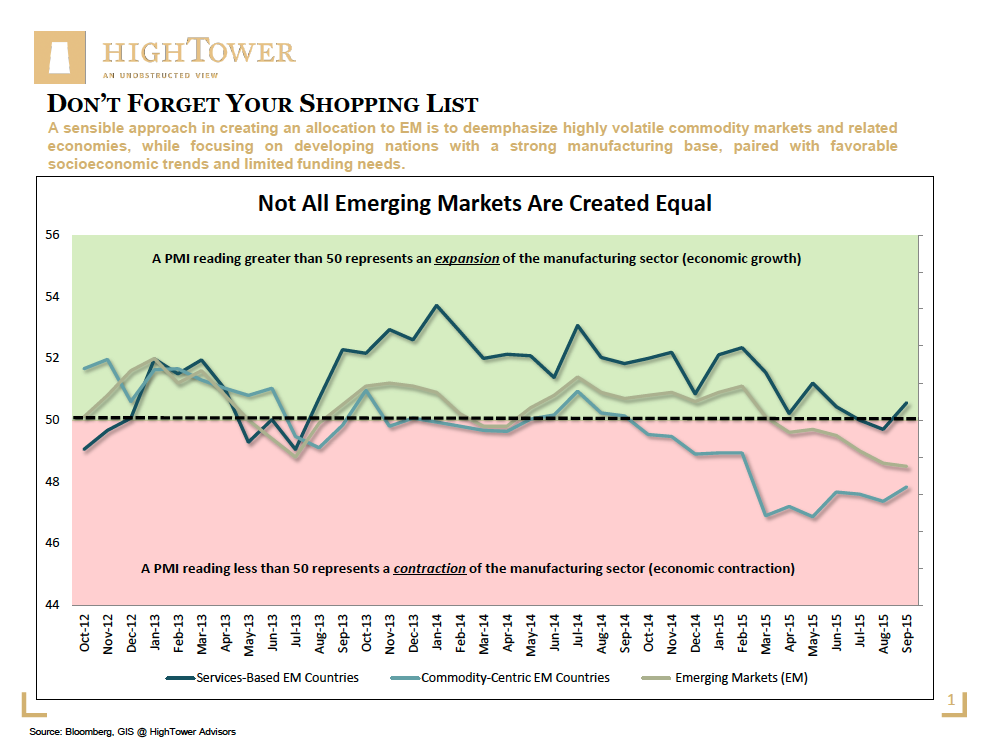

Investors have basis for two investment opportunities: 1) for those expecting a recovery in commodity/energy prices, some EM markets have simply been “crushed” in the path of the more recent global equity correction, and consequently may offer discounted value in the long run. Periods of intense volatility, however, have to be anticipated, especially if respective economies are paired with current account deficits; 2) another, likely more sensible, approach in creating an allocation to EM is to deemphasize highly volatile commodity markets and related economies, and instead focus on developing nations with a strong manufacturing base, paired with favorable socioeconomic trends and limited funding needs. At last, a combination of the two approaches may hold the right answer. Now is the time to create a plan and “shopping list” to pick the right exposure to the developing world.

{kind=link}

Matthias Paul Kuhlmey is a Partner and Head of Global Investment Solutions (GIS) at HighTower Advisors. He serves as wealth manager to High Net Worth and Ultra-High Net Worth Individuals, Family Offices, and Institutions.