It is a common understanding that a “canary in the coalmine” acts as a metaphor for impending danger. Quite understandably, investors are always on the lookout for this proverbial little bird to guide decision-making, either by avoiding losses or taking advantage of opportunities presented by increased volatility. Yet, these days, we have to wonder if the proper collective focus guiding the process of avoiding danger is being applied. With an obsession to dissect day-to-day moves in equity markets, especially led by the mainstream media, most investors have failed to notice (or at least consider) that volatility in most asset classes (vs. equities) has increased sharply over the last year—potentially foreshadowing more significant issues to come, and also that we may rest with a false sense of security regarding our investments.

We know the obvious stories too well, for example the recent correction in Chinese equities (please see our recent entry, Bulltrap Made in China), but it was the credit market that had given entry to the Financial Crisis in 2007—not late 2008, when equities came under pressure. Volatility in bonds is up 40 percent(!) year-over-year, but even more concerning is that there are now signs of increased fragility and divergence of liquidity conditions across multiple fixed income market segments.

The picture in bonds is mixed, and investors have to look for the right signs to understand risk/reward and, more importantly, whether or not there is a bigger issue “brewing.” Whereas most sovereign bonds have returned to pre-crisis transaction sizes (in the U.S. especially) as well as acceptable bid-ask spreads, the trading of corporate debt has become more challenging. Some market makers note that liquidity conditions in major corporate segments resemble conditions of 2005-2006 (which were not all favorable).

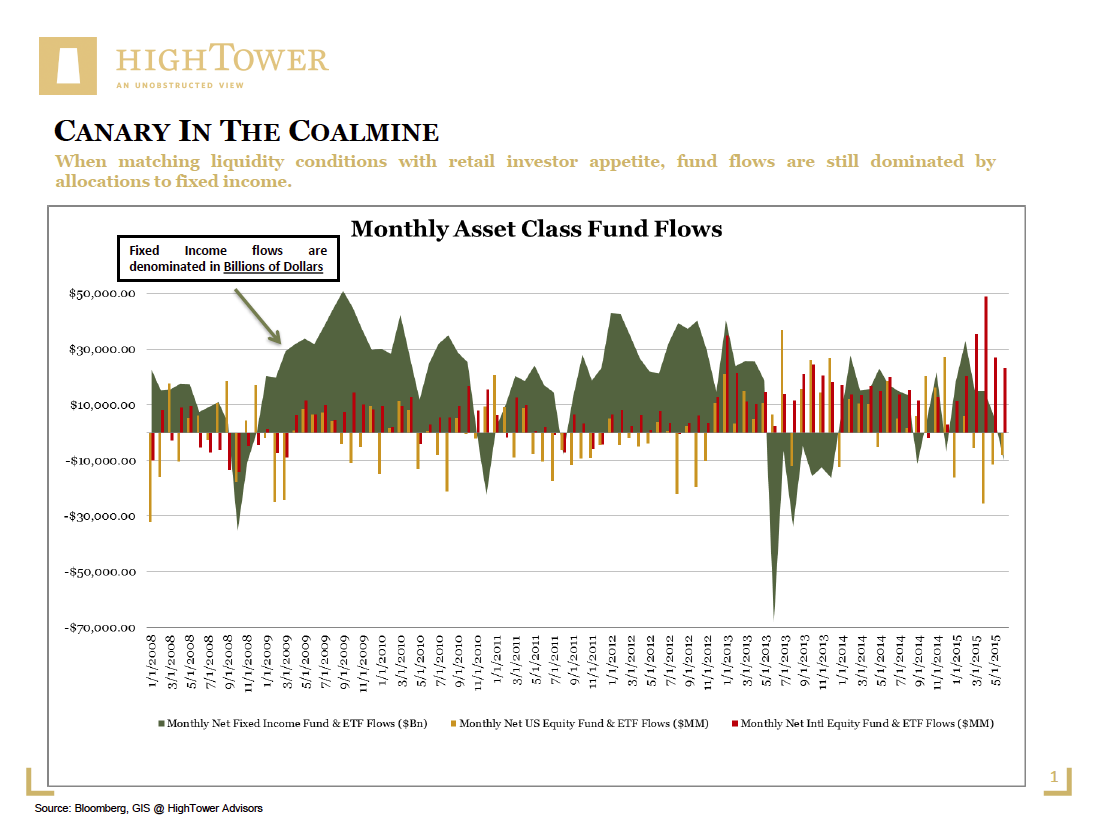

When matching liquidity conditions with retail investor appetite, fund flows are still dominated by allocations to fixed income. Even though the bond market has grown to a staggering $100 trillion (2014 data), an increase of 40 percent since mid-2007, the very segments sought after by most private investors are challenged by liquidity conditions (some issuances have simply not kept up with demand). Over the past five years, U.S. fund holdings in fixed income instruments (MFs/ETFs) have grown by more than $1 trillion, while net dealer holdings (the liquidity providers) have contracted materially.

{kind=link}

As much as we think equities are “risky” or “riskier” than bonds, respective market volatility in the U.S. (as measured by the VIX) is still below its 20-year average and unchanged year-over-year. However, the sharp volatility increase in other market segments, paired with concerns regarding liquidity, constitutes our exemplary canary in the coalmine. Nevertheless, given that global central banks have compressed natural market outcomes, coupled with more-than-rich valuations in stocks today, equity investors should be careful not to develop a false sense of comfort. At the same time, bond investors need to consider liquidity constraints as a major risk, especially in instruments that carry the “daily liquidity” tag, such as most bond ETFs.

If our canary is correct, the potential adjustment to historic volatility levels across multiple asset classes will also lead necessary change of somewhat laissez-faire investor sentiment. As we have argued before, now is the time for investors to adopt a rigorous financial planning framework, recognize the relationship between risk and reward, and adhere to a standard of global diversification.

Matthias Paul Kuhlmey is a Partner and Head of Global Investment Solutions (GIS) at HighTower Advisors. He serves as wealth manager to High Net Worth and Ultra-High Net Worth Individuals, Family Offices, and Institutions.