There has been a growing recognition that China can be complicated, not only considering the seamless integration of this emerging superpower into an already tightly-knit world economy (and related adaptation of global financial standards), but also with respect to the question of how economic progress is (or should be) reported to the outside world. In comparison to a number of other emerging “hotspots,” with Greece and Puerto Rico serving as recent examples, China’s significant domestic equity market meltdown should be regarded as truly complicated and likely entirely “made in China.”

In our 2015 Outlook, From Wall Street to Main Street, we concluded that global central banks eventually will have to disappoint, as their restructuring, recapitalization, and monetization efforts to address the overhang of a decadal credit expansion would create speculation (as a byproduct) substantial enough to trigger black swan-like events. Now here we are: an estimated $3.2 trillion, nearly equal to the total market capitalization of the United Kingdom (at $3.7 trillion), has been eliminated from the Chinese domestic stock market since its rapid rise and peak in mid-June 2015.

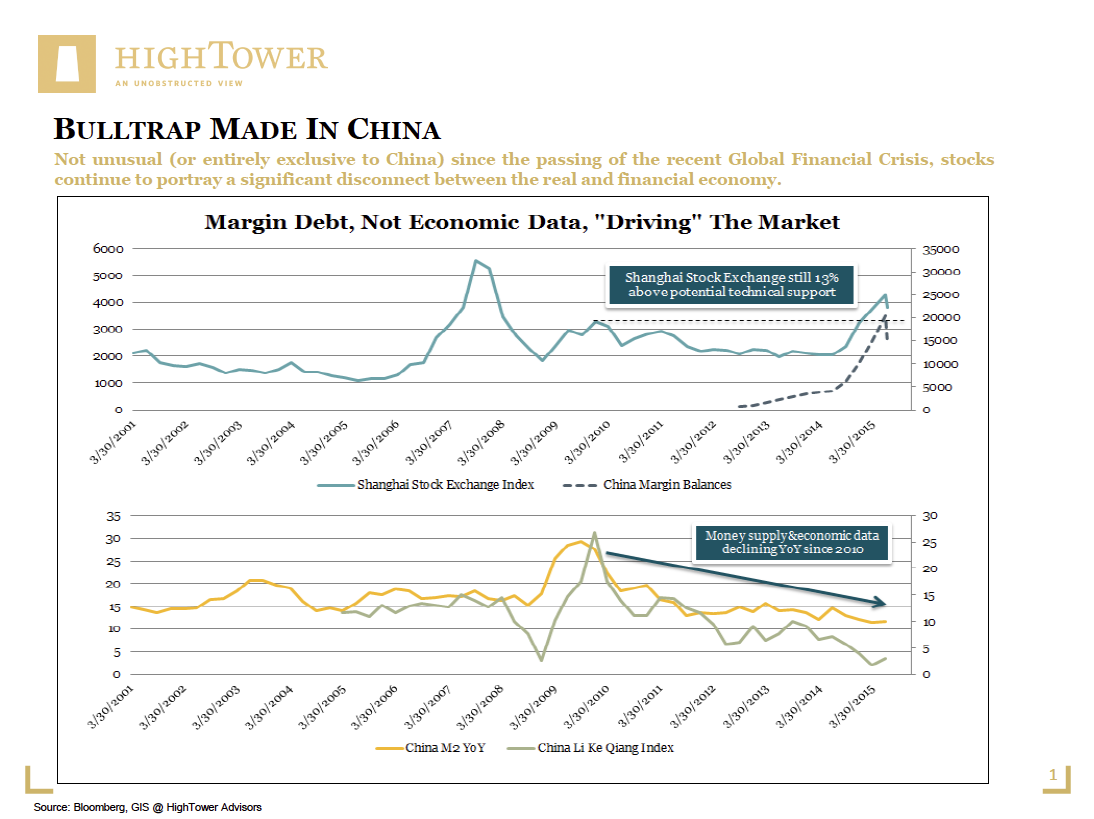

Not unusual (or entirely exclusive to China) since the passing of the recent Global Financial Crisis, stocks continue to portray a significant disconnect between the real and financial economy. Based on the Li Keqiang Index, a composite (and good indicator of economic activity), accounting for 1) consumption of electricity by manufacturers; 2) volume of goods carried by railways; and 3) balance sheets of financial institutions, the Chinese economy has been in a declining trend since 2010, only having recovered briefly in 2011 and 2012-2013 before resuming its ongoing consolidation. At the same time, the Shanghai Stock Exchange Composite Index kept moving exponentially higher, with a noteworthy June 2014-2015 year-over-year increase of nearly 150 percent(!).

The Chinese were excessive in their willingness to speculate, which has been quite evident in the number of new brokerage accounts opened in recent months. Whereas, on average, nearly 181,000 accounts per week were established for trading purposes in 2014, this figure passed the 1.5 million mark in 2015, with a peak reached in the last week of May at 4.5 million openings per week—clearly “over the top,” and something the world has not experienced since the dot-com bubble in the U.S. While we can assess the overall value destruction in general terms, the socioeconomic impact of the market’s rapid decline is far more worrisome, as private investors are carrying most of the burden.

To make matters more complicated, Chinese policymakers did not attempt to curb the excessive behavior but instead fueled a speculative boom through a somewhat unparalleled liquidity bonanza. Even with the economy in full consolidation, the availability of margin (for trading purposes) increased by nearly 2,900 percent between mid-2012 and the June 2015 market top. Regrettably, Chinese authorities did not stop there: with equities meeting a violent decline, the Chinese Government “crowded out” market participants by halting trading in nearly 70 percent of all listed stocks (aside from other rather questionable measures).

Given the rapid drop of Chinese markets, investors around the globe are “banking” on finding deals via buying into much lower stock and index levels; although this may sound like a simple approach, it will not be easy or straightforward, as the differentiation between China's real economy and financial economy is more important than ever. China will continue its rapid ascent as a global economic power, including the aspiration for reserve-currency status and the inherent recycling of reserves through “financial colonization” (think Africa, Brazil, etc.), but equity culture will suffer for some time to come. The “natural” buyers into the two domestic bourses (Shanghai and Shenzhen) are the very same who have experienced significant losses of both assets and trust. With every recovery, we should expect sellers trying to recoup losses, likely fading many rallies to come.

{kind=link}

Matthias Paul Kuhlmey is a Partner and Head of Global Investment Solutions (GIS) at HighTower Advisors. He serves as wealth manager to High Net Worth and Ultra-High Net Worth Individuals, Family Offices, and Institutions.