In “Tradition,” the opening number of the musical Fiddler on the Roof, Tevye the dairyman regales the audience with the time-honored roles of family members and other villagers in keeping his society alive. Tevye would not have made a good alternative (“alt”) fixed income fund manager. These managers shun the conventions of bond investing by taking long/short bets or by hedging credit or duration.

Historically, vanilla bond funds have been a portfolio safety net. They provided the yin to the stock market’s yang. But dramatic shifts in monetary policy have disrupted the traditional stock-bond relationship, compelling money managers to shop for fixed income strategies that can capitalize upon an asymmetric risk of rate hikes and the prospect of widening credit spreads.

The question investors and advisors must ask is whether so-called “liquid alt” funds—alternative investment strategies in a mutual fund or ETF wrapper—provide value for money. They’re certainly not cheap. The average investor pays 134 basis points (1.34 percent) annually to own a nontraditional bond fund. A broad-based, passively managed bond fund, the iShares Core US Aggregate Bond ETF (NYSE Arca: AGG), can be held for just eight basis points (0.08 percent).

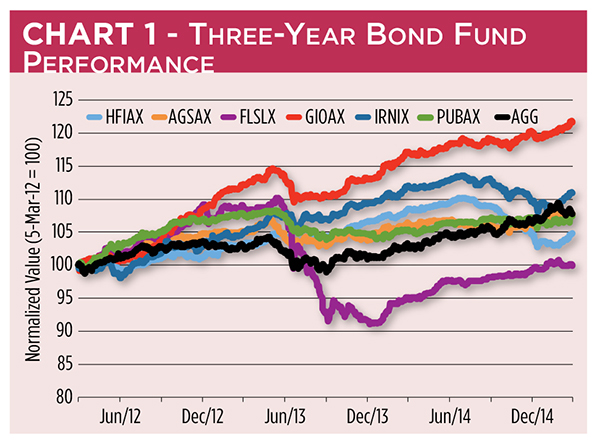

The unequivocal answer to the value question is: “It depends.” If you define a bargain as a higher return than that produced by a low-cost exchange traded fund, alt portfolios are a mixed bag. Of a half-dozen funds with three-year track records, three have outdone AGG on a cumulative basis. Chart 1 illustrates the comparative performance of this seasoned alt fund universe.

Collectively, these funds produce costly gains. On a market-weighted basis, nontraditional bond funds crank out returns at a 2.6-to-1 ratio to costs. The index ETF produces returns at a 32.4-to-1 rate.

More Than One Way to Measure Value

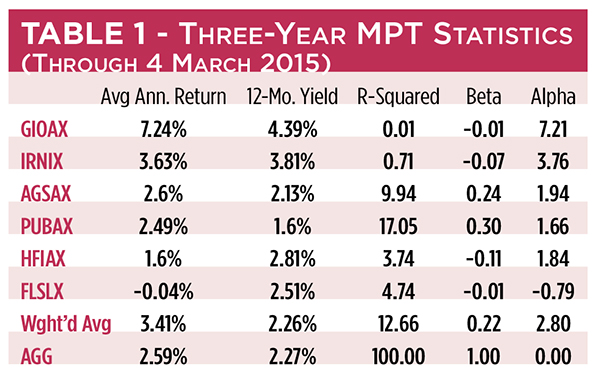

There’s more than one way to measure value, of course. Modern Portfolio Theory (MPT) statistics—i.e., R-squared, beta and alpha coefficients—are universally used to describe a fund’s relationship to its benchmark and, therefore, the fund’s investment utility.

- R-Squared – Values for this statistic range from 0 to 100 and reflect the percentage of the fund’s price movements that can be explained by movements in the benchmark. Nontraditional bond funds will typically be uncorrelated to classic bond benchmarks.

- Beta – Systematic risk is measured by the beta coefficient. A beta of 1 indicates the fund will likely move in lockstep with the benchmark. More-volatile funds will exhibit betas above 1, while low-volatility portfolios are signposted by coefficients less than 1. A negative beta denotes fund price action inverse to that of the benchmark.

- Alpha – A manager’s skill in outperforming the benchmark is revealed by a fund’s alpha coefficient. The statistic is derived by comparing the fund’s return to that of the beta-adjusted benchmark. A positive alpha of 1 indicates the fund outperforms its benchmark by 1 percent, while a negative alpha of similar degree implies the fund lags the benchmark by 1 percent.

As you can see by the market-weighted averages in Table 1, the alt funds are barely correlated (R-squared of 12.66) to the broad-based bond market mirrored by AGG but, because of their low volatility (beta of 0.22), they outdid the index fund on a risk-adjusted basis (alpha of 2.80).

Performance Varies

Individually, there’s a fair degree of variance in the performance of the nontraditional bond funds, in large part due to their differing investment mandates.

Guggenheim Macro Opportunities Fund (OTC: GIOAX) – This $2.9 billion portfolio is the archetype of an unconstrained fund. GIOAX managers look for investment prospects across a wide spectrum, including global fixed income, equity, currency and commodities markets. Presently, the fund’s largest allocation is a 24 percent slug of medium-term (five- to seven-year) bonds. GIOAX’s overall bond exposure is 81 percent net long and is tilted to U.S. issuers. With a 127 basis point expense ratio, GIOAX is the most cost-effective fund in the alt space.

Iron Strategic Income Fund (OTC: IRNIX) – At 150 basis points, this $328 million fund plows the middle ground expensewise. It operates with a diverse set of tactics, including long/short credit plays, yield curve maneuvers and convertible arbitrage. IRNIX is nearly 60 percent net long and is skewed to medium-term maturities.

AllianceBernstein Unconstrained Bond Fund (OTC: AGSAX) – A global multisector fund, AGSAX is most heavily weighted in long-term (20- to 30-year) maturities with a slightly net long bias. The $380 million fund’s 90 basis point expense ratio is the lowest in the nontraditional universe.

PIMCO Unconstrained Bond Fund (OTC: PUBAX) – PIMCO’s product, with a $10.5 billion asset base, is the category behemoth as well as the lowest-yielding fund. The fund’s mandate allows a wide-ranging duration target to achieve positive absolute returns. PUBAX tilts heavily toward short (one- to three-year) maturities in its net long securities mix. Holding costs for PUBAX run 130 basis points a year.

Hatteras Long/Short Debt Fund (OTC: HFIAX) – This $380 million portfolio splits its assets among seven managers pursuing arbitrage, long/short credit, structured credit and relative value plays at an annual expense of 299 basis points.

Forward Credit Analysis Long/Short Fund (OTC: FLSLX) – Forward’s $132 million fund is most heavily weighted in the 10- to 15-year maturity bucket. FLSLX exclusively owns debt from domestic issuers, mostly municipalities. Expenses run 211 basis points annually.

Many analysts distrust a fund’s beta and, by extension, its alpha when the R-squared coefficient is low. For these critics, other measures of portfolio efficiency are heeded. These typically include the Sharpe, Sortino and information ratios.

Sharpe, Sortino and Information Ratios

- Sharpe ratio – This metric ranks risk-adjusted returns by dividing an investment’s excess return—i.e., the return above or below the risk-free rate—by its volatility, or standard deviation. The higher the ratio, the better. Generally speaking, a ratio of 1.00 represents “good” compensation for risk, while a ratio of 2.00 earns a “very good” rating, and 3.00 or better is “outstanding.”

- Sortino ratio – A derivative of the Sharpe ratio, this statistic uses downside deviation rather than total volatility to gauge risk-adjusted returns. With the Sortino ratio, a manager isn’t punished for “good” risk, only for “bad” risk. If an investment’s returns are normally distributed, i.e., in a bell-shaped curve, its Sortino ratio will be roughly equivalent to its Sharpe ratio. Sortino ratios can be graded on the same scale as Sharpe ratios.

- Information ratio – The information ratio uses an investment’s return over/under that of its benchmark as a dividend and the investment’s tracking error as a divisor. The ratio assesses a manager’s skill when deviating from a benchmark to produce excess returns. Like the other ratios, a higher quotient is better as it denotes the efficiency of a manager’s bets. A ratio of 1.00 or better is usually considered “outstanding,” 0.25 is deemed “good” and 0.00 is “above average.”

From Table 2, we can see that alt funds have bettered the risk-adjusted return of the traditional long-only AGG fund on a market-weighted basis. That’s not to say that all nontraditional funds are superior, however. There are clear winners and losers in the pack. The Guggenheim GIOAX fund is the across-the-board victor, handily outdoing the index ETF on every measure except cost, while Forward’s FLSLX portfolio brings up the category’s rear.

Will it always be thus? No doubt there’ll be jockeying for primacy among nontraditional bonds funds, especially as newer funds enter the fray. As for the prospects of conventional long-only funds like AGG, it’s good to remember Woody Allen, who once said, “Tradition is the illusion of permanence.”