Back in the 19th century, one of the rallying cries for this country's zealous westward expansion was "54-40 or fight!", a war whoop referring to the latitude of the disputed northern border of Oregon Country.

In the 20th and 21st centuries, portfolio managers have touted a numeric acclamation of their own. You know it as "60/40," the classic equity/fixed income mix. By throwing 60 percent of a client's assets into the stock market and 40 percent into bonds, the thinking goes, you'll be diversified enough to successfully ride out most market cycles. By and large, that allocation's worked pretty well over the past few years.

The current environment isn't like most market cycles, though. Low yields and volatility have pushed and pulled reward-to-risk ratios out of their historic shapes, prompting many advisors to consider allocations to alternative investments ("alts") to diversify away some rebound risk. Nowadays, "60/40" is giving way to "50/30/20," an apportionment that makes room for alts with carve-outs from both the equity and fixed-income sides.

Here's the case for alts:

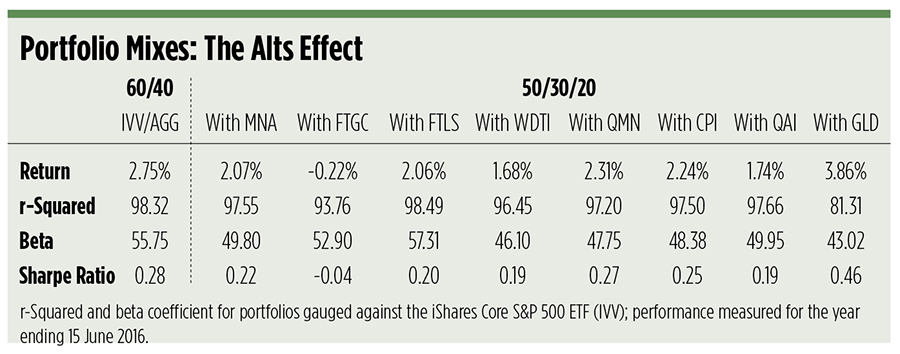

If you held a simple "60/40" portfolio consisting of investable proxies for the S&P 500 Index and the Barclays Aggregate Bond Index over the past decade, you might have thought that the large bond allocation would have loosened your ties to the equity market. Not so, however. Your portfolio's r-squared (r2) coefficient would have been 95.50, indicating that most all of its variance could be explained by gyrations in the S&P benchmark.

Still, your bond allocation would have dampened the portfolio's volatility and improved its risk-adjusted return compared to a straight stock allocation. The "60/40" mix earned a .87 Sharpe ratio versus a .61 value for the S&P 500 in the last ten years. Think of the Sharpe ratio as excess return per unit of volatility. A ratio of "1" (1.00) represents a good return for the risk undertaken; "2" is very good and "3" is exceptional. The relatively low Sharpe ratio for the classic allocation in the past decade reflects the deep swoon in security prices during the 2008-2009 financial crisis.

More recently, the "60/40" portfolio's become less efficient. In the past year, metered by its daily returns, it's earned a lowly .28 Sharpe ratio.

You can see why advisors and investors are looking to alternatives now. Alts are often touted for their low correlations to stock and bond benchmarks. Low correlation is one thing, but not the only thing to consider. Obviously, returns matter. Let's see how some of these alternative exposures, captured in some leading exchange traded funds (ETFs), are behaving.

Alternative exposures

Arbitrage – An arbitrage is typified by buying and selling related securities to capitalize upon pricing disparities. Merger arbitrage is the basis for the IQ Merger Arbitrage ETF (NYSE Arca: MNA), a portfolio that buys takeover targets and shorts equity indexes to minimize market exposure. Over the past 12 months, MNA's r-squared coefficient was 19.62 measured against the iShares Core S&P 500 ETF (NYSE Arca: IVV) and 4.43 versus the iShares Core U.S. Aggregate Bond ETF (NYSE Arca: AGG).

Commodities – The First Trust Global Tactical Commodity Strategy Fund (Nasdaq: FTGC) is an actively managed fund that provides net long exposure to a broad spectrum of commodities through futures contracts, ETFs and structured products. Against IVV, FTGC earns a 14.62 r-squared and 1.18 against AGG.

Hedged Equity – The actively managed First Trust Long/Short Equity ETF (NYSE Arca: FTLS) takes both long and short position in U.S. stocks, maintaining a net long exposure between 100 percent and 50 percent. The fund's managers typically buy issues noted for the quality of their earnings while taking short positions in low-quality stocks. R2: 83.52 (vs. IVV); 9.27 (vs. AGG).

Managed Futures – Managed futures differ from the commodities allocation represented by the likes of FTGC because managed futures don't have a long mandate. Funds in this category could conceivably be net short at any given time. The Wisdom Tree Managed Futures Strategy Fund (NYSE Arca: WDTI) is actively managed to emulate the returns of index strategy, tracking currency, commodity and Treasury futures. R2: 1.34 (IVV); 0.00 (AGG).

Equity Market Neutral – Market-neutral funds, such as the IQ Hedge Market Neutral Tracker (NYSE Arca: QMN), attempt to zero out beta, going a step beyond hedged equity products that retain some degree of market exposure. QMN uses large fixed-income and cash positions to nullify beta, rather than directly shorting stocks. R2: 5.30 (IVV); 2.34 (AGG).

Real Returns – The mandate of a real returns, or absolute value, fund is deceptively simple: beat inflation. The IQ Real Return ETF (NYSE Arca: CPI) uses a multi-factor model to build an "ETF of ETFs," including a large exposure to short-term Treasury securities. R2: 10.59 (IVV); 0.47 (AGG).

Multi-Strategy – A cornucopia of ETFs, the IQ Hedge Multi-Strategy Tracker ETF (NYSE Arca: QAI) takes a "fund-of-funds" approach across different strategies (long/short equity, arbitrage, etc.), to provide broad exposure to alternative strategies. R2: 47.96 (IVV); 1.47 (AGG).

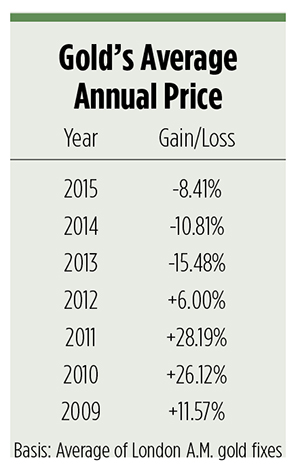

Gold – Bullion, with its low correlation to stocks, is a classic portfolio diversifier. Gold's returns, however, are notoriously cyclical. The average annual return for spot metal has been negative in three of the past seven years. Several bullion-backed products are available, the largest being the SPDR Gold Shares Trust (NYSE Arca: GLD). R2: 4.16 (IVV); 11.04 (AGG).

Track records

In the past 12 months, the classic "60/40" portfolio produced a total return of 2.75 percent, largely on the back of bonds. IVV barely squeaked by with a 0.94 percent gain for the year while AGG picked up 5.47 percent. The bond allocation also dampened the inherent volatility of the stock side. The standard deviation of IVV's daily returns is 16.70 percent. The standard deviation for the combined portfolio is 9.42 percent. That's reflected in the 55.75 beta coefficient.

Note the effect of carve-outs for alts on portfolio beta. One "50/30/20" allocation produced a higher beta coefficient than the "60/40" mix. Adding FTLS actually increased stock risk. Given the long/short ETF's high r-squared value, that's not really surprising.

All the other alts-enhanced portfolios exhibit lower beta, signaling potentially smoother rides in the event of a future equity downturn. One alt ETF, though, dragged portfolio returns into the red. FTGC, the long-only commodity fund, suffering losses on its livestock and soft commodities positions, tumbled 11.65 percent in the past 12 months.

Only one alt exposure actually improved gross and risk-adjusted returns over the past year. Adding gold was a tonic for the basic portfolio, improving gross and risk-adjusted returns while lowering the beta and r-squared coefficients.

{kind=link}

So gold's the way to go for an alt-enhanced portfolio, right? Well, maybe. Gold's certainly proved itself as a portfolio diversifier over the long term. Given its cyclicality, though, would you really want a fifth of your portfolio in gold?

Are we, after three years of grinding losses, headed back into a gold upcycle? It's hard to say. What's obvious is this: tying up 20 percent of a portfolio in a single asset is risky. Looking at the table of gold's price, you can see that the risk paid off handsomely in certain years; in others, not so much.

"A mask of gold hides all deformities," opined English dramatist Thomas Dekker. In "good" years, gold looks like a genius add. Gold can certainly be part of a 20 percent allocation to alts, but to hedge against the "bad" years, other non-correlated assets such as market-neutral equity and absolute return products ought to be in the mix.

Brad Zigler is WealthManagement's Alternative Investments Editor. Previously, he was the head of Marketing, Research and Education for the Pacific Exchange's (now NYSE Arca) option market and the iShares complex of exchange traded funds.