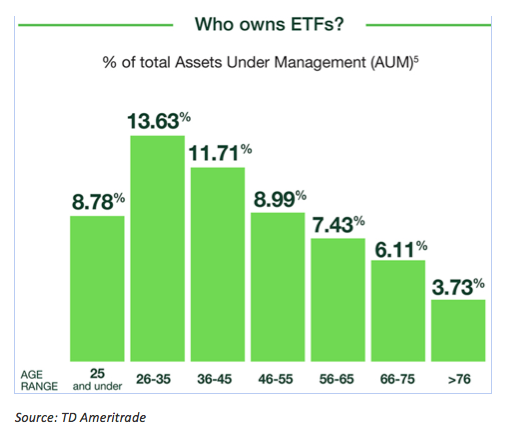

The exchange-traded fund (ETF) market has now surpassed $2 trillion, and analysts forecast it still has much more room to grow. So who is behind the momentum of this ever-increasing industry? Perhaps, surprisingly, Millennials are a big part of it.

The ETF is actually something of a Millennial itself, having turned 25 earlier this year and come of age during the era of the Internet, mobile computing and social media. So part of the appeal of ETFs for the Millennial crowd might be that, for a generation accustomed to broadcasting their personal lives to the world, the transparency of ETFs is appealing. Or it could be that growing up at a time when information is instantaneous, global and ubiquitous, young investors now seek to broaden their reach across countries, sectors and asset classes, which ETFs provide. Or it might be that in a culture of instant gratification, Millennials appreciate the intraday liquidity of ETFs.

Another critical influence is the impact of the market crash of 2008 and the ensuing Great Recession, which had a particularly painful effect on this generation at a critical time in their careers. Studies have shown that 88 percent of millennials are more likely to live within their means and 74 percent say they are more comfortable saving and investing extra money than spending it. The low cost of ETFs might appeal to this frugal aspect of Millennial thinking.

Another potential reason for Millennials’ role in the growth of ETFs is simply that it’s easier and more appealing than ever to invest. A wide array of companies offer innovative ways for new investors to create a diversified portfolio, offering low fees and catchy marketing hooks to attract – and grow – investment dollars. We researched some of the most clever platforms that all Millennials (and financial advisors) should be aware of.

Investing Spare Change

Acorns is a free app that invests the spare change from everyday purchases into a diverse set of investments. It rounds up the differences of your transactions and moves the cash to the Acorns account to create a steady inflow to the user’s investment portfolio. With less than a year of history, it has already transacted more than 20 million trades which represent more than $10 million of funds. Much of the credit goes to Nobel Prize-winning economist Dr. Harry Markowitz, who is behind the investment portfolio choices. As the fund grows, we hope to see the app expand its portfolio into more diverse asset classes.

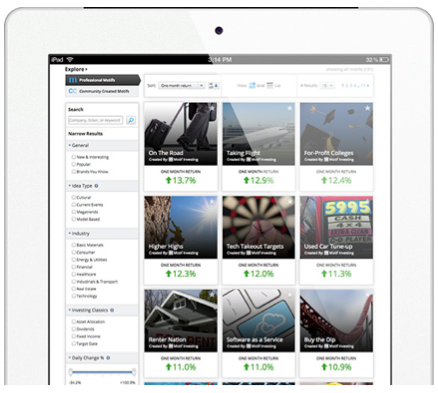

Motif allows the user to build customizable baskets of up to 30 stocks or ETFs that represent a unique industry trend, trading strategy, financial goal or personal value. They also offer 150 pre-made motifs to choose from. They charge a flat $9.95 per motif that you choose to invest in. Motif was started by a former Microsoft Executive and funded by Goldman Sachs.

Motif is appealing to Millennials due to its low fees and its investors’ ability to customize their portfolios according to which sectors “motifate” them to invest.

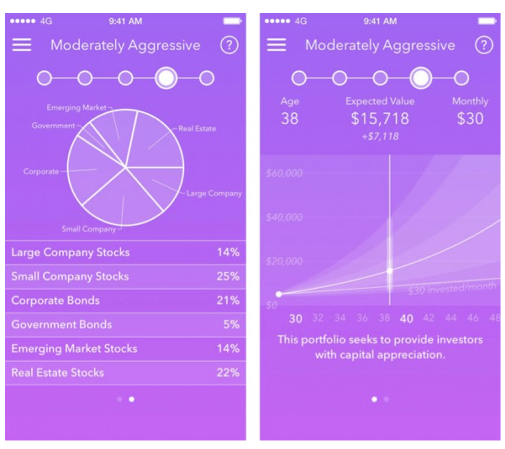

WiseBanyan is the world’s first free financial advisor. That raises the immediate question: how do they make money? The answer is that their premium customized portfolio management service charge an annual fee of 0.50%-1.0%. WiseBanyan has become so popular that there is even a waitlist to join. Although WiseBanyan has no hidden charges, the ETFs they recommend do charge annual fees. They also only require $10 to get started. Hopefully that will make Millennials think twice about that extra beer at the baseball game.

While much of the attention is rightfully focused on the technology underpinning these new investing platforms, Hedgeable is most notable for offering perhaps the most sophisticated investment strategies in the automated advisor market today. It differentiates itself from other robo-advisors by focusing on bringing techniques used by wealthy and professional investors – such as downside protection, alternative investments, and tax loss harvesting – to the masses. That means investors have access to ETFs beyond the largest and most mainstream index funds, including strategic and alternative funds that may help diversify portfolios. Hedgeable also employs a proprietary technology it says mitigates risk and offers downside protection, so when markets are in a downturn the system gradually sells positions in an attempt to limit losses. There is no minimum investment, but the fees are slightly higher than the competition.

Ride the Tide

Millennials and ETFs have grown together to become juggernauts in their own right. Advisors, retirement plans and technology will need to quickly start incorporating their preferences. In fact according to the 2015 Trends in Investing Survey by the Journal of Financial Planning and the FPA Research and Practice Institute™, ETFs now surpass mutual funds in popularity. This marks the first time since the survey was first completed in 2006 that ETFs have assumed the role of preferred investment vehicle among advisers, with 81 percent of financial advisers surveyed currently using or recommending ETFs with their clients—the most popular investment vehicle among 17 options. Clearly the Millennial mindset has advisors on notice and they are responding.

It takes an income of about $106,500 a year to be in the Millennial “one percent,” according to data from the U.S. Census Bureau’s Current Population Survey. That’s a group of about 720,000 young adults, and they control about double the income of the 14 million Millennials in the bottom 20 percent – do the math, that’s a large pool of investors who potentially will demand ETFs. And for advisors who fail to embrace this once emerging asset class as here to stay, they may miss the proverbial boat.

Meanwhile, robo-advisors and investing apps are causing a disruption in the investment world. However, they can never replace the value of human contact that comes with an advisor. And as young investors grow their portfolios using these new technologies, they will eventually seek out advisors who can tailor a financial plan and investment portfolio to their unique needs. That’s great news for advisors who are fluent in ETFs, as they will have a generational tide of investors who have been saving and investing more prudently, and in greater numbers, creating massive pools of assets in search of sophisticated financial advice.

Ken Han is Associate Portfolio Manager at Reality Shares. This article represents the opinion of Han and may not represent the view of Reality Shares.