And the votes are in… The people made their decisions and cast their votes, electing President Donald J. Trump and Vice President Mike Pence. Despite the partisan gridlock in our capitol, there is strong bipartisan agreement on the need to reform the federal tax code.

Winning the White House does not necessarily mean the President-elect has an easy path from tax proposal to enactment. Regardless, congressional tax writers and proponents for tax overhaul are optimistically planning to move bipartisan tax legislation forward in early 2017 given the stated support from both lawmakers and the new President-elect.

Trump Administration Tax Plan

The Trump Administration’s Tax Plan would reform the federal tax code by reducing marginal income tax rates for all individuals and businesses, increasing standard deduction amounts, repealing personal exemptions, capping itemized deductions, repealing the individual and corporate alternative minimum taxes (AMT), repealing the 3.8 percent net investment income tax (NIIT) and repealing the federal estate tax. However, as detailed below, some ambiguities still remain, especially with regard to the estate tax and pass-through business income tax proposals.

Individual Income Tax Proposals

- Create three ordinary income tax brackets of 12 percent, 25 percent and 33 percent, maintaining the current capital gains tax rates of 0 percent, 15 percent and 20 percent.

- Increase the standard deduction from $6,300 to $15,000 for single filers and from $12,600 to $30,000 for married couples filing jointly, eliminating personal exemptions.

- Cap itemized deductions at $100,000 for single filers and $200,000 for married joint filers.

- Repeal the individual AMT and the 3.8 percent NIIT.

- Tax carried interest income at ordinary income tax rates.

Transfer Tax Related Proposals

- Repeal the estate tax, establishing in its place a carryover basis for appreciated capital gain property, with an exemption amount of $10 million.

- Disallow an income tax deduction for contributions of appreciated assets into a private charity established by the decedent or the decedent’s relatives.

Business and International Tax Proposals

- Reduce the corporate income tax rate from 35 percent to 15 percent, with the reduced tax rate “available to all businesses, both big and small, that want to retain the profits within the business.” It is unclear whether to interpret this to mean that the 15 percent tax rate would apply to all business income or only to businesses that are organized as C corporations, with the ordinary individual tax rates applying to the income of pass-through businesses, such as partnerships and S corporations.

- Eliminate most corporate tax expenditures except the research and development credit.

- Imposes a one-time 10 percent deemed repatriation tax on corporate profits held offshore, ending the deferral of tax on profits held offshore, which under current law are not subject to U.S. tax until they are repatriated.

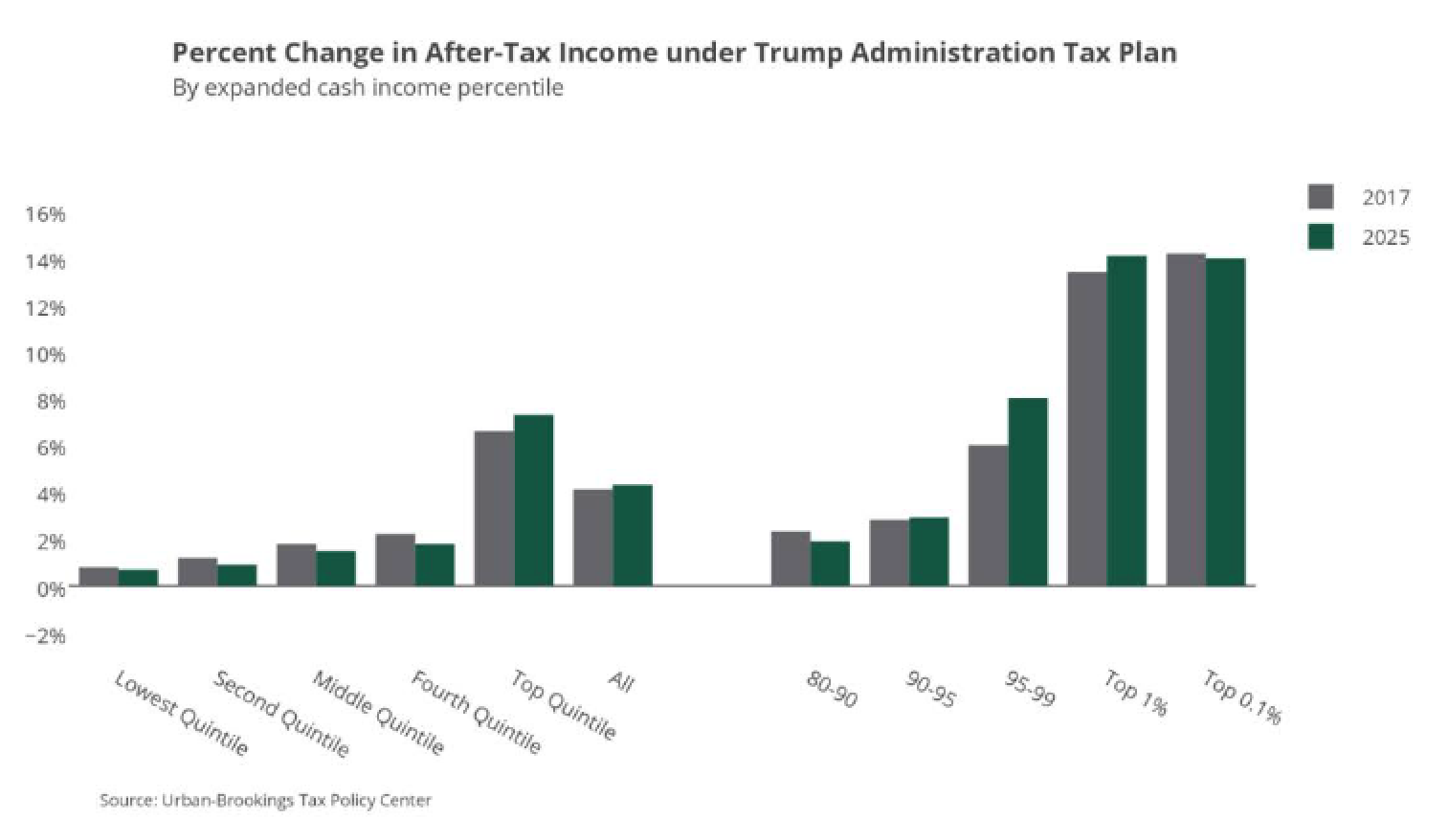

President-elect Trump’s proposed tax changes are estimated to reduce federal tax revenue by $6.2 trillion between 2016 and 2026, increasing the federal debt by approximately $7.2 trillion (including interest) over the same period if not offset by spending cuts. Under the Trump tax plan, nearly all taxpayers would see a reduction in federal taxes in 2017 and thereafter. Taxpayers with household incomes between $143,100 and $292,100 would see an average tax decrease of approximately $4,310. Those with incomes over $3.8 million—the top 0.1 percent—would see an average $1.07 million decrease in federal tax in 2017.

House GOP Tax Plan

Republican leaders of Congress have also chimed in on tax reform, releasing a consensus blueprint for comprehensive tax reform on June 24, 2016. The House GOP tax plan would overhaul major components of the current tax code, lowering taxes across the board for individuals and repealing the 3.8 percent NIIT, estate and generation-skipping transfer taxes. In addition, House Ways and Means Committee Chairman Kevin Brady (R-Texas) and Senate Finance Committee Chairman Orrin Hatch (R-Utah) have both stated their readiness to move forward with bipartisan tax reform. The key details of the House GOP tax plan are:

Individual Income Tax Proposals

- Create three brackets with rates of 12 percent, 25 percent and 33 percent, replacing the current capital gains tax rates with a 50 percent income tax deduction for net capital gains, dividends and interest income.

- Increase the standard deduction from $6,300 to $12,000 for single filers and from $12,600 to $24,000 for married couples filing jointly.

- Eliminate the personal exemption, all itemized deductions except for the mortgage interest deduction and the charitable contribution deduction, the 3.8 percent NIIT, the additional 0.9 percent payroll tax, the medical device tax, the health insurance tax and the individual AMT.

Transfer Tax Proposals

- Repeal the estate and generation-skipping transfer taxes. Some modeling projections of the revenue impact of the proposal have assumed carryover basis for appreciated property, but this has not been definitively resolved.

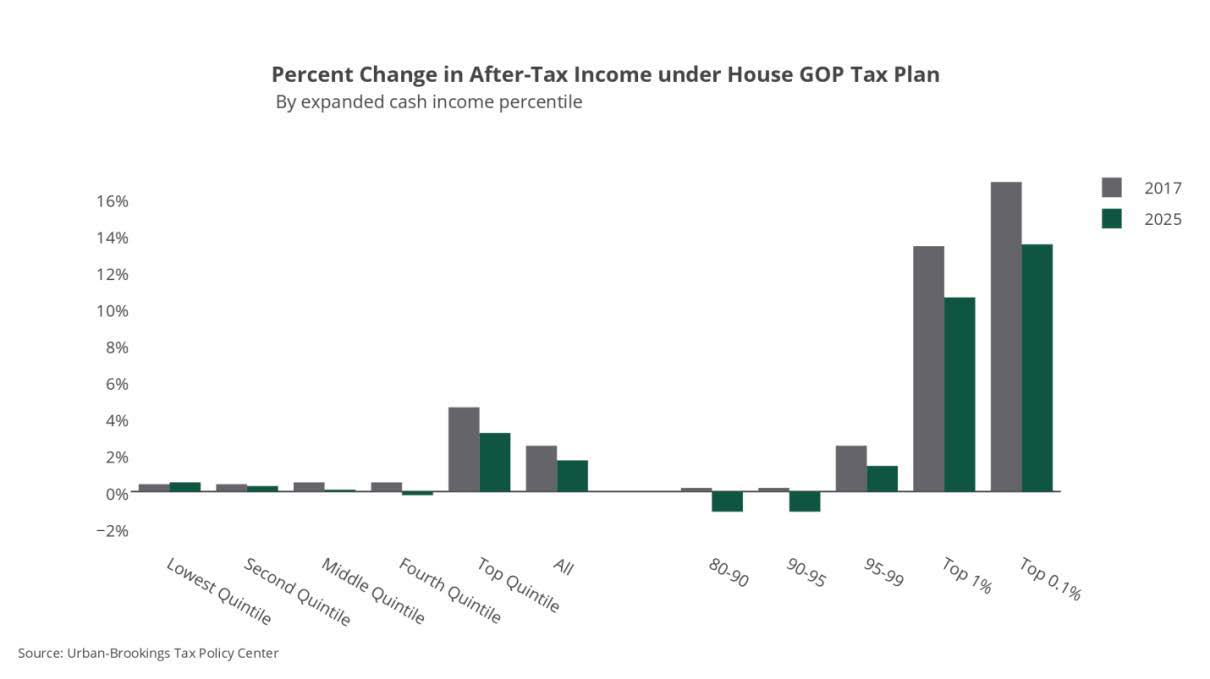

The House GOP tax plan’s changes are estimated to reduce federal tax revenue by $3.1 trillion between 2016 and 2026, increasing the federal debt at least $3 trillion (including interest) over the same period if not offset by spending cuts. Under the House GOP tax plan, all taxpayers would see a reduction in federal taxes in 2017 and thereafter. Taxpayers with household incomes between $143,100 and $292,100 would see an average tax decrease of approximately $340. The top 0.1 percent would see an average $1.2 million decrease in federal tax in 2017.

The Long Road Ahead

Even with a Republican-controlled Oval Office and Congress, President-elect Trump will first need to work with the House GOP to converge their respective tax reform plans into one before moving forward with legislation. Tax legislation will still likely face resistance from House Democrats. Nevertheless, Republican and Democratic leaders in both houses of Congress are optimistic that comprehensive tax reform will progress in 2017. There is a long road from proposal to enactment, and unless the leaders in the capitol are able to work together to advance tax reform, the status quo will likely remain for the foreseeable future. At this point we can only plan for uncertainty, maintaining needed flexibility and agility.

Suzanne L. Shier is the Wealth Planning Practice Executive and Chief Tax Strategist/Tax Counsel and Benjamin J. Lavin is a Wealth Planning Strategist/Associate Tax Counsel for Northern Trust.