In October of 2009, life as a Citigroup bank broker was turned upside down. That's how the Citi reps describe it, anyway. It all started in June, when the bank brokers were cut loose from Smith Barney. The Morgan Stanley Smith Barney joint venture didn't include them. And with Smith Barney went its coveted investment platform, too. Then, in October, the other shoe dropped. Citi management announced that Citi bank brokers would no longer be bank brokers; they'd be fee-only investment advisor reps who, by 2011, would no longer be permitted to receive commissions. The crowning insult? They'd have to work in teams of seven or more — or take a pay cut. And they found out that they'd be competing with outside RIAs for the bank's referrals. Deborah McWhinney, the head of Citi Personal Wealth Management, was creating a preferred list of outside RIAs to refer bank clients to — for a fee. Just as they do over at Charles Schwab, where McWhinney toiled for seven years heading up its RIA business.

Of course, none of that is sitting well with the bank branch brokers, many of whom have left the firm. But some analysts say that may be the point — Deborah McWhinney's actual endgame.

When troubled Citigroup spun off a 51 percent stake in its 11,000-FA Smith Barney retail advisory unit to Morgan Stanley to raise some cash, it left a gaping hole in the bank's wealth management offerings to affluent households. McWhinney was hired as head of Citi Personal Wealth Management (as the bank brokerage is now called) three months after the joint venture was announced. She appears to be attempting to overhaul the way the unit operates.

When the change in strategy was announced, Terri Dial, the then-head of North America Consumer Banking and Global Consumer Strategy (who has since moved on), said in a statement, “Moving to an investment advisory model is the right decision for our clients and for Citi. This model is where the market is headed and it will help us offer clients greater flexibility, transparency and meaningful investment choices. This change is about keeping our clients at the center of all we do and providing them with the investment advice they're looking for and the services they need.” The strategy will apparently not affect Citi Private Bank, which currently employs about 130 private bankers and serves clients with $25 million in net worth or more.

McWhinney is no stranger to the fee-only world, of course. After two decades at Bank of America, she headed up Schwab Institutional's RIA custody unit from 2000 to 2007. Under her watch, Schwab Institutional became an RIA platform giant, hitting some $500 billion in custodied RIA assets. Those who worked with McWhinney say she can be credited with segmenting Schwab's RIA base and creating “tiered services” that gave more customized services to larger investment advisors and less personal attention to smaller RIAs.

So Long

Now, her RIA experience has some bank brokers thinking she wants to “Schwab-ify” Citi Personal Wealth Management (PWM). Many are simply abandoning ship as a result.

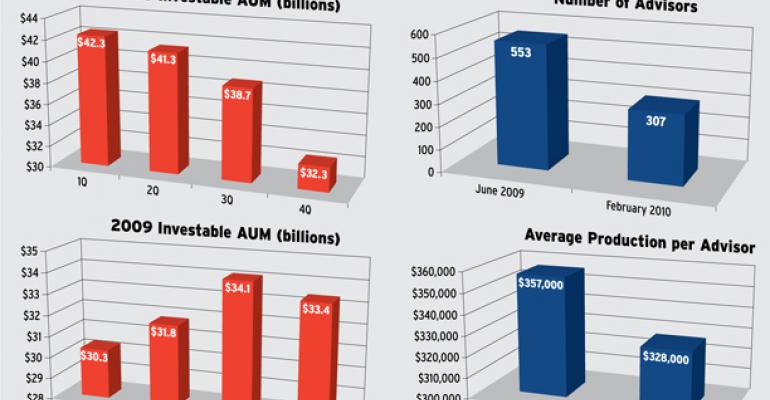

Indeed, nearly 45 percent of the firm's bank brokers have departed since June of last year, leaving just 307 (as of February 2010) scattered across 1,003 North American Citibank bank branches. So what exactly does Citi have in store for this harried group? Some say McWhinney is giving the unit a covert makeover, intentionally purging most of the bank brokers, a breed that does not tend to have the asset acquisition drive, or product sophistication, that big-time wirehouse or RIA advisors do. Put another way, she is outsourcing the retail financial advisory function to handpicked fiduciaries — much like Schwab does through its branches. Under this scenario, Citi would collect a fee — something like 25 basis points on assets referred to outside RIAs.

“Putting brokers in bank branches is almost never successful,” says Dick Bove, a bank analyst with Rochdale Securities. That's because retail banks simply aren't associated with high-end investment advice, he says. “It rarely works. That system has to be shaken up, and creating a new system for investment advice at the bank might work for Citi,” he says.

Either way, the current changes are bad news for many of the bank brokers, and it's causing major animosity toward McWhinney. One broker who averages about $300,000 in production, (we'll call him Jimmy) says when he and fellow advisors found out they weren't part of the joint venture their main concern was losing the Smith Barney platform and the research that came with it. “But so much has happened since that news that losing the Smith Barney platform seems like the least of our problems.” He adds, “[McWhinney] doesn't care about our group. She doesn't listen to top advisors or advisors period. She has an agenda and doesn't want to hear what we have to say about it.”

McWhinney declined repeated requests for an interview, but Citi did make available Tim Williams, managing director of field management and services at Citi PWM. Williams says the firm absolutely does not intend to get rid of the bank brokers. “We are committed to the bank channel and we've demonstrated that by investing heavily in our people and client-centric model,'' he says. In fact, since the initial announcement, Citi seems to have back-pedaled a bit: The firm is still moving toward an advisory model, but now advisors can do commission business where it makes sense for the client. It just shouldn't be their main calling card, he says. “Citi and our wealth management business have dealt with a lot over the past couple of years,'' he says. “We know we needed to make changes, and that included putting client relationships front and center, and this is exactly what we're doing.''

Citi advisors are not happy with this explanation. The rank-and-file Citi brokers fear that transactions will be so frowned upon by management as to be just short of forbidden. One Citi bank broker with about $800,000 in production calls McWhinney and Williams “a losing team” that “never got together with the biggest producers to ask what we thought about the changes being made. They just implemented these rules and said, ‘Do it.’” Another advisor and his partner say McWhinney doesn't even respond to queries left for her on “Ask Debby” website. (“There is always a ‘system problem,’” they grouse.) Williams counters that McWhinney holds regular conference calls, town halls and smaller meetings with FAs, and does take advisors' suggestions into consideration. “As for emails, no system is perfect, but ‘Ask Debby’ is an important communications channel for us. Many FAs use it regularly, and we've benefited from the ongoing dialogue,” he says.

Another Citi advisor out West acknowledges that fee-only has some advantages: fees are more transparent than commissions. But they only make sense for some clients, he says. Most Citi advisors have smaller clients who would be better off paying a commission. He argues that fee-based advice would raise costs for smaller investors and could amount to reverse churning. After all, under McWhinney's plan, transactions will pay out less and fees will pay out more — that may create conflicts since fees may not be in the interest of some clients. For example, it doesn't make sense to charge ongoing fees to build a bond ladder, he says. “She is just trying to rush the pure RIA model on us,” he complains, because that's the culture from which she sprung.

Regardless, some say that the hybrid model — offering both transaction business and RIA-like advice as needed — is ascendant. The hybrid model is currently supported by firms like Pershing, Fidelity and LPL, for example, to name a few. Perhaps Citi is headed in that direction, ultimately.

Then there is the team initiative. McWhinney announced in October that Citi bank brokers should work in teams to increase their productivity. It doesn't sound like such an appalling idea on the surface, but those who don't join teams will see a drop in their payout. For example, the payout on transaction business for an advisor who is not on a team is 25 percent, while advisors that are part of a team are paid 35 percent on the same transactions. One Citi broker with almost a million in production says, “I'm getting 35 percent on commission business now, because I'm on a team. But by 2011 commission business will probably be gone. If you're not wrapping your business, you'll be out of business at Citi.”

One team that was formed at the onset of the October announcement had a combined AUM of almost $2 billion among roughly 10 brokers. By mid-March, five brokers had departed to the likes of UBS and Wells Fargo Advisors, leaving the team with about half a billion. One of the advisors who is still on the team says he's in talks with Wells Fargo, Merrill Lynch and UBS about making a move. “We're a bank channel and [Citi] brought in someone from Schwab. What do you expect?” he says. He adds, “You can't force people into teams and tell them all of a sudden they're fee-only advisors. I built my book alone, and I don't want to share it with anyone. And I don't want to wrap it for the sake of wrapping it.”

Perhaps the biggest irritation to the bank brokers is McWhinney's plan to refer banking clients not only to its own PWM brokers but also to a select group of outside RIAs. In return, the RIA would give Citi 25 basis points on the assets each year. Citi is currently vetting the list of RIAs it will choose to work with, but it's reportedly looking for established firms that are managing at least $250 million in client assets. The RIA referral program will kick off in the New York City and San Francisco metro areas this year.

Dennis Gallant, principal of consulting firm Gallant Distribution Consulting in Sherborn, Mass., says, “It's an interesting idea, but it certainly undermines your ability to build out your wealth management business internally when you're referring business to outside advisors.”

But again, some think that is exactly what McWhinney has up her sleeve. As Bove points out, maybe the lack of concern about losing almost 45 percent of your brokers combined with referring clients to outside RIAs means getting rid of a group that may not make much money anyway. “The issue isn't about brokers leaving. If they wanted to keep those people, wouldn't they have found a way to keep them somehow?” Bove asks.

For Jimmy, the Citi broker with $300,000 in production, and others like him, this is bad news. “Wow. I haven't really thought about [Citi] getting rid of all of us. But I guess that's something to think about. I already have one foot out the door,” he says. Another broker puts it this way, “It makes sense since they're not replacing the advisors who left. The million dollar question is at what point are there not enough guys in the program to even bother funding the program at PWM?” Citi says it is recruiting advisors for PWM.

The Fiduciary Problem Solved?

The Citi broker who referred to McWhinney and Williams as a “losing team” says he is convinced McWhinney was hired by Citi to figure out how to work with the fiduciary pressures coming from Washington. Whether or not that will emerge in any financial services regulatory overhaul is unclear. SEC Chair Mary Schapiro has stated in several speeches that she favors a fiduciary standard for all financial services professionals who deal with retail clients. But that could get costly for broker/dealers who engage in things like proprietary trading or investment banking. Nonetheless, McWhinney's efforts to farm out business to outside fee-only RIAs is a unique way for a bank of its size to address the fiduciary issues facing Wall Street firms, consultants say.

Williams says the PWM changes are mostly a matter of putting client needs first, but he admits that “throughout the industry there is a heightened awareness of the fiduciary standard of care. Whether that comes from competitive or regulatory pressures, or both, it is a trend that is gaining momentum and we are taking it to heart as we appeal to our clients.”

One former internal lawyer for Morgan Stanley says the RIA referrals make sense for Citi if it's looking to find a way to offer fiduciary advice and get paid for it. “They'll have to disclose the arrangement with the clients, of course,” he says. He also adds that if the model is a success, then Citi might want to consider getting rid of all the branch brokers.

As Tim Welsh, president and founder of wealth management marketing consultant Nexus Strategy in Larkspur, Calif., puts it, “If I'm the CFO of Citi, I'm thinking, ‘I don't have to pay these RIAs a dime but I'm getting basis points off the assets I refer to them.’” He says few management teams have the patience it takes to turn a traditional force of advisors into fee-only investment advisors. In the meantime, Citi has a huge base of banking clients that it needs to offer wealth management advice to. Welsh calls Citi's bank brokerage a “floating carcass” if changes aren't made — and the referrals to outside RIAs may be a saving grace, he says.

Like Welsh, Gallant says converting a traditional brokerage to fee-only can take a long time and “you know there will be a lot of folks who aren't interested and who will walk. Citi might be looking to prune the flock.''

The RIA referral structure will give Citi a steady stream of revenue on assets without the office overhead or the costs of building its own fiduciary model, Gallant says. The client leads are also great news for the RIAs on Citi's preferred list. “If you're an RIA, you absolutely want to be on the Citi list. The value of a new client is immeasurable. Sure you're paying an ongoing 25 basis points, but you're not doing the legwork required to find new clients. You're getting clients sent to your door with a checkbook in hand,” Welsh says.

For now, it seems McWhinney's RIA referral strategy will be something unique to Citi. Welsh says it's unlikely Wells Fargo or other banks will be referring business to outside RIAs since just about every other major firm has a brokerage force. Welsh adds, “It's a major shift in business for an entire unit to leap in the fee-only RIA world. There's been turnover and dislocation among the brokers, but if anyone can do it, it's Debby.”