Liquid alternatives grew in popularity following the crisis as investors came to view them as a bridge between portfolio diversification and an increased demand for liquidity. As we saw in the first part of this series, “Generation One” liquid alternatives failed to deliver on this mandate due to: i) structural underperformance relative to hedge funds; ii) high fees; iii) performance dispersion across funds. The shortcomings of Generation One have paved the way for “Generation Two” products to deliver on the promise of their predecessor.

Starting Point: How Institutional Investors Add Hedge Funds and Fill the “Bucket”

The goal of liquid alternatives is to provide investors with consistent, cost-efficient access to a portfolio diversifier. A looming question, however, is how “alternatives” like hedge funds get into a diversified institutional portfolio in the first place. In general, allocators rely heavily on return assumptions and quantitative models to determine the “optimal” portfolio allocation to stocks, bonds and other asset classes given a particular investor’s risk and return objectives.

There is no simple way to invest in the hedge fund “bucket” given that the indices consist of hundreds (sometimes thousands) of individual, illiquid hedge funds. Institutional investors, or their advisors, instead will select a portfolio of hedge funds with the objective to match or outperform the hedge fund bucket over a market cycle. In order to reduce tracking error to the index over time, investors need to reduce idiosyncratic fund risk by spreading their bets over dozens of funds.

How Hedge Fund “Replication” Offers a Proven “Generation Two” Solution

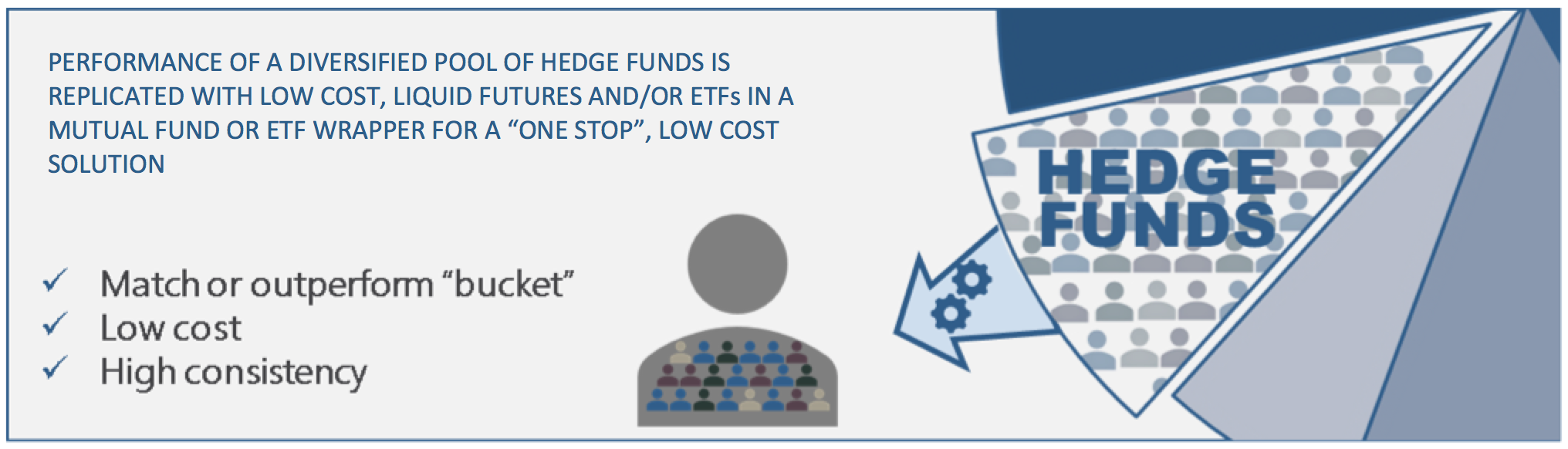

Hedge fund replication represents an efficient alternative to the complexity of filling the hedge fund bucket. Specifically, replication seeks to identify the core (market) drivers of performance of hedge fund strategies and invest directly in liquid and transparent instruments (futures, ETFs, etc.) to deliver comparable results. Replication strategies have several features that align with the Generation Two objectives; namely they:

- Seek to match or outperform a diversified pool of hedge funds (outperformance usually comes from targeting pre-fee returns with a much lower fee structure).

- Work seamlessly within the constraints of mutual funds, UCITS funds, ETFs or similar vehicles.

- Closely match the performance of the target pool of hedge funds (e.g., eliminate underlying manager risk).

- Have an efficient fee structure.

How would this work in the Generation Two framework? The graphic below shows how a single replication-based fund can meet the allocation objectives:

Replication-based strategies have been around for 10 years, and the obvious question is how they have performed relative to actual hedge funds. In order to show comparable results, we use two bank-sponsored replication products that have been continuously offered over the past decade to avoid any question of back-testing. Since replication products have daily liquidity, we compare the results to both the illiquid HFRI Fund of Funds index (an accurate representation of asset-weighted portfolios) and liquid HFRX Global Investable Hedge Fund Index. To make the numbers comparable from a net-of-fee basis, we deducted 0.75 percent per annum from the replication products, although we did not make a comparable adjustment to the HFRXGL. Over the past 10 years, two bank-sponsored replication products outperformed the HFRI Fund of Funds Index by a cumulative 7.7 percent on average and outperformed the HFRX Global Investable Hedge Fund Index by a cumulative 27.2 percent on average. Furthermore, the replication products had comparable standard deviation and lower drawdowns during the 2008 crisis. From the perspective of an allocator, stable outperformance with lower drawdowns is highly valuable.

Conclusion

Hedge fund replication remains controversial among institutional investors. However, after 10 years of results, critics of replication have been forced to acknowledge several key conclusions. First, replication does not systemically underperform hedge funds. In fact, with a 300 bps head start on fees, the products typically outperform. Second, replication is lower risk than hedge funds — no gating risk, no unexpected drawdowns during a liquidity crisis like 2008 (when the illiquidity premium went negative), and no single stock crowding risk (a big reason replication outperformed leading hedge funds in 2015-16). Third, the sources of “alpha” that are not “replicable,” primarily stock selection and illiquidity, are insufficient to warrant the 2/20 fee structure.

Today, as reality has set in on some of the limitations of Generation One products, allocators are looking for more reliable, cost effective, longer-term solutions. Whether through replication or other means, Generation Two must focus on outcomes and realistic results, preferably those backed by a decade or more of concrete evidence.

Andrew Beer is Managing Partner and Co-Portfolio Manager, Dynamic Beta at Beachhead Capital Management, a hedge fund replication strategist with more than $500 million under management.