Jeremy Grantham, GMO’s chief investment strategist, kicked off Morningstar’s annual investment conference in Chicago warning that equity markets are overvalued and “creeping nicely and slowly toward bubble land,” but that we weren’t there yet. Rapacious capitalism, buoyed by the Federal Reserve’s easy money policies, is to blame.

Grantham’s investment philosophy is based on a belief in reversion to historical means – valuations in the market will cyclically get out of whack, but always revert to a long-term historical average.

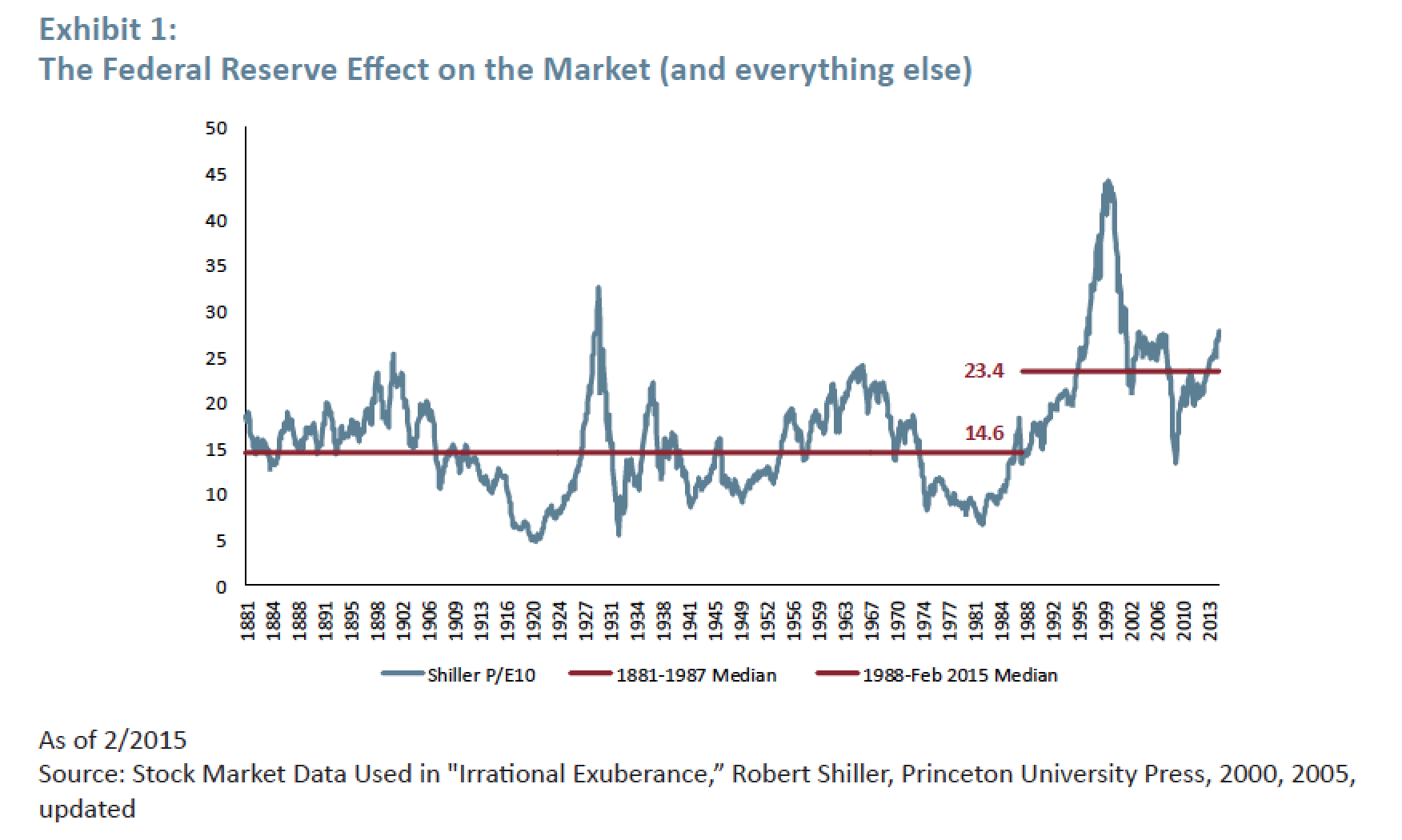

That’s been a tougher argument to make in the face of an extended bull market, he admitted. Currently, he pointed out, the price-to-earnings ratio in the S&P 500 is 21.1. It’s historical average is 16. Likewise, the current level of corporate profit margins is 7.3 percent; the historical mean is 5.7 percent. “Remember, the market tripled in the past six years. It’s not unlikely that it’s overpriced.”

Predicting an imminent pullback is one Grantham has been making for a few years now. The problem, Grantham pointed out, is that the metrics “have been abnormally high and have yet to regress.”

“So the question is, why has regression slowed and everything becomes sticky?”

He blamed in part a shift in the Federal Reserve of the 1970s and 1980s to the era of Greenspan, Bernanke and Yellen. “All three of these chairs have publicly bragged about their role in creating the “wealth effect” by pushing up stock prices. They admit they manipulate the market.”

Consider that the average P/E ratio on stocks is 60 percent higher since 1986 than it was prior:

{kind=link}

Profit margins too are 40 percent higher than they were in the pre-Greenspan era.

“This is not an insignificant shift,” he said. “It makes the bulls look good and clairvoyant.” The market, he estimated, would need a 57 percent drop to get back to mean averages of the earlier Fed regimes.

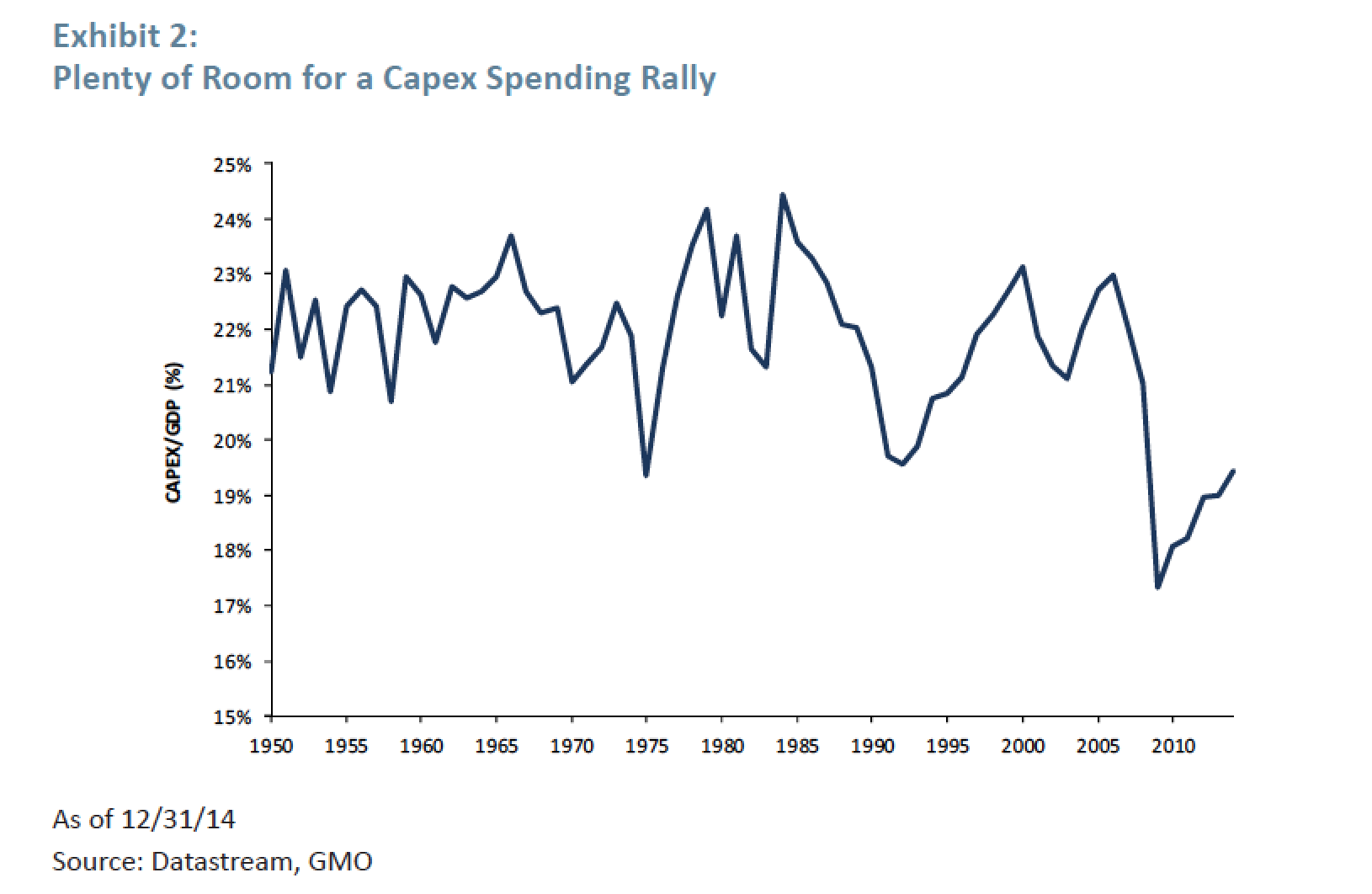

The era of easy money is also fueling a “stock option” culture in corporate America which incentivizes corporate managers to inflate short-term profits and higher market valuations by buying back stock instead of on capital expenditures.

Stock repurchases are running at a $700 billion annualized rate year-to-date. “Back in the 1960s and 1970s, companies were driven by market share. Everyone wanted to dominate their industries. That’s great for capitalism, bad for profit margins. Now, the Fed has artificially lowered interest rates. Debt is cheap. It’s more profitable for corporations, and desperately appealing to buy back stock.”

Companies aren’t spending the easy money on factories or expanding their businesses, he pointed out. Capitalization expenditures are four percentage points below average, despite six years of roaring markets.

{kind=link}

“I’m trying to understand the efficiencies in capitalism,” Grantham said. “There is nothing to treat the long-term harm to the public common. Now it’s profit maximization, and to hell with other stakeholders.”

“You get mean revision if capitalism happens in the normal way,” he said. “But we’re not allowing profit margins to mean revert. For 20 years, we’ve had abnormally high returns. All we’re doing is buying back our own stock. We’re not even responding. We’re not expanding our economy. We’re running away from it to protect our stock options.”

Despite the lofty valuations, Grantham said we are not in bubble territory yet, and the market could move higher. For a bubble, we need markets that have more “oomph” and speculation, when the economy is “screaming with overcapacity,” and we’re not there yet. “What we need is a trigger. Broad overvaluation has never done it. We need to wait until deals become more of a frenzy.”