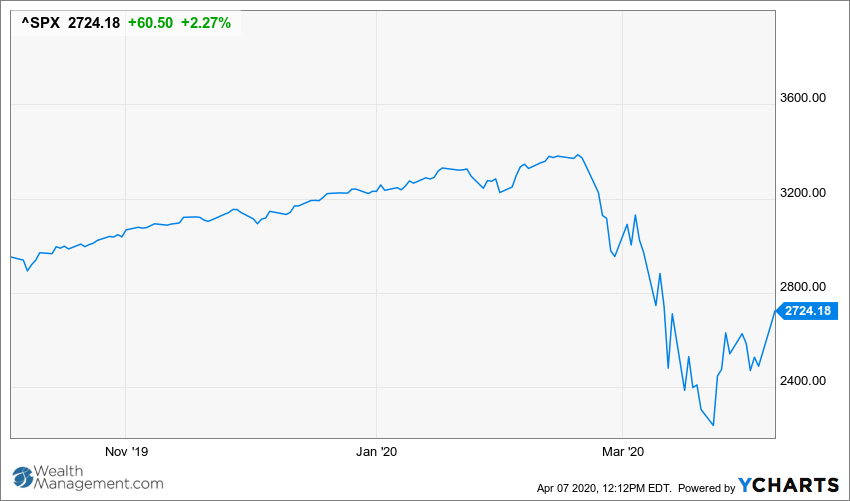

(Bloomberg) -- Fifteen days ago, the S&P 500 was mired in a bear market, 34% from its February peak. On Tuesday, at least technically, it rocketed into a new bull market.

The benchmark for American equity rose 1.2% as of 11 a.m. in New York, taking it 20% above its March 23 low. If the rally holds and it closes above that threshold, it will meet the time-honored definition for the start of a bull market. It accomplished the feat just 48 days after the end of the longest such run on record, marking one of the shortest bear markets in history.

The velocity of the rebound mirrors the speed of the plunge, calling into question the staying power of the gains. Bounces of similar magnitude happen from time to time in fast-moving markets and aren’t taken seriously by market historians until they stick. The S&P 500 is still almost 20% below that February record.

“We’ve seen the lows. Now, will they be tested again? There’s a distinct possibility they may,” said Arthur Hogan, chief market strategist at National Securities Corp. “But do they have to? No.”

Regardless of the statistical milestone, volatility is likely to remain. The VIX is stuck above 40 and the S&P 500 has swung 4.8% a day on average since the start of March. Testament to the nuttiness is that Tuesday’s gains came after a 7% rally, and before this year the index hadn’t jumped 5% in a single day since the financial crisis.

Many are quick to highlight that sharp rallies are hallmarks of bear markets. After all, within 14 bear markets passed, the S&P 500 has rallied more than 15% on 20 separate occasions before falling back toward, or through, the lows.

“The conditions for it to be the end of the bear market or the end of the dip would be if we can see a path forward to companies earning again,” said Kim Forrest, chief investment officer of Bokeh Capital Partners. “It has the potential for staying power. There’s always the possibility for temporary bad news. Does it change the fundamentals? I don’t think so.”

But the latest rout, induced by a viral outbreak that’s forced economies around the globe to shutter, has been unique. Notably, the speed of the decline compares to no other experience. According to Jim Paulsen, chief investment strategist for the Leuthold Group, the rate as which stocks fell into a bear market this year was 6.5 times faster than what’s usual.

Paulsen is still expecting at least a re-test of the initial lows as economic data in the coming weeks illustrate an economy in collapse, but he encourages investors to be aware of this one-of-a-kind scenario.

“Investors should be mindful of the ‘warp speed’ of this debacle across the financial markets,” he wrote in a note Monday. “Without precedent, this recession was almost immediately predictable; therefore, stock, bond, and commodity markets have probably discounted far more of the total downside risk than would be traditional at this point.”

The Dow Jones Industrial Average was first to claim the 20% mark on March 26. The tech-heavy Nasdaq 100, on the other hand, is only up 18% from its lows, although it fell the least of the three benchmarks on the way down.

The equity recovery has also been global, with Tuesday’s rally bringing the MSCI All-Country World Index to 21% above the low it reached last month.

Due to the fluidity of the coronavirus, analysts, strategists and economists alike have had a difficult time forecasting what’s to come. A measure of earnings estimate dispersion shows sell-side analysts have almost never been more divided on what corporate profits will look like when earnings season begins in a week. Top-down strategist forecasts for where the stock market will venture to next span the gamut.

But even in more common times, a debate stands over how to classify bear and bull markets. The uniqueness of this event only complicates the matter further.

“I understand that you need to have some definitions -- and 20% up and 20% down are as good as any others -- but clearly it doesn’t always capture the essence of what a bull market or bear market really is,” said Chris Zaccarelli, chief investment officer at Independent Advisor Alliance. “The entire event has been so outside the realm of what you normally see in markets and economic cycles that it calls into question whether ‘normal’ definitions of bull and bear markets make as much sense in this context.”

To contact the reporters on this story:

Sarah Ponczek in New York at [email protected];

Vildana Hajric in New York at [email protected]

To contact the editors responsible for this story:

Jeremy Herron at [email protected]

Brendan Walsh