With value opportunities shrinking in the domestic bond market, we think nimble and opportunistic investors should consider taking a closer look at emerging markets, particularly high-quality U.S. dollar-denominated corporate bonds, for potential value. After a challenging year in 2013, emerging markets are once again under pressure. A multisector approach that takes a bottom-up, fundamental view of the credit markets may be helpful in finding potential opportunities in beaten-up emerging markets where selectivity is important.

Why emerging markets now?

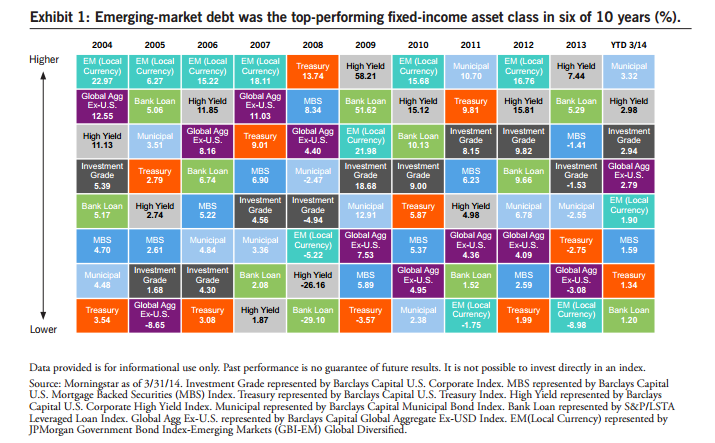

While many risk-minded investors may want to avoid the turbulence of these markets, we recognize that uncertainty and volatility are often accompanied by value. For the better part of the past decade, emerging-market debt was viewed as a sector play; investors wanted broad exposure to the outsized yields of the asset class. As Exhibit 1 shows, local currency emerging-market debt led asset class returns six times from 2004 to 2013, with only three years of negative returns.

The case for being nimble in 2014

Nimble is traditionally defined as being responsive or having the ability to move quickly and easily. We think investors should strive to be nimble, which we define as having the ability to quickly turn ideas into portfolio positions. We believe a key factor for 2014 will be having the liquidity to put to work as growth exceeds expectations and the markets readjust in response.

After taking on debt that allowed them to build and grow, many of these countries are starting to feel the pinch of higher rates here in the U.S. Emerging-market fundamentals deteriorated sharply after the Federal Reserve (Fed) announced a tapering of its asset purchases in May 2013, putting many of these markets under considerable stress. Recent negative headlines of various geopolitical issues have only made emerging markets appear more unattractive and potentially riskier to investors:

- A string of weaker-than-anticipated economic releases out of China have raised some concerns about an economic slowdown and the potential need for stimulus.

- Russia’s increased action in Ukraine and Crimea has increased tensions with the U.S. and other western countries.

- Turkey is mired in an ongoing political crisis, and clashes in Syria threaten to spill over across the border.

- Deep economic problems in Venezuela persist and have resulted in violent protests.

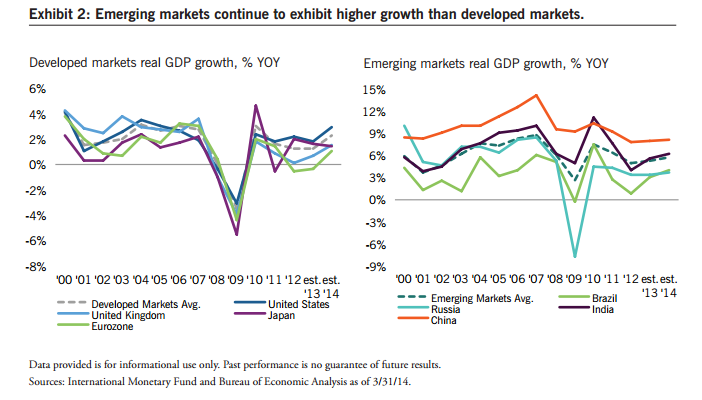

As contrarian thinkers, these issues have captured our attention. Growth rates in emerging-market countries may be slowing, but they still outpace developed markets, as Exhibit 2 highlights. Rather than assuming broad exposure to emerging markets (EM), we think it is more important to consider differentiation and finding select opportunities in the EM space.

How investors may employ a multisector bond strategy in emerging markets

One of the hallmarks of our multisector approach to the bond markets is the desire to trade interest-rate risk for credit risk. In the U.S., yields have begun to rise and spreads over Treasurys are compressed below average historical levels, making it harder to find attractive income opportunities that also avoid unwanted interest-rate risk.

Emerging-market debt, on the other hand, has gotten cheaper due to the sell-off over the past year. This comes as investors have begun to price in not only the end of the Fed’s quantitative easing (QE), but an eventual rise in the Fed's base rate, effectively raising the bar on the so-called carry trade on emerging-market currency short-term yields. Historically, central banks in these emerging countries will step in and raise short-term rates in order to defend their currencies.

We believe we are at the beginning of this cycle, where a decline in an emerging-market currency makes domestic goods from that country more competitive in world markets. We maintain that there is a tremendous amount of sovereign and political risk, so as a way of gaining exposure to the unloved emerging markets, we have been focusing on fundamentals of corporate issuers in EM countries. In other words, while we don’t advocate diving into the pool of emerging markets, we think it makes sense to consider dipping a toe in the water with individual corporate credits.

We think there is opportunity in emerging-market corporations with diversified businesses that have a reach beyond their home market, which potentially insulates them from the country or political risk. Given where we believe we are in the aforementioned cycle, we think it is prudent to consider the amount of currency risk. However, as the cycle develops, we think investors should consider examining areas the market may be undervaluing, including emerging-market currencies.

To sum it up, we believe that a multisector approach based on bottom-up, fundamental analysis may help to uncover potential opportunities that provide us with a yield advantage and diversification away from U.S. interest-rate risk.

Opportunities still remain in the U.S., but selectivity is important

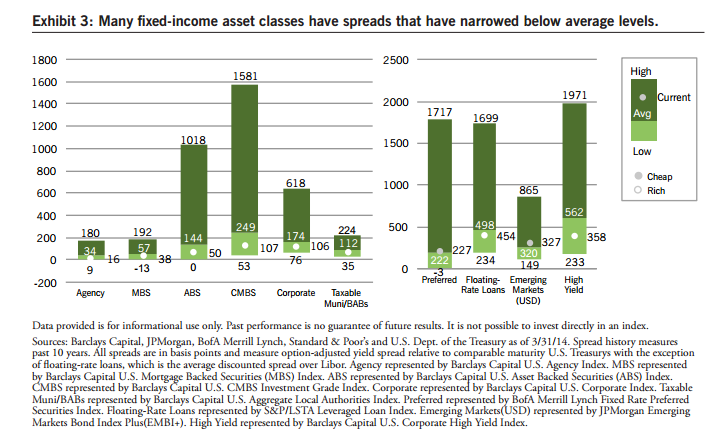

As we mentioned, spreads over Treasurys in U.S. credit markets are compressed — in fact, the absolute level of yields is below average levels for asset classes like investment-grade corporate bonds, high-yield debt and floating-rate loans, as Exhibit 3 (below) shows. In our view, there appears to be a lot of interest-rate risk in traditional credit markets. This is a result of the Fed’s QE programs reducing systematic risks.

Our multisector approach focuses on less-efficient, nontraditional fixed-income groups that have low correlation to Treasurys, which has led us to several alternatives to expensive investment-grade debt. Although spreads continue to get tighter, we see opportunity in preferred securities and convertible bonds giving us equity flexibility that comes with large-cap, high-quality issuers.

Stay opportunistic and flexible in today’s markets

A multisector approach to bond investing requires investors to be nimble, opportunistic and global, in our view. We’ve seen this play out over the past several months; for example, high-yield debt appeared attractive to us early in 2013 when spreads still had room to compress. More recently, we have seen opportunities in equity-related income assets as an alternative to richly priced investment-grade fixed income. Now, we think the next place for bond investors to consider is emerging markets. All of this highlights the need to be nimble, opportunistic and global to take advantage of these shifting opportunities.

The key to investing in both U.S. and emerging-market securities is selection, finding opportunity in an unfavorable sector. This brings us to the important caveat that investors must keep a very careful eye on valuations. The individual names are what make the U.S. and emerging-market corporate sector attractive to us. Investors need to judge whether they are getting compensated enough for the credit risk, and they may benefit by letting a professional, experienced manager make those opportunistic shifts for them.

Index Definitions

Barclays Capital Global Aggregate Ex-USD Index is a broad-based measure of global Investment Grade fixed-rate debt investments, excluding USD-denominated debt.

Barclays Capital Municipal Bond Index is an unmanaged index of municipal bonds traded in the U.S.

Barclays Capital U.S. Agency Index measures agency securities issued by U.S government agencies, quasi-federal corporations, and corporate or foreign debt guaranteed by the U.S. government.

Barclays Capital U.S. Aggregate Local Authorities Index measures the performance of U.S. investment-grade fixed-rate debt issued directly or indirectly by local government authorities.

Barclays Capital U.S. Asset Backed Securities (ABS) Index measures ABS with the following collateral type: credit and charge card, auto, and utility loans.

Barclays Capital U.S. CMBS Investment Grade Index measures the market of conduit and fusion CMBS deals with a minimum current deal size of $300 million.

Barclays Capital U.S. Corporate High Yield Index measures USD-denominated, noninvestment-grade corporate securities.

Barclays Capital U.S. Corporate Index is an unmanaged index that measures the performance of investment-grade corporate securities within the Barclays Capital U.S. Aggregate Index.

Barclays Capital U.S. Mortgage Backed Securities (MBS) Index measures agency mortgage-backed pass-through securities issued by GNMA, FNMA and FHLMC.

Barclays Capital U.S. Treasury Index measures public debt instruments issued by the U.S. Treasury.

BofA Merrill Lynch Fixed Rate Preferred Securities Index is an unmanaged index of fixed-rate, preferred securities issued in the U.S.

JPMorgan Emerging Markets Bond Index Plus(EMBI+) is a market-cap-weighted index that measures USD-denominated Brady Bonds, Eurobonds and traded loans issued by sovereign entities.

JPMorgan Government Bond Index-Emerging Markets (GBI-EM) Global Diversified is an unmanaged index of local currency bonds with maturities of more than one year issued by emerging-market governments.

S&P/LSTA Leveraged Loan Index is an unmanaged index of the institutional leveraged loan market.

Unless otherwise stated, index returns do not reflect the effect of any applicable sales charges, commissions, expenses, taxes or leverage, as applicable. It is not possible to invest directly in an index.

About Asset Class Comparisons

Elements of this report include comparisons of different asset classes, each of which has distinct risk and return characteristics. Every investment carries risk, and principal values and performance will fluctuate with all asset classes shown, sometimes substantially. Asset classes shown are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. All asset classes shown are subject to risks, including possible loss of principal invested. The principal risks involved with investing in the asset classes shown are interest-rate risk, credit risk and liquidity risk, with each asset class shown offering a distinct combination of these risks. Generally, considered along a spectrum of risks and return potential, U.S. Treasury securities (which are guaranteed as to the payment of principal and interest by the U.S. government) offer lower credit risk, higher levels of liquidity, higher interest-rate risk and lower return potential, whereas asset classes such as high-yield corporate bonds and emerging-market bonds offer higher credit risk, lower levels of liquidity, lower interest-rate risk and higher return potential. Other asset classes shown carry different levels of each of these risk and return characteristics, and as a result generally fall varying degrees along the risk/return spectrum. Costs and expenses associated with investing in asset classes shown will vary, sometimes substantially, depending upon specific investment vehicles chosen. No investment in the asset classes shown is insured or guaranteed, unless explicitly stated for a specific investment vehicle. Interest income earned on asset classes shown is subject to ordinary federal, state and local income taxes, except

U.S. Treasury securities (exempt from state and local income taxes) and municipal securities (exempt from federal income taxes, with certain securities exempt from federal, state and local income taxes). In addition, federal and/or state capital gains taxes may apply to investments that are sold at a profit. Eaton Vance does not provide tax or legal advice. Prospective investors should consult with a tax or legal advisor before making any investment decision.

The views expressed in this Insight are those of Kathleen Gaffney and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Eaton Vance disclaims any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Eaton Vance are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund.

This Insight may contain statements that are not historical facts, referred to as forward-looking statements. Future results may differ significantly from those stated in forward-looking statements, depending on factors such as changes in securities or financial markets or general economic conditions.

About Eaton Vance

Eaton Vance Corp. (NYSE: EV) is one of the oldest investment management firms in the United States, with a history dating to 1924. Eaton Vance and its affiliates offer individuals and institutions a broad array of investment strategies and wealth management solutions. The Company’s long record of exemplary service, timely innovation and attractive returns through a variety of market conditions has made Eaton Vance the investment manager of choice for many of today’s most discerning investors. For more information, visit eatonvance.com.

About Risk

An imbalance in supply and demand in the income market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. Investments rated below investment grade (typically referred to as “junk”) are generally subject to greater price volatility and illiquidity than higher-rated investments. Investments in foreign instruments or currencies can involve greater risk and volatility than U.S. investments because of adverse market, economic, political, regulatory, geopolitical or other conditions. In emerging countries, these risks may be more significant. As interest rates rise, the value of certain income investments is likely to decline. Commercial mortgage-backed securities (CMBS) are subject to credit, interest-rate, prepayment and extension risks. Investments in income securities may be affected by changes in the creditworthiness of the issuer and are subject to the risk of nonpayment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. Derivative instruments can be used to take both long and short positions, be highly volatile, result in economic leverage (which can magnify losses), and involve risks in addition to the risks of the underlying instrument on which the derivative is based, such as counterparty, correlation and liquidity risk. If a counterparty is unable to honor its commitments, the value of Fund shares may decline and/or the Fund could experience delays in the return of collateral or other assets held by the counterparty. There can be no assurance that the liquidation of collateral securing an investment will satisfy the issuer’s obligation in the event of nonpayment or that collateral can be readily liquidated. The ability to realize the benefits of any collateral may be delayed or limited. Fund share values are sensitive to stock market volatility. While certain U.S. government-sponsored agencies may be chartered or sponsored by acts of Congress, their securities are neither issued nor guaranteed by the U.S. Treasury. A nondiversified fund may be subject to greater risk by investing in a smaller number of investments than a diversified fund. No Fund is a complete investment program and you may lose money investing in a Fund. The Fund may engage in other investment practices that may involve additional risks and you should review the Fund prospectus for a complete description.

Bank loans are subject to prepayment risk. When interest rates rise, the value of preferred stocks will generally decline. Investments in equity securities are sensitive to stock market volatility. Equity investing involves risk, including possible loss of principal.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of a mutual fund. This and other important information is contained in the prospectus and summary prospectus, which can be obtained from a financial advisor. Prospective investors should read the prospectus carefully before investing.

Not FDIC Insured • Not Bank Guaranteed • May Lose Value

©2014 Eaton Vance Distributors, Inc.

Member FINRA/SIPC

Two International Place, Boston, MA 02110 800.836.2414 eatonvance.com