Non-Traded REITs

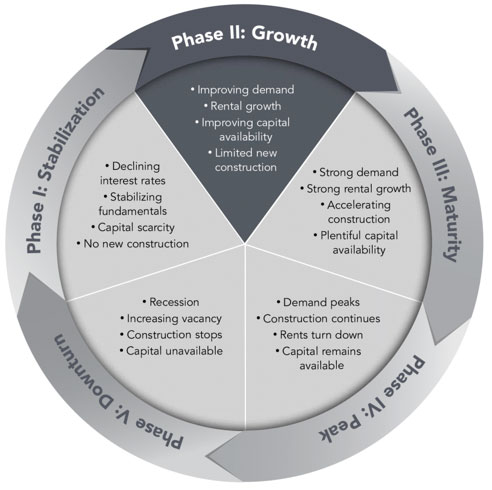

Enter Phase II of the real estate cycle

It has been a good year for real estate investing, and we believe the outlook for 2014 is favorable as well. The global economic recovery appears, at last, to have legs; interest rates remain low, consumer and business confidence is on the rise, demand for commercial space is improving, and there has been a years-long dearth of new construction. Perched on the sweet spot of the cycle, investors have been able to access real estate at attractive valuations.

Now that the sector has stabilized, we are moving into the growth phase, and it warrants a review of how we believe investors should position their portfolios.

Real estate cycles fall into five phases, as the chart above shows, with each lasting between three and five years. We entered 2013 at the end of Phase I — a period of stabilization following the sharp downturn precipitated by the subprime mortgage crisis and the Great Recession. Liquidity events over the past two years were unprecedented at more than $15 billion, greatly assisted by buying at the right time of the cycle.

Wrong type of real estate for the right type of cycle

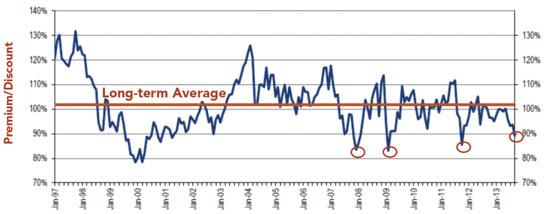

Amid the good news, investors began to worry about the end, or at least the tapering, of quantitative easing, and what it would mean for interest rates. In response, the 10-year Treasury yields briefly touched 3% in September.

The expectation of higher interest rates should create an adjustment phase in the real estate cycle. We have already seen this in listed REITs which, because of their greater liquidity, respond more quickly to events and are now trading at a 15% discount to NAV. We believe this is an attractive entry point for total return investors, but may have some predictive power for the short term outlook for real estate price appreciation in certain non-traded REIT property types.

Source: BoA Merrill Lynch; September 2013

One particular aspect of the non-traded REIT market is that in contrast to listed REITs, which have exposure to multiple real estate types, about 77% of non-traded REITs are net lease. Typically the underlying lease profile of such property is a ten-year, single-tenant lease with no rent adjustments. These bond-like characteristics make them vulnerable to rising interest rates. Short-duration real estate, such as apartments and hotels, along with economically sensitive property like industrial, tend to do much better in an improving economy.

In addition, the success we saw with liquidity events for non-traded REITs with assets bought at the bottom of the real estate cycle is unlikely to be repeated, particularly as the premium to NAV in the publicly traded market has diminished.

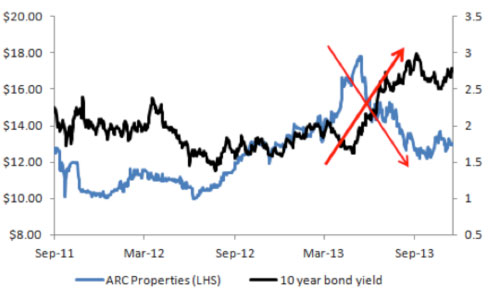

American Realty Capital Properties (ARCP): A case study

The trajectory of yields in the chart below illustrates the conundrum. The negative correlation between ARCP and 10-year Treasury yields is evident. The new lower NAV premium has significantly reduced the profitability of ARCP’s most recent acquisition offer for Cole Credit Property Trust III compared with its unsolicited offer to buy Cole in the spring.

A part of the reason for the negative reaction to higher interest rates is the level of debt that was incurred to finance an aggressive acquisition strategy; ARCP grew its enterprise value from only $300 million at the beginning of the year to $21.5 billion. The intersection of a highly leveraged balance sheet and the specter of higher rates has had a dampening effect on ARCP’s share price.

The company’s biggest acquisition was Cole, finally executed in October for $11.2 billion, including debt. The markets questioned why ARCP, a company trading at 11.6X 2014 FFO, paid a dilutive 14.1X FFO for Cole. The probable reasons include:

- ARCP became the biggest REIT in the net-lease sector, with 3,732 properties and an enterprise value of $21.5 billion.

- Cole has some key capital raising relationships which are valuable to ARCP.

- Cole is underleveraged, so the acquisition helps ARCP deleverage.

Follow the fees: ARCP and Apple

Liquidation events that carry a premium will be hard to find and impossible to count on given non-traded REITs are no longer buying at the bottom of the cycle, and publicly traded NAV premiums are diminished, indicating that investors need to look carefully at a REITs’ fundamentals. This includes fees and related-party transactions.

While the market has become more focused on internalization fees, non-traded REIT’s fees also exist in other forms. For instance, Cole’s internalization fee of up to $500 million, or 10% of enterprise value, garnered a great deal of negative attention.

However, it may not be widely understood that ARCP, while not charging internalization fees, is able to charge investment banking fees for related party transactions, including its recent merger with Cole, through Realty Capital Securities.

Further, an even more creative example of fee obfuscation can be seen with the Apple REIT merger. In August we learned that Apple REIT Seven, Apple REIT Eight and Apple REIT Nine — all hospitality REITs that made some good acquisitions in the downturn — entered into a merger agreement. Seven and Eight will roll up into Nine and terminate their management advisors. Nine will become self-advised and list as a publicly traded REIT in 2014.

There are no internalization fees involved in this merger. On further investigation, however, we found that when each Apple REIT was created, management granted themselves the right to buy Series B preferred shares at $0.10 per share. Upon merger or takeover, the preferred shares convert to common shares at a ratio of 24 common shares for each preferred. Thus, we estimate that with an initial investment of $850,000, management will pay themselves about $200 million when this deal is completed. That equates to 5.8% of equity value.

Related-party payments often obscure the dilutive impact hidden fees have on shareholders, and we would like to see better disclosure and an industry standard emerge.

The case for REIT preferred equity: Starwood snaps up Griffin preferreds

REIT perferreds are an often-overlooked way to invest in the real estate sector. They have the potential to provide income with less equity risk, a historically attractive yield premium to bonds and seniority over common equity holders.

Starwood Property Trust, a listed REIT, is a case in point. The company paid $250 million for 24.3 million preferred shares of non-listed Griffin Capital Essential Asset REIT. Griffin will use the funds to finance part of the acquisition of 18 office properties.

Starwood’s incentive is clear: The preferred shares will pay LIBOR plus 7.25% of the redemption price ($10.28), and that rate will increase 100 basis points per year. Starting in 2017, the rate will increase by 500 basis points per year.

The deal is a sweet one for Starwood. More than 80% of the Griffin portfolio’s operating income is generated by investment-grade tenants, or tenants with investment-grade parents. On the other hand, we think this is expensive capital for Griffin. The transaction does represent a tacit endorsement for the non-traded REIT industry however, with the involvement of a high quality institution such as Starwood in the space.

To sum up . . . .

The real estate cycle is evolving. We believe the sector’s outlook is positive, but the gains will be harder fought. With higher interest rates in the near future and discounts to NAV very much in the present, investors must position their portfolios with care. Rewards from non-traded REITs will come from good investments rather than quick money on the exit. Discounted listed REITs offer a good entry point, and REIT preferreds are another means of diversifying and rounding out a real estate allocation. An experienced portfolio management team can be crucial in navigating this changing environment.

Scott Crowe is the Global Portfolio Manager at Resource Real Estate. Previously,

he was the lead Global Portfolio Manager for Cohen & Steers, where he led the investment and research team of over 20 portfolio managers and analysts.

Mr. Crowe was accountable for over $10B in FuM across the global, international

and emerging market portfolios. Prior to this, Mr. Crowe held the position of Head

of Global Real Estate for UBS Equities Research where he built and managed the US REIT division while leading a global team of more than 40 analysts.