Eugene Fama and Lars Peter Hansen of the University of Chicago and Robert Shiller of Yale were the winners of the Nobel prize in economics. At first glance, one might wonder how the Nobel prize could be awarded to research work done in the same field on essentially the same topic that arrived at 180 degree opposite conclusions. Fama is famous for arguing that future stock prices cannot be predicted as the market is nearly perfectly efficient and stock prices are random. Shiller and Hansen conclude that future stock prices are somewhat predictable based on valuation, risk attitudes, behavioral biases and market frictions.

Understanding this dichotomy can make a tremendous difference in how you manage your personal investment portfolio. It is really important to try to synthesize what is underlying these opposite conclusions about future stock prices because it has fundamental implications what you should be doing with your stock investments today.

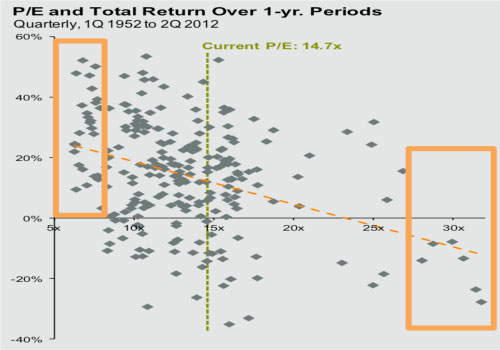

Let’s take a look at some fundamental evidence that supports the idea that stock prices are somewhat predictable over time using a chart of price/earnings ratios and market returns over a 1-yr period.

Source: JP Morgan Asset Management

You don’t need a PhD in economics to see that when the market P/E is roughly greater than 28, 100% of the time the stock market had a negative return over the next 12 months and when the market P/E is below 8, 100% of the returns were positive over the next twelve months. The problem is that the vast majority of time, the market P/E is between 8 and 28 and stock returns can be either positive or negative. During a one year time frame, the average P/E does not predict much. For example, the forward P/E of the S&P 500 was 15.2x at the market peak on October 9, 2007, just in front of the worst bear market since the Great Depression. On October 9, 2002, the forward P/E of the S&P 500 was not significantly different at 14.1x just before a five year, 100% bull market run.

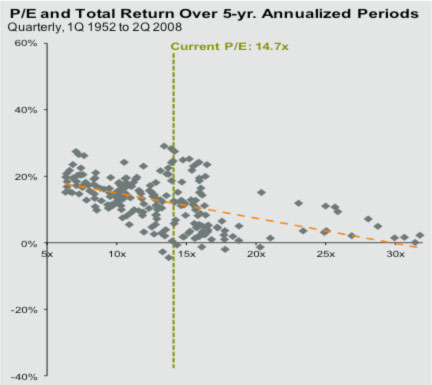

The next chart shows the relationship between P/E and five year returns. What happens by extending the investment time horizon is the data points consolidate around a trend line. Lower P/Es are generally associated with higher returns and high P/Es are generally associated with lower returns.

Source: JP Morgan Asset Management

Essentially, what the academic world is concluding is the dichotomy between random and predictable boils down to what time frame you use. In the short-term, stock prices seem to be random. In the longer term, prices seem to have an element of predictability.

Why does any of this matter? The reason why it matters is that if you believe future stock prices are completely random, you should be indifferent about buying when stock prices are low or high. High and low prices provide no information about future prices.

The implication of the Nobel awards and the charts above is future stock prices are somewhat predictable. After decades of buy-and-hold doctrine, the Nobel awards mark a significant paradigm shift in the world of personal investing. Market timing can work. Buy-and-hold is not the only solution. If you come to this conclusion and were not satisfied with having sustained two major hits to your stock portfolio over the past 13 years, you should start to explore the idea of market timing.

Historically, the problem with trying to time the market for a great number of individual investors is their emotions. Human beings are driven in large part by fear and greed. We often are our own worst enemy.

In the year 2000 near the end of the strongest bull-run in over a century of market history, many people vigorously increased their stock investment activity in the belief that earnings growth was robust and risk was low. Over the next decade, we experienced 9/11, extended wars in the Middle East, a housing market collapse, a credit crisis, a European sovereign debt crisis and a number of miscellaneous other confidence draining events including three debt ceiling negotiations. In the year 2008 and up through 2012, many investors sold stocks as they perceived risk to be elevated and growth prospects diminished.

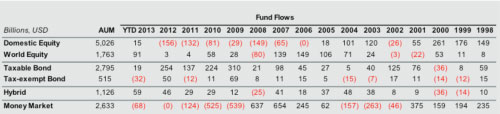

Shown below is a chart of fund flows in to stocks and bonds from 1998 through August, 2013.

Source: J.P. Morgan Asset Management

Note that the largest inflow into stocks occurred in 2000, in advance of a 12 year, highly volatile time with the S&P 500 through the end of 2012 showing essentially no appreciation. Shortly after the end of 2000, the NASDAQ depreciated by over 80%. The largest outflows from U.S. equities have occurred in 2008, 2011 and 2012 while the S&P 500 advanced roughly 160% from the March 2009 low. Year-to-date, the S&P 500 is up over 20%.

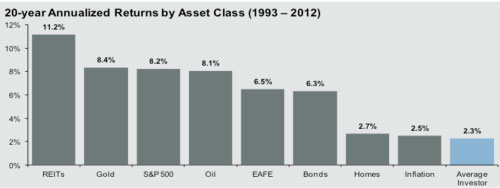

Because so many of us tend to buy at market highs and sell at market lows, the average investor has far under-performed a buy-and-hold approach. The chart below shows the 20-year annualized returns by the average investor is 2.3% which is worse than a buy-and-hold approach using almost every other major asset class. Clearly, the average investor is not adding value to the investment process.

Source: J.P. Morgan Asset Management

To take advantage of the Nobel prize winning economics research, you need to stop being human. You need to take a disciplined, non-emotional approach to investing. You need to stop letting fear and greed be your guide and start using some simple tools like moving average crossover models and other time-tested systems that allow you to avoid major market down moves and participate in major market up-moves.

There is a lot to the academic research that we do not touch upon in this discussion including the role of changing risk attitudes on expected future stock prices. The present value formula is being re-examined from the perspective of the importance of the discount rate (denominator) rather than the summation of expected future earnings (numerator). The really important takeaway is the average investor can significantly improve investment performance by engaging in some amount of market timing based on a systematic approach that overrides the normal human reactive emotions.

You should be asking your financial advisor if they are aware of the latest tactical trading methodologies and if they have examined the historical track records. You should wonder why your portfolio is not being dynamically and actively rebalanced as investor risk perceptions change. You should not be willing to accept a -55% drawdown in your stock holdings because buy-and-hold is the only way. You should recognize that your investment horizon may only be 20 to 40 years and you cannot tolerate a lost decade.

Where the world of real-world financial management appears to be ahead of the academic curve is in its understanding of the timeframe by when future stock prices transition from random to predictable. The world of actual money management, where attention is highly focused by having real-money on the line, is currently demonstrating that stock prices have a high degree of predictability in time segments of less than a year.

Stay tuned. Money management is evolving. Do not be late to the party. Get active.

Nick Atkeson, Author of Win by Not Losing and founding partner of Delta Investment Management.