Our “Approaching Retirement” blog will focus on the ways that financial advisors address the opportunities and challenges associated with delivering support for their clients nearing and living in retirement. We will also provide perspective and insights for broker-dealers, asset managers, insurance companies, wholesalers and other financial services providers in the retirement income marketplace.

A good place to start the discussion is by defining retirement income. As an industry, we tend to look at retirement income as a new trend. In reality, providing retirement income is not new. Most advisors serve retirement income clients and have done so for most of their career. While retirement income is a familiar activity to advisors, it is drastically changing driven by the first wave of retiring boomers, increasing investor longevity, and growing market complexity.

The term retirement income is used liberally in our industry. In a web search you’ll find related definitions on retirement planning or saving or retirement income solutions, but few definitions of retirement income. The website, businessdictionary.com, defines retirement income as “The amount of money an individual earns after retiring based on retirement savings assets, Social Security allowances, pensions, stocks, mutual funds, savings accounts, CDs, home equity funds, annuities, insurance, rental income, royalties, or inheritances.” But is this how key parties involved with retirement income see this activity?

We have observed that retirement income means different things depending on your point of view. These different viewpoints help contribute to the confusion surrounding retirement income and the lack of consensus on how it should be delivered.

![]()

· Product Providers

If you ask a product provider such as a fund company or annuity firm to define retirement income, you will likely get a more prescribed definition. They see retirement income primarily as an investment or insurance issue involving the creation of income for client needs and wants in retirement. This narrow product orientation makes sense given the value and core business of product providers. However, it may be too limiting given how others perceive retirement income.

· Broker-Dealers

Broker-dealers may define retirement income more expansively than do product providers. Many brokerage firms are taking a broader view as they grapple with supporting the needs of their advisors. But you're still likely to get a definition that focuses on retirement income relating ultimately to implementing an investment-related solution.

· Financial Advisors

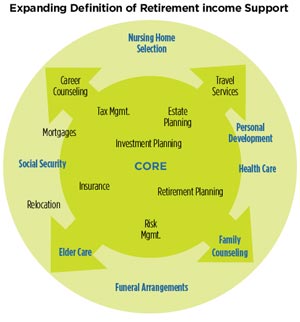

For financial advisors, creating income streams is a core component of the support they offer retirement income clients. Many advisors define retirement income more holistically, involving a range of comprehensive financial and personal issues that clients encounter as they shift to living in retirement. The range of services expands beyond investment management, risk protection, and income creation. It incorporates wealth transfer, health care, elder care, career development, and family issues. Advisors initially offered this broader definition of retirement support as an accommodation for clients. However, as the number of retirement income clients rise within their practice advisors are proactive and deliberate in offering broader services and support.

Few advisors offer all of the expanded services highlighted in the exhibit above. Nonetheless, advisors need to address the breath of capabilities they provide given the time and expertise required. They must also determine how best to provide these services, whether through themselves, their internal staff, or via a third party network

· Clients and Prospects

With regard to how clients define retirement income, they don’t. Retirement income is an industry term, not something in the client’s vernacular. Most clients are not able to articulate their needs in retirement beyond wanting to know if have enough savings to retire and maintain their lifestyle. Retirement income is at best a hazy term that defines living off their savings, Social Security and other available sources. Many clients don’t have a thorough or deep understanding of retirement income. As a result, the concept is often associated with misunderstanding or confusion and brings to the surface underlying anxieties and fears.

In the end, none of these definitions truly matter. The bigger challenge is not defining retirement income but instead putting in place the processes and capabilities to help clients make sound decisions. Product providers, broker-dealers and advisors must all align their support to serve the needs of a new generation of retirees.

We welcome your thoughts and comments about how you support retirement income clients and how you effectively engage with them on related subjects.