Solo advisors face many unique challenges, but perhaps the biggest is that they are, in bad times as well as good, solo. According to a REP. magazine survey, a significant portion of these advisors have no contingency plan in place should they unexpectedly not be able to continue working.

Medical emergencies, accidents, family problems, military deployment and maternity leave are just a few of the circumstances that can sneak up on advisors and keep them out of the office for prolonged periods, or perhaps permanently. At best, an unplanned change could simply mean confusion for clients and delayed access to accounts. At worst, advisors are failing in their fiduciary duty by exposing clients to real risks and potential litigation should their portfolios be negatively affected.

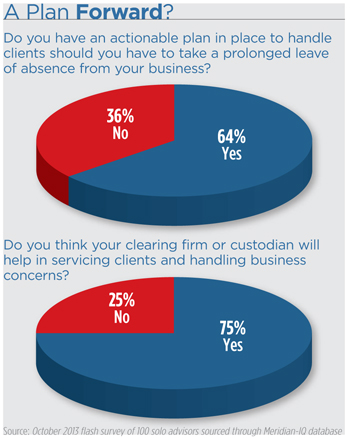

It’s human nature not to think about unplanned interruptions—think of the number of advisors who have no succession plan even though retirement is a foreseen event. And indeed, a significant portion of the population is vulnerable. An estimated 36 percent of the roughly 50,000 solo practitioners in the industry admit they do not have any actionable, documented business continuity strategy in case of unplanned events, according to an October survey of single-advisor practices conducted by REP. magazine. They have, on average, an estimated $10 to $30 million in AUM each, according to Sophie Schmitt, a senior analyst with Aite group.

“Anybody acting as a solo practitioner has to start by saying, ‘what happens if the unthinkable happens?’” says Knut Rostad, founder of the Institute for the Fiduciary Standard. “As a matter of course, sole practitioners should look at the types of ways they can prevent interruption. Unplanned events have real world business ramifications.”

Whether they know it or not, most solo advisors, of course, will rely on processes in place through their firms or custodians to step in in case of an emergency. That generally happens—to a point. If the advisor has any affiliation at all, the clients will likely be picked up—eventually. “Vultures have a great sense of smell,” says Brandon Odell, director of The Ensemble Practice. For advisors with a broker-dealer, the firm usually will parse those clients out to other advisors within the same geographical area. For RIAs, usually custodians will step in. Schwab, for instance, will roll over an advisors’ assets to nearby retail locations. “If it matters to them, they will figure it out,” Odell says.

But for clients who are generally clueless about their advisors contingency plans, or lack thereof, the notion that they will “be picked up” by the institutions running in the background or handed off to other advisors will bring scant comfort. Not to mention the smaller clients that won’t be able to find a home with another advisor.

Failing to prepare not only can weaken client relationships, it also opens advisors up to legal and ![]() regulatory scrutiny, especially those acting as fiduciaries. “From a fiduciary perspective, there cannot be any material lapse of service,” Rostad says. And that can mean as little as a day without crucial communication to clients.

regulatory scrutiny, especially those acting as fiduciaries. “From a fiduciary perspective, there cannot be any material lapse of service,” Rostad says. And that can mean as little as a day without crucial communication to clients.

Many of these solo practitioners fall under state regulators, where the quality of oversight varies state to state.

“We do consider (business continuity plans) to be part of the standard fiduciary obligation,” says Mark Leyes, spokesman for the California Department of Business Oversight, the division overseeing state securities enforcement. “We do examinations of investment advisors and that’s something examiners are mindful of.”

While the state doesn’t have specific regulations requiring advisors to have a business continuity plan,  examiners would recommend advisors develop these business provisions during an audit. “It has happened in the past that [clients] were left without certainty of what to do next,” Leyes says. It’s most common with clients of single advisors, he added.

examiners would recommend advisors develop these business provisions during an audit. “It has happened in the past that [clients] were left without certainty of what to do next,” Leyes says. It’s most common with clients of single advisors, he added.

On a larger scale, the SEC recently weighed in on the importance of continuity plans—especially in the wake of natural disasters and other events—issuing a risk alert in August. The regulator recommended advisors should not only have business continuity plans in place, they should enhance them to anticipate widespread events, “including possible interruptions in key business operations and loss of key personnel for extended periods.”

There could also be legal ramifications, especially if clients lose money during a transition.

“One of the biggest risks (if not the biggest risk) for a solo’s clients is the potential that something catastrophic could happen such that the solo could no longer work/manage their clients assets,” says California securities attorney Patrick Mahoney says. Not having a plan opens up advisors to liability. And while the advisor may not be around to face the consequences of angry client, an advisor’s surviving family may have to resolve any lingering business issues in court.

An astute lawyer seeking damages could argue that an adviser should have foreseen that a catastrophic event was not out the realm of possibility. “Failure to have a contingency plan in place, as a fiduciary, is certainly not in the best interests of their clients,” Mahoney says.

Preparation is Key

A little over three years ago, Columbus, Ohio-based Lori Embrey had to develop a unique continuity strategy after founding her solo practice, Fairfield Investments and Wealth Management—she was pregnant. And while she had a plan in place for emergencies, she needed to create a specific plan of attack for this particular situation, which would keep her away from daily client work, but not entirely absent.

“It was about preparation,” Embrey says. Several months before her due date, she went through all of client accounts, meeting with every single client and going over their financial goals, account statements and who to contact in case she could not be reached.

Within Embrey’s overall business continuity plan, she created binders on each client. For high net worth clients, she directed them to a specific firm that could meet their needs. She also had another, separate advisor assigned to take over for middle-income clients and clients with one-time financial plans. “It’s a best practice for doing business, especially if you are doing things on your own,” she says.

But for her maternity leave, Embrey relied on a long-term intern majoring in financial planning at The Ohio State University, as well as technology, to keep things running smoothly. “I didn’t work full time, but I always had my phone attached to my side,” Embrey says, calling the months after the birth of her fourth child “time unpredictable” because she didn’t know what she’d be doing from day to day.