Before beginning any discussion on the tax benefits of charitable giving with your clients, it’s always good to stop and remember that the tax tail should never wag the charitable dog. Although gift planners, attorneys, accountants and financial advisors can have a measurable impact on the effectiveness of charitable giving by providing proper advice and structuring, ultimately, the gift is about the good it can do and not the tax benefit it accumulates on the way.

Although there have been several legislative and other proposals that may affect the tax benefits of charitable giving in the future, as of the date of this writing, the benefits of charitable giving for 2012 remain much as they have been in previous years. However, as we move into 2013, the effect of the 3.8 percent net investment income tax and the return of various phase-outs and reductions of the benefits of itemized deductions, will start to erode the benefit of the charitable itemized deduction. Of course, legislation may defer or cancel those provisions. Once effective, those changes put more of a premium on excluding income from adjusted gross income (AGI), than on generating a tax deduction. The following examples are simplified to focus on those differences.1

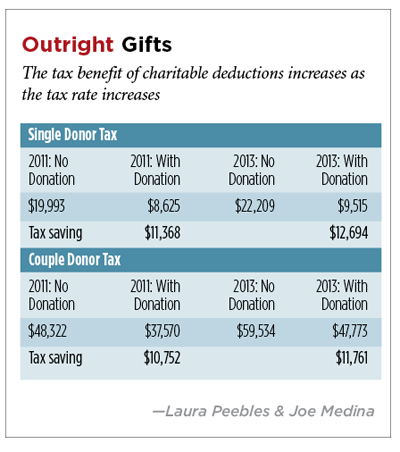

Outright Gifts of Cash

The tax benefit of cash gifts is a function of the effective tax rate of the donor. In 2012, the top effective individual federal rate is 35 percent. Many donors will find themselves with a different top effective tax rate: they may be paying alternative minimum tax (AMT) at 28 percent or the 15 percent tax rate on qualified dividends and capital gains.

For 2013, barring legislative action to the contrary, the top rate will return to 39.6 percent, the capital gains rate will rise to 20 percent, qualified dividends will be taxed as ordinary income and a number of indirect factors will affect the true effective rate for donors. Although the 28 percent AMT rate is expected to remain, the AMT “patch” hasn’t yet been extended for tax years 2012 or beyond.2 State rates vary from zero to approximately 12 percent, although state effective rates also vary based on the deductions and exemptions allowed at both the federal and state levels.

For most of our examples, we’ll use two donors:

1. A single individual with an AGI of $100,000 composed solely of wages or pension income, and

2. A couple with an AGI of $250,000, $30,000 of which is long-term capital gain and $20,000 of which is qualified dividend income.

What happens if each donor gives $50,000 cash to a public charity? (Assume they live in a state with either no state income tax or no state benefit for charitable donations.)

Today, the tax benefit of charitable deductions increases as the tax rate increases in 2013, even with the return of the phase-out of the benefit of itemized deductions (see “Outright Gifts, p. CGS 7).

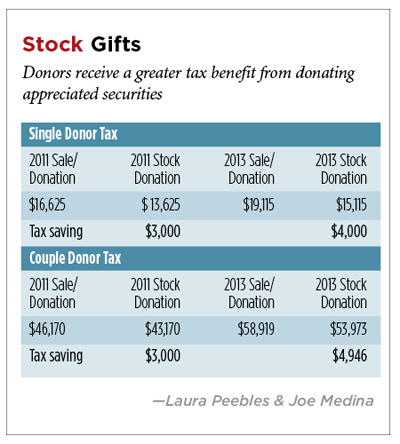

Appreciated Securities

One of the benefits of the U.S. tax system is the ability to deduct the value of long-term capital gain assets given to charity without being taxed on the appreciation inherent in the asset. For example, if a donor contributes an appreciated security that has a basis of $20,000 and a fair market value (FMV) of $100,000, he may take a deduction equal to $100,000 (subject to certain limitations), and the charity receives a gift worth $100,000. If the donor was to sell the securities and donate the after-tax proceeds, the charity may receive only $88,000.3 In addition, the donor would receive a smaller income tax charitable deduction. However, like many tax benefits, this one isn’t unlimited. Unlike cash donations that can be deducted up to 50 percent of a donor’s AGI, contributions of long-term capital gain property can only be deducted up to 30 percent of a donor’s AGI. Like cash donations, there’s a 5-year carryover for any donations in excess of that annual limit.4

To keep the comparison simple and to avoid carryover calculations, let’s say that our donors contribute $30,000 of stock with a basis of $10,000 or, instead, that they sell the stock and donate the cash. Again, this comparison is for federal rates only. (See “Stock Gifts,” this page.)

In addition to receiving a greater tax benefit from donating appreciated securities (rather than cash) to charity, the donor can use the cash that would have been donated to charity to purchase new investments with a refreshed basis. For example, assume a donor would like to provide a public charity with a $30,000 benefit, and he’s indifferent as to whether the donation is made in cash or other assets. The donor has XYZ stock in his portfolio, with a cost basis of $10,000 and an FMV of $30,000. If he donates the stock to the charity, he’ll have a charitable deduction of $30,000, subject to certain limitations. He can then use the $30,000 that he otherwise would have donated to charity to repurchase the XYZ stock. The basis of the new XYZ stock is $30,000. In effect, the donor received a step-up in basis of the XYZ stock from $10,000 to $30,000, in addition to meeting his charitable goals. The wash sale rules apply only to losses upon sale, not gains or donations; therefore, the wash sale rules don’t apply to this situation.5

The benefit of such a non-cash donation to a private foundation (PF) would be similar, although the tax benefit would be spread over two years. The limit for deductions of publicly traded stock to PFs is 20 percent of the donor’s AGI with the same 5-year carryforward for the excess.6 The deduction for donations of other appreciated property to non-operating PFs is limited to cost basis or FMV, whichever is less.7 Such a donation, followed by a sale of the property by the PF, may still make sense, since the gain is excluded from the donor’s income.

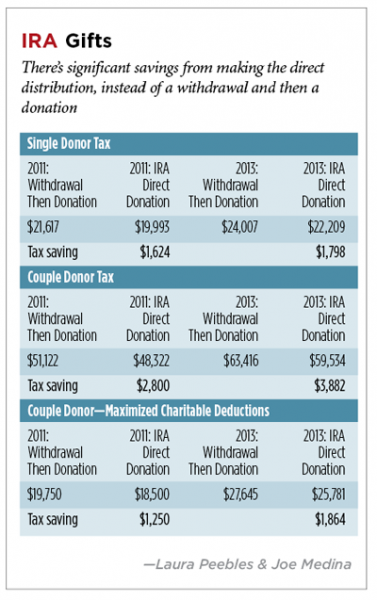

Gift of IRA

This tax provision receives a great deal of attention, perhaps more than it deserves in many cases. For those wealthy donors who are bumping up against AGI limitations for cash or property donations, it’s an effective tool to reduce their taxes, while increasing their philanthropy. Of course, it’s only available to those individuals 701/2 or older. For comparison purposes, we’ll add a third variation to our two donors: a couple who have already maximized their cash charitable deductions at 50 percent of AGI. As of this writing, this provision hasn’t been extended into 2012, but the comparison for 2011 is included, as the provision may be reinstated for 2012 or future years.

Assume that each donor either takes $10,000 from his individual retirement account and donates it to a qualifying public charity or, instead, makes a qualified charitable distribution from his IRA directly to the charity. (See “IRA Gifts,” this page.)

In every case shown in “IRA Gifts,” there’s significant savings from making the direct distribution, instead of using the “withdraw and contribute” method. There’s an exception to this rule: If a donor in 2011 already has itemized deductions in excess of his standard deduction, there will be no difference between the direct and indirect donation. But, donors would never be worse off for doing the direct distribution to the charity.

The exclusion from AGI becomes more valuable in 2013, as the effect of the 3.8 percent net investment income tax kicks in. The effect of the exclusion is especially valuable if the donors wouldn’t otherwise itemize, since all or a portion of the deduction is lost due to the large standard deduction allowed to individuals over age 65 ($14,200 in 2012). The latest Internal Revenue Service statistics show that non-itemizers are 64.4 percent of those filing individual returns. Obviously, many of those individuals can’t afford significant charitable deductions either, but some older donors have paid off their mortgages and/or live in lower tax states and, therefore, don’t have deductions otherwise in excess of the standard deduction. Notice this effect in the third example: their benefit from the direct IRA transfer is only $1,864, which is the benefit of not exceeding the 50 percent limit on charitable deductions. Our comparison couple, who will save $3,882 in 2013, are affected by the loss of the benefit of the deduction (their donation is lost in their standard deduction), the phase-out of itemized deductions and the 3.8 percent additional tax.

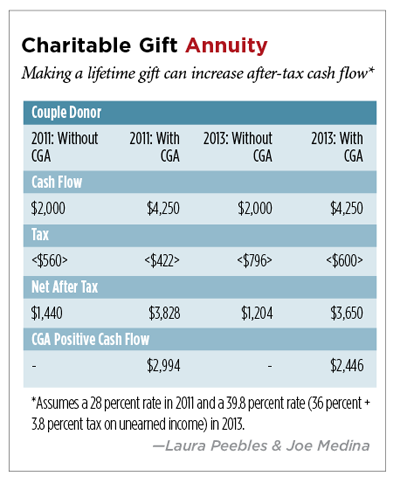

Gift Annuity

A gift annuity is the only way to accomplish the equivalent of an installment sale of publicly traded securities. It’s also a gift that keeps on giving back, through a lifetime of payments to the donor or the donor and one other person.

By creating a gift annuity with appreciated securities, donors can avoid pushing themselves into a higher tax bracket and, instead, spread the gain on a sale over their lifetime. Since the gain on a sale could push someone into the 3.8 percent net investment income tax bracket starting in 2013, spreading out the gain could produce a tax benefit. The gain will be taxed at the capital gains rate, whatever that happens to be for the year the payments are received (currently 15 percent for 2012, scheduled to return to 20 percent thereafter). However, the income components of the gift annuity income will be subject to the 3.8 percent tax on net investment income.8 That will be true for gift annuities already in process, not just ones starting after 2012.

Our single donor with only $100,000 of AGI will be unaffected by the 3.8 percent net investment income tax, since the threshold for single individuals is AGI of $200,000. Not so for our couple with the AGI of $250,000; every dollar of their portfolio income in excess of $250,000 will be subject to the 3.8 percent tax. (This tax is calculated on the lesser of the amount of income in excess of $250,000 or certain types of income: generally unearned income.9) The income tax deduction for charitable contributions, like most other itemized deductions, can’t reduce the amount of their income subject to the 3.8 percent net investment income tax.

Assume our $250,000 income couple has contributed $100,000 to a lifetime gift annuity. Assume ages 55 and 58 for the annuity calculation, using standard National Council on Gift Annuities rates, but reduced to 4.25 percent, from 4.6 percent, to meet the 10 percent remainder test at the January 2011 Internal Revenue Code Section 7520 rate of

2.4 percent. If they hadn’t set up a gift annuity, they would have left the $100,000 invested in a 2 percent yield fund and made a testamentary bequest of the $100,000.

By being willing to make a lifetime gift, they increase their gross cash flow, decrease the risk of outliving their income and increase their after-tax cash flow by substituting a return of capital for (taxable) investment income. They also benefit from the approximately $10,000 charitable deduction in the initial year of the annuity. Also, don’t forget the acknowledgement and satisfaction that goes with lifetime giving as well. (See “Charitable Gift Annuity,” this page.)

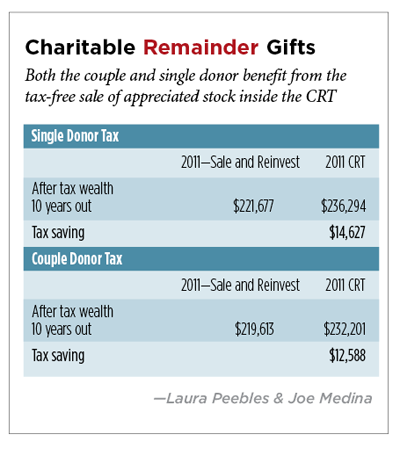

Charitable Remainder Trust

The true benefit of a charitable remainder trust (CRT) is not just the up-front deduction for the value of the remainder interest—it’s the deferral of the tax on the gain realized on the sale of appreciated assets. Assume for our examples that our two donors place an appreciated stock worth $200,000 into a 10-year charitable remainder unitrust, taking back the maximum amount, so that the deduction is $20,000. Using the January 2011 Section 7520 rate of 2.4 percent gives the donors a 21.061 percent payout. Assume the cost basis of the stock was only $40,000. At the end of 10 years, assuming that the 2013 rates continue throughout the term, “Charitable Remainder Gifts,” p. CGS 11 shows the numbers to compare with what the donors would have had if they had sold the stock and invested the proceeds. At the end of the 10-year term, the “sell and reinvest” donors then donate the same amount to charity as passes to the charity at the end of the CRT. With or without the charitable trust, the assumed return on investment is ordinary income of 5 percent.

Both the couple and the single donor benefit from the tax-free sale of the appreciated stock inside the CRT over the choice to sell the stock outside the trust and reinvest the proceeds in a taxable environment.

Charitable Lead Trusts

For the truly wealthy donor who wants to benefit charity and family, it’s worth looking at the charitable lead trust (CLT) as a planning tool. The recent changes to the tax laws aren’t likely to have a significant effect on the planning process, because most donors who are suitable for CLTs are wealthy enough that they’ll be affected by the 3.8 percent net investment income tax before and after any CLT.

What’s important when working with these donors is the need to consider the 3.8 percent net investment income tax as it applies to the trust in any economic model presented to the donor. Unfortunately, although trusts are allowed to reduce their taxable income by distributions to non-charitable beneficiaries before calculating the 3.8 percent tax,10 this reduction, apparently, doesn’t apply to payments made to charities by charitable lead or other trusts, since those payments aren’t considered “distributions” under the trust tax rules.11 As a consequence, it appears, subject to future guidance, that a CLT will have its net investment income subjected to the 3.8 percent tax unless its AGI (as defined in IRC Section 67(e)) isn’t in excess of the dollar amount at which the highest tax bracket in IRC Section 1(e) begins. Remember, for trusts and estates, the tax brackets are very narrow (for example, for 2012, the highest tax bracket for trusts and estates starts at $11,650). Future guidance, either from Congress or the IRS, may clarify the effect of Section 1411 on CRTs, but in the meantime, prudence dictates that the worst case be assumed.

The Moral

Everyone’s numbers are different, and there will be exceptions to almost every principle discussed above. The moral of our story is twofold: 1) the impact of the potential tax rate increase and the net investment income tax will differ depending on the type of charitable vehicle used; and 2) ALWAYS run the numbers!

—This article contains general information only and Deloitte is not, by means of this material, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect you or your organization. Before making any decision or taking any action that may affect your organization, you should consult a qualified professional advisor. Deloitte, its affiliates and related entities, shall not be responsible for any loss sustained by any person who relies on this article.

Endnotes

1. The examples use 2011 rates. Other than an inflation adjustment to the tax brackets, the 2011 and 2012 tax rules are similar and the observations made on the provided examples are the same.

2. The alternative minimum tax (AMT) “patch” is an adjustment to the exemption amount. Without that adjustment, usually enacted one year at a time, millions more taxpayers would pay AMT in addition to their regular tax.

3. [$100,000 - (($100,000 -$20,000) x 15 percent)].

4. Internal Revenue Code Sections 170(d) and 170(b)(1)(D)(ii).

5. IRC Section 1091.

6. IRC Section 170(b)(1)(D).

7. IRC Section 170(e)(1)(B)(ii).

8. IRC Section 1411(c)(1)(i).

9. IRC Section 1411(a)(1).

10. IRC Sections 1411(a)(2) and 1411(e)(2).

11. Treasury Regulations Section 1.663(a)-2.