Given the lofty federal estate and generation-skipping transfer tax exemptions, it’s quite possible that many individuals will never be subject to either tax. As estate planners seek to add value to clients’ estate plans, income tax planning (which affects the majority of individuals) is becoming more important to individual clients and, therefore, to estate planners. Traditional individual retirement accounts with balances that remain after an IRA owner’s death, often present a significant income tax planning opportunity. IRA balances, in addition to being candidates for lifetime stretch-out distributions to children and other beneficiaries, are a natural source of funding charitable bequests at death.

Estate planners, whether driven by probate avoidance or other desires to provide protection for beneficiaries, frequently use trusts to effect the distribution of their deceased clients’ estates. If a planner wishes to fund charitable bequests at death with taxable income, such as IRA benefits, he frequently must juggle at least three (sometimes more) legal balls: (1) the fiduciary income tax rules, (2) the law of trusts, and (3) the inherited IRA stretch-out rules. If just one ball drops, the planner may be met by an unhappy beneficiary, as well as a worried law firm loss prevention officer.

To clarify the issues for planners, let’s look at four aspects of funding charitable bequests with IRA assets: (1) the advantages of using such a strategy; (2) the trust technique most commonly used (up to this point) to fund charitable bequests; (3) why this technique is no longer effective due to a recent change in Treasury Regulations Section 1.642(c)-3(b)(2) (the Regulation); and (4) suggestions on how to satisfy the Regulation’s rules, including, when appropriate, the use of a charitable distribution trust (CDT).

Advantages of Using Taxable Income

It’s easy to explain the advantages of using taxable income to fund a client’s charitable bequests, and clients usually understand and appreciate the explanation. Specifically, if a client is charitably inclined, has two assets of equal value, such as a mutual fund (the basis of which has just increased to its fair market value as a result of the client’s death) and a traditional (non-Roth) IRA (consisting entirely of taxable income), and the client has the ability to choose which asset should pass to the charity, the answer is obvious. It’s better to fund the charitable bequest with the IRA benefits (which are fully taxable) and give the mutual fund (which has no negative income tax characteristics) to the family. This result is favorable, because the charity pays no taxes on such income, while the family would have paid income taxes if it had received such income.

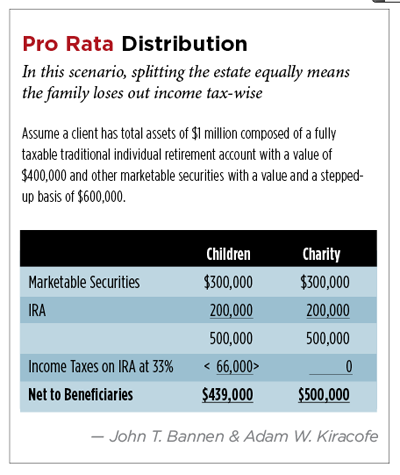

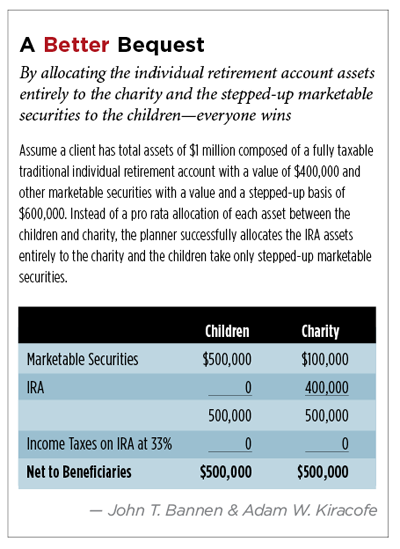

For example, “Pro Rata Distribution,” p. CGS 29, demonstrates that, if the IRA benefits are distributed to the family share, the family members’ share will ultimately be reduced by income taxes. Assuming an applicable income tax rate of 33 percent, the income taxes due would be approximately $66,000. Is there a better way than making a pro rata distribution of assets between the family and the charity? Definitely! Let’s look at “A Better Bequest,” p. CGS 29, in which the taxable IRA benefits are, instead, distributed to the charity, no income taxes are owed or paid and the family benefits from a tax savings of approximately $66,000. The charity receives the same amount in each scenario. The client’s charitable goals are satisfied, and his family ultimately receives a greater inheritance. Moreover, a $66,000 tax savings should make a modest bill for estate-planning services more palatable. This is a win-win for the client and the planner.

The Common Approach

The most common approach to funding charitable bequests in trusts (based solely on our anecdotal review of estate-planning documents that have passed our desks) is to simply provide in the document that any bequests to charity will first be funded with income in respect of a decedent (IRD).1 IRD is any item of taxable income that accrued to the decedent prior to his death, but was not yet properly reportable on the decedent’s final income tax return. This definition precisely describes an IRA balance remaining at a decedent’s death: Income has accrued, but isn’t reportable on the decedent’s final income tax return, because the IRA benefits haven’t yet been withdrawn. A direction to the trustee to fund charitable bequests first with IRA assets and then with other assets is a logical approach and clearly describes the desired result. Yet, the tax environment in which this direction operates is more complex than it appears.

The fiduciary income tax rules establish several different categories or “classes” of income (capital gain, tax-exempt interest, foreign income, ordinary interest, unrelated business taxable income (UBTI) and others) and provide special rules with respect to allocating these classes. These rules circumscribe the ability of a planner to reach into the bucket of income, pull out a specific class of income and allocate it to a particular beneficiary. This is precisely what the planner would like to do, namely, reach in, grab the IRA proceeds and place them on the charity’s doorstep. If there was ever a doubt whether this provision produced the desired result, it was resolved (unfavorably) effective April 16, 2012, when the Treasury issued T.D. 95822 (the Regulation), making final an earlier proposed regulation affecting Internal Revenue Code Section 642(c) and the fiduciary income tax charitable deduction.

The New Requirement

The Regulation requires that, before an allocation of a particular class of income to a particular beneficiary will be respected, the provision in the governing instrument (such as a will or trust) “must have economic effect independent of the income tax consequences.”3 Similar rules govern the allocation of items of partnership income among partners, that is, the allocation must have economic substance in addition to producing the desired tax consequences.4 While the penumbra of the economic substance doctrine has yet to be fully defined, the Regulation charts a sure course in at least one respect: A provision in a governing instrument that allocates a particular class of income (such as IRA proceeds) to a particular beneficiary (for example, a charity) must have independent economic effect to be respected. Such a provision will have independent economic effect if the amount the charity receives is determined by the amount of the class of income available. In other words, such a provision would require the distribution to the charity to be satisfied solely from and limited to a particular class of income. If the class of income—such as IRA proceeds—was insufficient to fulfill the bequest, then the bequest would go unsatisfied, at least as to the shortage. Such an allocation of income has economic substance.

On the other hand, if an allocation provision lacks economic substance, then it will be ignored and the income that the beneficiary (in this case, the charity) receives will consist of the same proportion of each class of the items of income as the total of each class bears to the total of all classes.5 Any other beneficiaries who receive a distribution in the same year (the children, for example) will receive the same pro rata share of income, including a share of the IRA assets. (This produces the same negative tax results shown in “Pro Rata Distribution.”)

Here’s another way of looking at it: If the allocation of income doesn’t affect the actual amount the charity receives, it won’t be respected. For example, if a trust provision directs that a charity receive $100,000, and the class of income specifically allocated to the charity is only $80,000, the fact that the fiduciary distributes other classes of income (or even principal) to complete the distribution to the charity will cause the allocation provision to lack economic substance. In that scenario, regardless of the allocation of a specific class of income, the charity received the full $100,000. The specific allocation of income ($80,000) neither controls nor affects the economic result. Thus, the provision lacks economic substance independent of the tax consequences and will be disregarded. In contrast, for the allocation of income provision to have economic substance (and, therefore, be respected), the charity must bear the risk of losing some part of its specified distribution if the class of income is insufficient.

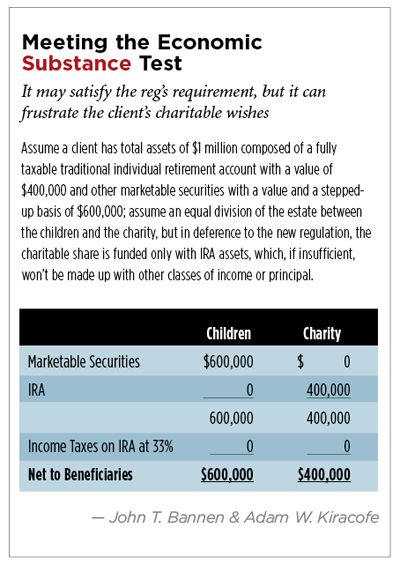

Accordingly, one way to satisfy the economic substance requirement and still effectively allocate the IRA proceeds to the charitable share would be to limit the charity’s share by the amount of income allocated. Thus, if there’s sufficient income in the allocated class, the charity is paid in full. If not, the charity loses. There’s economic reality independent of income taxes, because the charity has some skin in the game. The amount the charity ultimately receives can be affected by the amount of the class of income allocated to the charity under the governing instrument. Although such a provision would appease the gods of the fiduciary income tax regulations, it could very well frustrate the client’s charitable intentions. (For an example of this result, see “Meeting the Economic Substance Test,” this page.)

The problem with giving independent economic substance to an income allocation provision is that it actually has economic substance. So, what are the alternatives?

Alternatives

The villain in this tax drama is the fiduciary income tax system and the economic substance regulations dealing with the allocation of a specific class of income to a specific beneficiary. One possible solution involves beneficiary designations. With IRA benefits (less so with some other forms of IRD), distributions can be made in the beneficiary designation form provided by the IRA sponsor. In “A Better Bequest,” if the IRA owner simply made the IRA account payable directly to the charity, the IRA assets wouldn’t pass through the various hooks and snags of the fiduciary income tax system, because the assets wouldn’t pass through the trust. The trust would need no charitable deduction, because it wouldn’t have received any IRA benefits in the first place. The IRA distribution Form 1099 goes directly to the charity, which is exempt from income tax on IRA income (assuming no part of it is unrealized business taxable income). Moreover, the client’s revocable trust could include a provision requiring a distribution of principal to the charity to “top off” the distribution if the IRA benefits prove to be short of a desired amount. The result: income tax is avoided, the client’s desired charitable distribution has been achieved and the estate planner can pack up the tools of the trade and go home.

Unfortunately, this approach won’t work for every situation. If the IRA benefits represent a substantial portion of the decedent’s estate, making all of the IRA benefits payable directly to the charity could well overfund the charity’s bequest at the expense of the children’s share. Moreover, this approach involves a moving target (or perhaps a moving marksman), because the value of the IRA benefits is constantly in flux, affected not only by the slings and arrows of investment fortune, but also by required minimum distributions after age 701/2. Nor is addressing the matter in a formulaic IRA beneficiary designation (such as “I give to the charity one-half of my taxable estate as determined for federal estate tax purposes, etc.”) likely to be effective. Convincing an IRA administrator (other than a full service, full fee trust company) to respect, or even accept, such a beneficiary designation is, in our experience, nigh on impossible. Thus, if a formulaic allocation is required (such as an amount equal to one-half of the client’s federal taxable estate), the formula, as a practical matter, will be included in the client’s trust, and the planner must run the gauntlet of the economic substance regulations if more than a pro rata share of IRD is to be allocated to the charity.

Moreover, if a portion of the IRA is paid directly to charities by beneficiary designation and a portion to children or other natural beneficiaries, the charities must be paid out6 or a separate share must be created for them7 prior to Sept. 30 of the year following the year of death, if the lifetime stretch-out potential for the natural beneficiaries is to be preserved. If the charities are numerous, this can be both an arduous and risky endeavor. Depending on the date of death, the decedent’s personal representative or trustee may have as little as nine months and one day to accomplish this task (for example, if the decedent has the misfortune to die on Dec. 31). IRA administrators often require that an “inherited IRA” be created for each beneficiary (charitable or otherwise) listed on the designation form before making any distributions. This is understandable in view of the administrators’ desire to have a written contract with the beneficiaries confirming the IRA sponsors’ ability to take investment directions from each beneficiary and be protected from claims for unauthorized actions. Furthermore, if the charities are numerous, coordinating the signing of charitable inherited IRA agreements could be very time consuming. Even though each charity should be motivated to act promptly, the trustee or personal representative has no control over the situation and is at the whim of each charity. The charitable cats may resist herding. Is there a better alternative to resolve these issues?

We propose a solution: the CDT. But, to fully appreciate the advantages the CDT offers, it’s first necessary to briefly discuss the unique aspects of the charitable income tax deduction in the fiduciary income tax regime.

Fiduciary Tax Charitable Deduction

There’s much that’s kind and good about IRC Section 642(c), the provision that allows a charitable income tax deduction for certain income distributed to a charity from an estate or trust. For example, the exemption is unlimited; that is, unlike individuals, the charitable deduction for trusts isn’t limited to a percentage of the trust’s adjusted gross income. Nonetheless, there are a few stumbling blocks for the uninitiated.

For example, no charitable deduction is allowed to the extent a charitable distribution is made with federally tax-exempt income8 or certain UBTI.9 In addition, a trust or estate will qualify for a charitable deduction for distributions to charity only if the requirements of Section 642(c) are satisfied.

Under IRC Section 661, a Form K-1 is issued to each non-charitable trust beneficiary who received a distribution from the trust in that given taxable year. The income reported on a beneficiary’s Form K-1 is attributable to that beneficiary, and the beneficiary must report it on his personal income tax return. Many practitioners mistakenly assume that if income is actually distributed to a charity, the estate or trust will automatically qualify for a charitable income tax deduction for the amount of the gifted income and that the taxable income flows out to the charity under Section 661 on a Form K-1. This, however, isn’t the case. A Section 661 distribution deduction is expressly denied for distributions of income to charity.10

Thus, a trust is protected from income tax with respect to income it receives and subsequently distributes to charity, not by a distribution deduction under Section 661, but rather by a Section 642(c) charitable income tax deduction taken on the fiduciary income tax return, which is equal to the income distributed to the charity. Hence, there’s no K-1 involvement for income distributed to a charity.

The qualification requirements for a Section 642(c) charitable income tax deduction are very unforgiving and are literally interpreted by the IRS and, frequently, by the courts as well. There are three general requirements:

• The payment of income must be made pursuant to the governing instrument.11 Thus, the document must direct or authorize the trustee to make the charitable distribution from trust income.

• The payment must be made out of a trust’s gross income.12 This requires tracking the origin of the item that was distributed to the charity.

• The income may not be tax-exempt income or UBTI.13

Note that IRD is specifically included in the trust’s gross income for purposes of the charitable deduction.14 IRA benefits are a ubiquitous source of IRD. With this background, let’s turn to the advantages offered by a CDT.

Advantages of a CDT

A CDT addresses all of the shortfalls discussed above: the risk that a client’s desired charitable distribution may be frustrated if the amount of IRA assets directed to fund the bequest falls short of the desired level; the result that the allocation will lack economic substance and, thus, be ignored; the likelihood that IRA sponsors will refuse to interpret a beneficiary form containing a formula; the fact that the trustee will have no control over the timing of critical distributions; and the freezing of the IRA and its investment activity until all the beneficiaries can be rustled up to sign their inherited IRA agreements.

Enter the CDT. It’s a separate, independent trust to which part or all of a decedent’s IRA assets are payable. It could be a separate freestanding trust or a separate trust created within the decedent’s revocable trust agreement, much like a credit shelter trust or marital trust. The CDT’s sole function is to collect and distribute IRA assets made payable to it. It incorporates all of the requirements necessary to qualify for a charitable deduction for a distribution of income to a charity. Thus, the governing document specifically states the requirement to satisfy charitable bequests from income. It also provides that payments must be made out of the gross income of the trust including any IRA assets paid to the trust. The CDT satisfies the economic substance requirement, because the trust has only one class of income (IRA assets) and that class of income is the sole source for the payment of charitable bequests. If the IRA assets payable to the trust are insufficient, then as to the CDT, the bequest goes unpaid. If the client has a specific charitable distribution goal (an amount certain), query whether the revocable trust itself (as opposed to the CDT) could make a distribution of its principal to top off an underfunded charitable bequest in the CDT.

Those in favor of this technique would cite the fact that the revocable trust is a legal entity separate from the CDT, it has a separate tax identification number and substantially different beneficiaries. Even if such a top- off provision were to cause the CDT to fail the economic substance test (a result that could certainly be argued), the result at the CDT level would be to disregard the allocation of the class of IRA income and, instead, treat ratable portions of all classes of income as distributed among the beneficiaries. However, because the CDT has only one class of income and has only charitable beneficiaries, the income tax results and a full charitable deduction would be the same.

Moreover, the CDT eliminates the need to set up separate inherited IRAs for each charity named on the IRA beneficiary designation form. The CDT trustee would set up and control a single inherited IRA established for the benefit of the CDT beneficiaries. The CDT trustee, not the charities, would be the driver of the distribution bus and could ensure that a payout of the charitable beneficiary occurs on a timely basis before the Sept. 30 beneficiary determination date. In this manner, the CDT can assist in preserving stretch-out distributions to other natural beneficiaries. In addition, the CDT can assume investment control of the IRA (assuming the account is wholly paid to the CDT) immediately upon signing the single inherited IRA agreement. If there are beneficiaries other than the CDT, the trustee will need to coordinate with the beneficiaries in signing inheritance IRA agreements to unlock the control of the decedent’s IRA.

Other Considerations

While a detailed discussion of the designated beneficiary and IRA stretch-out rules that apply when IRA assets pass to trusts is beyond the scope of this article,15 a few general comments may be helpful. If all IRA assets (or all of the assets of a particular IRA) are payable to a CDT, then, as to such accounts, there’s no designated beneficiary for stretch-out purposes. Thus, the IRA assets must be distributed no later than the end of the fifth year following the decedent’s date of death if death occurred before the decedent attained age 701/216 or over a period not exceeding the decedent’s remaining life expectancy if death occurred after age 701/2.17 As a practical matter, and under typical circumstances, the charitable bequests would be paid out well before these deadlines. If, in the IRA beneficiary designation itself, the CDT is named as a beneficiary along with other natural persons, so that the division occurs as a result of the beneficiary designation and not the division of a single funding trust,18 then, so long as separate accounts are established in a timely manner,19 the continued existence of assets in an inherited IRA account for the CDT won’t affect the stretch-out possibilities of the other natural persons.

If, on the other hand, the CDT is named as the sole beneficiary of an IRA and provides that after making the desired charitable distributions, any remaining assets are to be distributed to other natural persons who would be eligible for stretch-out distributions, then the charitable beneficiaries must be fully paid out before Sept. 30 of the year following the year of the IRA owner’s death. A prudent draftsperson would place this requirement in the document itself, as a reminder of the importance of this date. Once paid out, the charitable beneficiaries won’t be present when the beneficiary designation camera flashes and won’t spoil the stretch-out potential for other natural beneficiaries.20 The separate accounts of the natural persons who receive the IRA benefits remaining after the payment of charitable bequests from the trust should be created no later than Dec. 31 of the year following the year of the decedent’s death. Because the separate accounts were created by a single funding trust and not in the IRA beneficiary designation itself, the applicable distribution period for all natural beneficiaries will be the life expectancy of the oldest beneficiary.21 The inherited IRA accounts for the natural beneficiaries who receive the remaining IRA assets should be set up by the beneficiaries and then funded by a trustee-to-trustee transfer from the assets remaining in the inherited IRA account established for the CDT.

In an environment in which fee-conscious clients heavily scrutinize estate-planning bills, providing for the payment of even modest charitable bequests with the administrative ease of a CDT incorporated into their revocable trust would likely produce tax savings that would more than offset the planner’s fee. The result is an estate plan that pays for itself.

Endnotes

1. Internal Revenue Code Section 691(c).

2. Internal Revenue Service Treasury Decision 9582, Internal Revenue Bulletin 2012-18 (April 30, 2012). See an earlier version published as a proposed Treasury Regulation on June 18, 2008, Vol. 73 F.R. 118, p. 34670.

3. Treas. Regs. Section 1.642(c)-3(b)(2).

4. Treas. Regs. Sections 1.704-1(b)(2)(ii)(b) and (d).

5. Treas. Regs. Sections 1.642(c)-3(b)(2) and 1.643(a)-5(b).

6. Treas. Regs. Section 1.401(a)(9)4, A-4(a).

7. Treas. Regs. Section 1.401(a)(9)-8, A-2(a)(2).

8. IRC Section 642(c)(1) provides that to be deductible, the distribution must be from the trust or estate’s gross income. Tax-exempt income is excluded from gross income and, therefore, a distribution from tax-exempt income isn’t deductible. See also Treas. Regs. Section 1.642(c)-3(b)(1).

9. See IRC Section 681(b) which does, however, potentially allow a charitable deduction for unrelated business taxable income, which resembles that available on an individual income tax return.

10. IRC Section 661(c).

11. IRC Section 642(c)(1).

12. Ibid.

13. See supra notes 8 and 9, as well as Revenue Ruling 2003-123, 2003-50 I.R.B. 1200.

14. Treas. Regs. Section 1.642(c)-3(a).

15. See Natalie B. Choate, Life and Death Planning for Retirement Benefits (Ataxplan Publications, Boston, 7th Ed. 2011), in particular, Chapter 6.

16. Treas. Regs. Section 1.401(a)(9)-3, A-4(a)(2).

17. Treas. Regs. Section 1.401(a)(9)-5, A-5(a)(2).

18. Treas. Regs. Section 1.401(a)(9)-4, A-5(c) and Private Letter Ruling 37044 (2005).

19. Treas. Regs. Section 1.401(a)(9)-8, A-2(a)(2).

20. Treas. Regs. Section 1.401(a)(9)-4, A-4(a).

21. Treas. Regs. Section 1.401(a)(9)-5, A-7(a)(1).