(Bloomberg) -- Time is ticking away for private equity firms to get ready for their next wave of deals.

Rising interest rates, inflation and recession risks have eroded consumer confidence and left buyout firms facing a new reality of higher financing costs and potentially lower returns. None of which changes the fact there’s more than $1 trillion sitting in their funds that needs to be spent.

“People say there’s no financing available but then our clients are telling us ‘we have a big fund that we have to deploy,” said Umberto Giacometti, co-head of financial sponsors in Europe, the Middle East and Africa at Nomura Holdings Inc. “If you need to deploy, say, $10 billion in four years, and don’t do anything for sixth months, you are under pressure.”

The shift is profound for an asset class that for more than a decade was flooded with cash from investors hunting yield in a low-interest rate environment. Those same rates allowed firms to pile debt onto deals to amplify returns, while rising valuations offered exit routes at healthy premiums. So it went, even through the depths of the Covid-19 crisis.

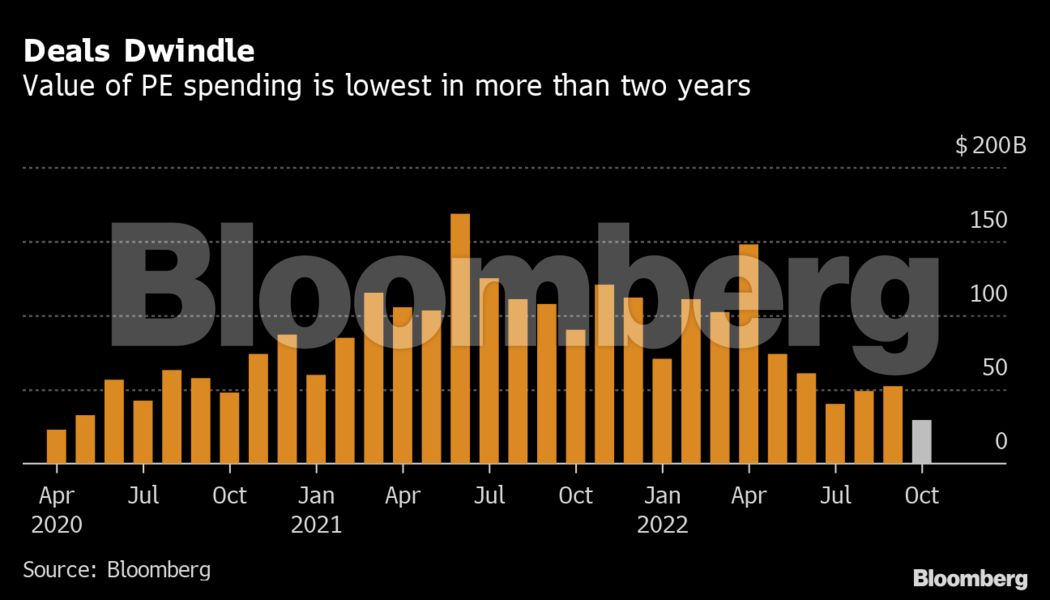

Things began to slow in early 2022 on creeping fears about inflation and rising rates -- trends that accelerated after Russia invaded Ukraine. Private equity spending stands at roughly $30 billion in October, according to data compiled by Bloomberg -- the lowest monthly outlay since early in the pandemic. Some investors have even asked firms to stop deploying capital while they seek to build cash buffers.

Bankers and advisers to private equity firms expect activity to pick up in early 2023, likely in the form of smaller minority transactions and mid-sized buyouts. Depressed stock prices mean take-privates will be a very important source of dealflow, they say, as will secondary buyouts -- whereby one fund sells an asset to another to bring in new investors.

“It’s really not that we’ve got nothing to do, on the contrary,” said Burc Hesse, a corporate private equity partner at law firm Latham & Watkins LLP in Germany. “There’s still lots of dry powder and many buyout firms have closed funds last year, so they will deploy.”

Pressures in the traditional financing markets and higher costs to source alternative private debt mean there’ll be fewer heavily-leveraged mega buyouts. Firms including KKR & Co. are among those ready to write bigger equity checks to get things done, with the hope of refinancing when credit markets improve, or work with a company’s existing debt.

Last week, Thoma Bravo and Sunstone Partners agreed to buy US digital consumer insight company UserTesting Inc. for $1.3 billion. It was Thoma Bravo’s second all-equity deal in October, following its takeover of software company ForgeRock Inc.

Listed buyout firms like EQT AB and Eurazeo SE, meanwhile, will be able to lean on balance sheets to help pay for deals in the absence of cheap debt.

“It’s the return to the all-equity finance LBO and holistic financing solutions,” said Klaus Hessberger, co-head of financial sponsors in EMEA at JPMorgan Chase & Co. “We’re seeing some signs of liquidity in credit markets improving. Until we see a recovery though, I expect more minority and non-change of control transactions.”

Hot Spots

Target sectors in the new cycle will include infrastructure, health care and energy, according to bankers. These sorts of companies tend to find it easier to pass on higher costs to customers, making them attractive to private equity investors, they say.

“One specific deal category where I see a lot of interest is the combination of health care and software,” said Latham’s Hesse. “Funds love it because these businesses are scalable and have projectable recurring revenues in two growth sectors at the same time.”

While volatile markets have made investors more skittish and selective about the private equity firms they’re willing to give money to -- leading to longer fundraising periods and downward adjustments on targets for some -- firms with proven track records in the hottest sectors continue to secure commitments.

Nordic Capital, which likes investing in health care, has just hit its hard cap on a €9 billion ($9 billion) buyout fund. Apax Partners, which also targets health care, as well as tech, raised $10 billion in five months for the first close of its new flagship.

The immediate challenge for those with money to burn is to allocate these funds at a time when it’s only getting harder to predict where rates and company earnings will go, and without the crutch of easy leverage to juice any returns.

“The fact that buyers are becoming more price sensitive is not necessarily a bad thing,” said Hesse. “They are pretty good at finding businesses with sustainable strategies at any point in time.”

Read more: Inside CVC, the Secretive Buyout Firm Heading Into New Waters

© 2022 Bloomberg L.P.