The recent appropriations bill (H.R. 133) and COVID-19 relief provisions, signed into law on Dec. 27, 2020, included a significant change to the interest rate assumptions underlying Internal Revenue Code Section 7702. These interest rates provide the parameters for a contract to qualify as a life insurance policy for income tax purposes. The effect will be to increase the amount of premium that can be deposited into a life insurance policy for a given amount of mortality risk that’s included in the policy contract. The change in the IRC Section 7702 interest rate assumptions is applicable to life insurance policies issued on or after Jan. 1, 2021.

A life insurance policy structured to receive optimal income tax treatment (referred to as a non-modified endowment contract) includes the following unique set of attributes:

- Investment returns within the life insurance policy are deferred from current period income tax(IRC Sections 72(e) and 7702(a)-(g)).

- The owner can take distributions of approximately 85% - 90% of the life insurance policy value on a tax-free basis at any time (IRC Section 72(e)(5)(A)-(C)).

- The deferred taxes are eliminated altogether at the death of the insured (IRC Section 101(a)(1)).

For PPLI policies, which are generally structured to include only the minimum amount of mortality risk needed to achieve optimal income tax treatment, the change in the Section 7702 interest rate assumptions will drive two very favorable outcomes:

1. Increase in premium deposit capacity: An increase in the total premium deposit capacity for each individual that can be insured through a portfolio of PPLI policies, and

2. Lower cost: A reduction in drag on return caused by mortality expense, and a corresponding increase in the investment account value that can be accumulated within a PPLI policy for each premium deposit.

How it Works and What’s Changing

Under Section 7702, a PPLI policy will be treated as a “life insurance contract” for income tax purposes if it satisfies: (1) the cash value accumulation test (CVAT) under Section 7702(b); or (2) the guideline premium test and cash value corridor test (GPT) under Section 7702(c). Both the CVAT and GPT were designed based on a simple principal: the maximum amount of premium or the maximum amount of cash value permitted for a life insurance policy should be capped at the amount required to assure that the policy will endow at the policy maturity date even if the life insurance company delivers only the performance that’s guaranteed under the policy contract.

A PPLI policy will satisfy the CVAT if the cash surrender value of the policy doesn’t at any time exceed the net single premium required for the policy to endow at the maturity date based on the policy’s guaranteed maximum mortality risk expense and the permitted interest rate assumption. Prior to the enactment of H.R. 133, the minimum permitted interest rate assumption for the CVAT calculation was 4%. For policies issued in 2021, the minimum permitted interest rate for the CVAT calculation is reduced to 2%. For policies issued in 2022 and thereafter, the minimum permitted interest rate will be a floating rate.

A PPLI policy will satisfy the GPT if the premium deposits don’t exceed the greater of the Guideline Level Premiums (GLPs) or the Guideline Single Premium (GSP) required for the policy to endow at the maturity date based on the policy’s guaranteed maximum mortality risk expense, the policy’s guaranteed maximum administrative fees and charges and the permitted interest rate assumption. In addition, the policy must meet the minimum net amount at risk requirement defined under the statute (a ratio for which the numerator is the life insurance proceeds payable at the death of the insured and the denominator is the policy cash surrender value) based on the insured’s age.

- Prior to the enactment of H.R. 133, the permitted interest rate assumption for the GSP calculation was 6%. For policies issued in 2021, the minimum permitted interest rate for the GSP calculation is reduced to 4%. For policies issued in 2022 and thereafter, the minimum permitted interest rate will be the floating GLP rate plus 2%.

- Prior to the enactment of H.R. 133, the minimum permitted interest rate assumption for the GLPs calculation was 4%. For policies issued in 2021, the minimum permitted interest rate for the GLPs calculation is reduced to 2%. For policies issued in 2022 and thereafter, the minimum permitted interest rate will be a floating rate.

In the future, the Section 7702 interest rate assumptions will be adjusted at the outset of a calendar year based on the lesser of: (1) the rate prescribed in the National Association of Insurance Commissioners’ Standard Valuation Law, or (2) the average mid-term applicable federal rate over the 60-month period that ends two calendar years prior to the adjustment year. While this language is complicated, the timing is intended to give the life insurance companies sufficient opportunity to adjust their product features and administrative systems to accommodate the changing interest rate assumptions. Once adjusted, the new Section 7702 interest rate assumptions will be applicable for each PPLI policy issued during the calendar year. Furthermore, the Section 7702 interest rate assumption applicable when a PPLI policy is issued will generally remain in effect for the entire time that PPLI policy exists.

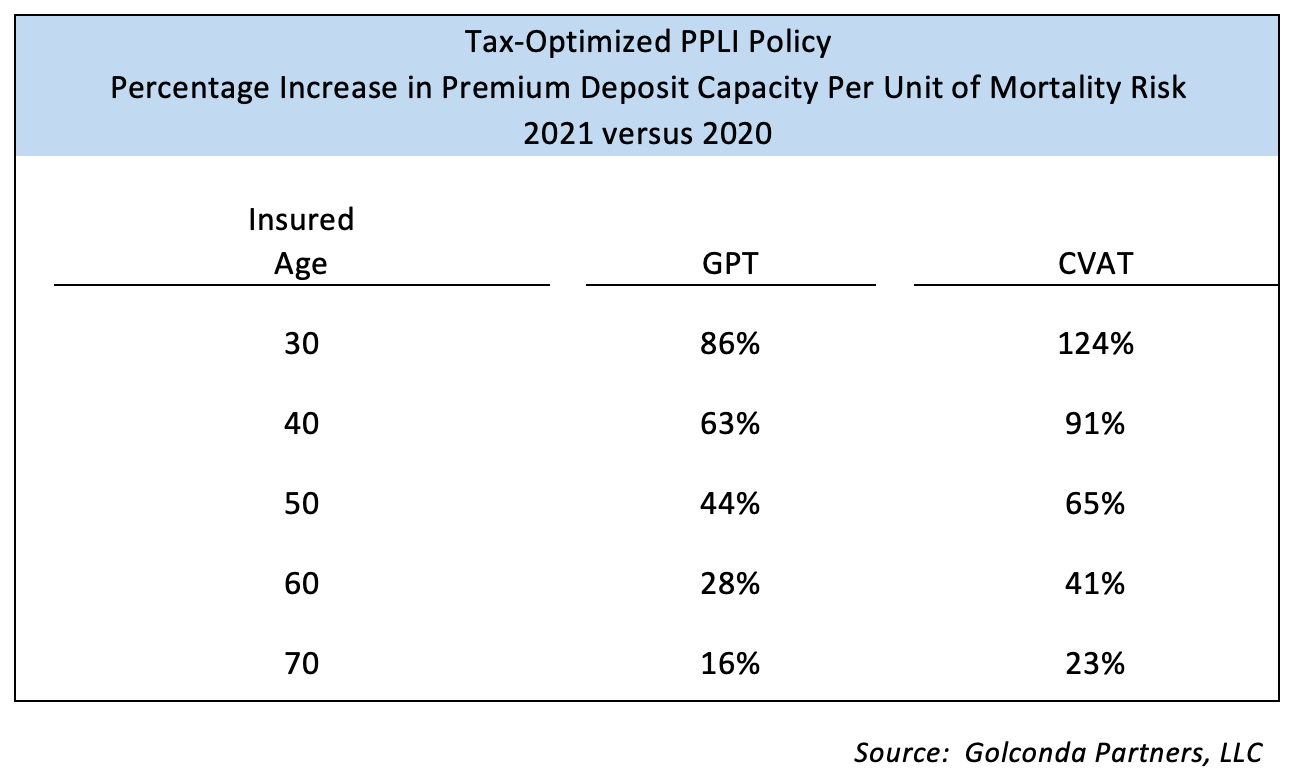

Increase in Premium Deposit Capacity

The amount of premium that HNW families are permitted to deposit into tax-optimized PPLI policies can be limited by the total amount of mortality risk that can be aggregated by life insurance companies and their reinsurers. The premium deposit for any insured is constrained by this overall mortality risk limitation and may be further constrained by the amount of coverage that can be underwritten financially (based on that insured’s financial status). The expansion of premium deposit capacity will enable many HNW families to increase the portion of their investment portfolio that can be shielded from income tax through the use of PPLI policies.

The percentage increase in premium deposit capacity for a tax-optimized PPLI policy acquired in 2021 will be a function of the age of the insured individual. The younger the insured individual, the greater the impact of the change in Section 7702 interest rate assumptions.

Lower Cost

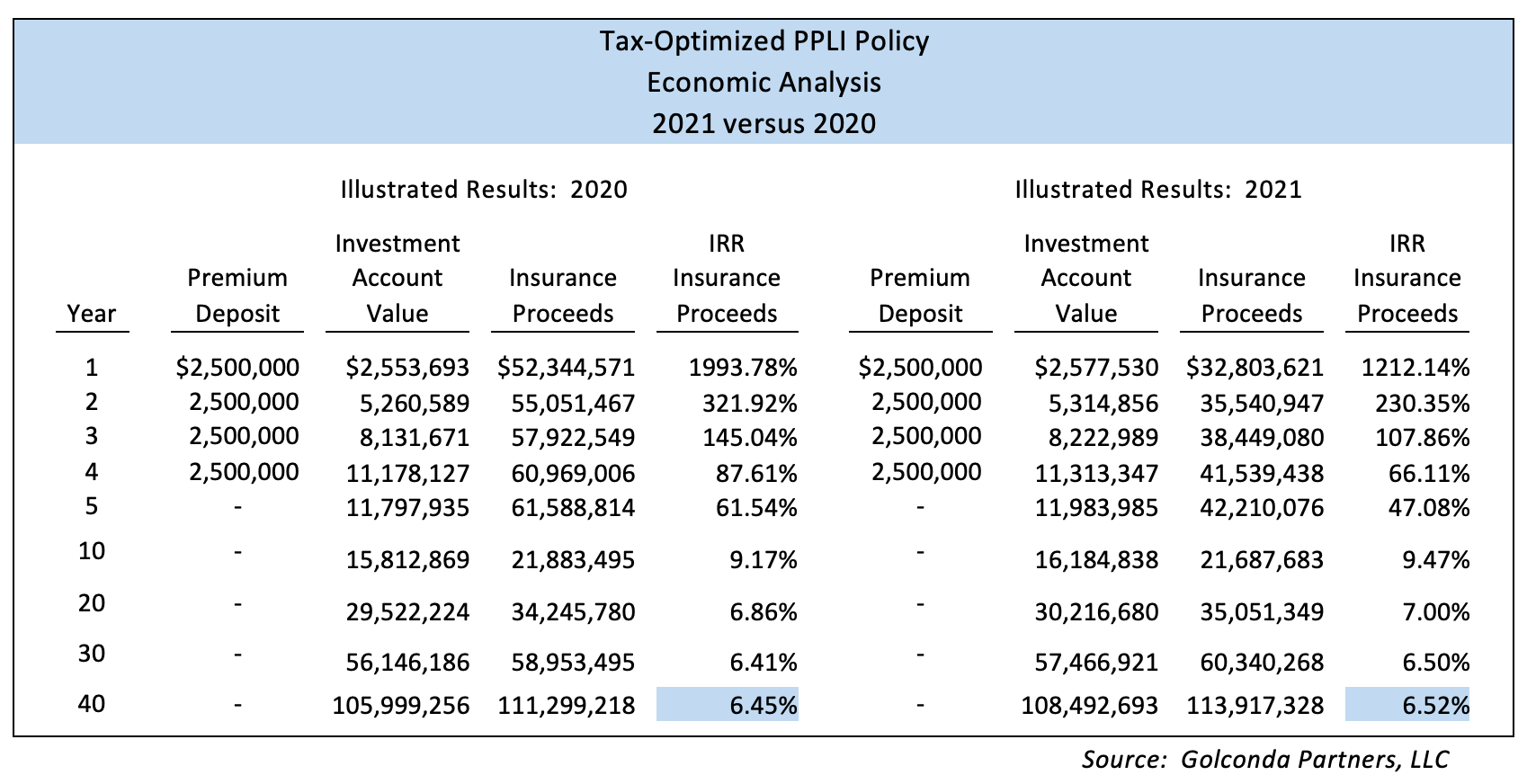

In most circumstances, a PPLI policy will be structured with the minimum amount of mortality risk required under Section 7702, because that structure enables an optimization of income tax results at the lowest cost. The change to the Section 7702 interest rate assumptions will enable PPLI policies issued in 2021 to achieve tax-optimization with lower amounts of mortality risk. The reduction in mortality risk will drive a corresponding reduction in the mortality charge component of the PPLI policy, resulting in a lower drag on the investment account return each year. The net effect will be an improved performance and greater accumulation of value in the policy investment accounts.

The table below compares the illustrated results for a tax-optimized PPLI policy that is structured to accept $10 million of cumulative premium deposits over four years, insures the life of a 50-year-old Male, and is assumed to earn a 7% return, net of investment management fees:

Tipping the Scales

The change to the Section 7702 interest assumptions will have a positive impact on PPLI policy premium deposit capacity and performance and should result in an increase in demand among HNW families.

Moreover, there’s is a strong possibility that Congress will enact legislation in 2021 to increase income tax rates and decrease estate and gift exemption amounts for HNW families. If that happens, the combination of greater premium deposit capacity and lower cost for PPLI policies could tip the scales for families that have been considering the acquisition of PPLI policies but haven’t yet taken action.

Michael Liebeskind is the founder of Golconda Partners, LLC, and Bryan Bloom is a tax partner at Faegre Drinker Biddle & Reath LLP.

The authors wish to express their gratitude to Gabe Schiminovich for his assistance with the preparation of this article.