Costs rose 7 percent among family offices globally from the year prior, even as they saw a 2.4 percentage point drop in the returns on an average portfolio, according to a new report.

A great deal of the total cost increase among global family offices is due to an across-the-board rise in administration costs from 15 percent in 2013 to 24 percent in 2014, according to the 2015 Global Family Office Report. In the report, UBS and Campden Research surveyed the leaders of over 224 family offices globally, with about 76 based in North America. The average size of the firms participating had $806 million in assets under management.

According to Charlie Buckley, head of UBS Americas’ global family office coverage, “increased sophistication in the tax code complicates multigenerational issues” and requires family offices to hire more employees with greater expertise in order to find the same (or lower) level of success.

To go along with the increased costs, returns are lagging, the report states.

Dollar-based returns across the family offices surveyed, while still positive, dropped to 6.1 percent from the 8.5 percent reported in 2013 amid diminished asset performances, most notably in equities.

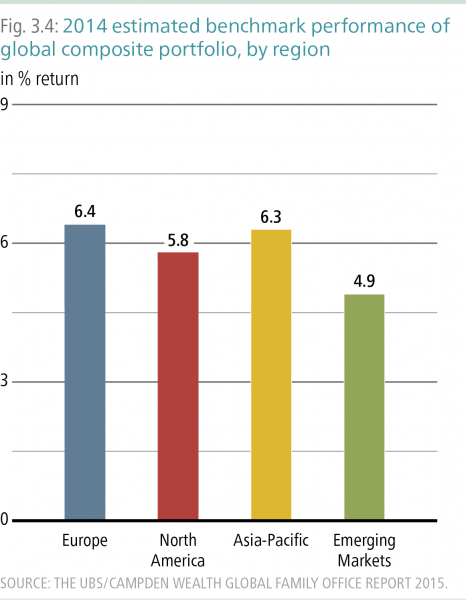

North American-based family offices saw the biggest drop in investment performance, close to 4 percentage points, from 2013 to 2014. The report found returns among U.S. family offices dropped from 9.9 percent in 2013 to 5.8 percent in 2014, due to record low interest rates, volatility and underwhelming performances by equities and alternative products.

To gain returns, family offices are increasingly taking on more risk, Buckley says. The percentage of family offices following a preservation strategy has fallen by 5 percentage points, down to only one in five offices now.

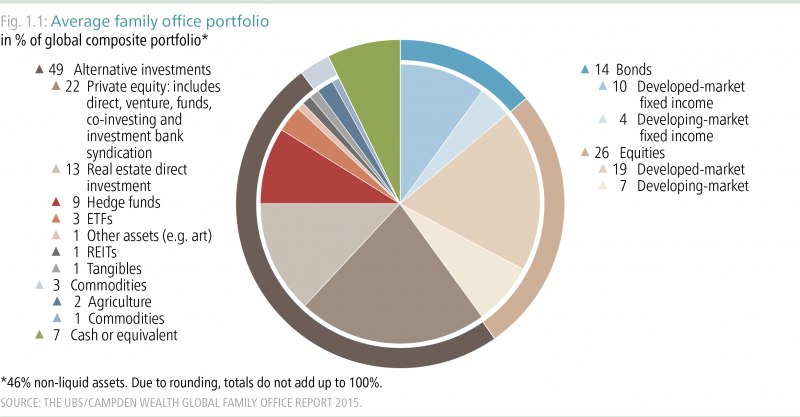

Meanwhile, almost half of the average U.S. family office investment portfolio is allocated toward alternatives — namely real estate and private equity, particularly around venture capital and co-investing. The average U.S. family office reports about 19 percent of the portfolio is allocated toward private equity, including direct, venture, funds, co-investing and investment bank syndication, with 11 percent toward real estate and 12 percent in hedge funds.

Real estate remains a core asset because families, particularly those operating businesses within that market segment, like investing in areas that are known to them, Buckley said.

The dragging performance extends to philanthropy as well. Though the report notes that the average family office donates 2.5 percent of its AUM to charity annually, delving further into the numbers reveals that this figure is probably significantly lower for the typical family office (insomuch as any family office can be deemed “typical”).

A combined 53 percent of respondents noted that they donate either 1 percent or less annually, suggesting that the stated average may be being bolstered by large donors.

Buckley maintained that philanthropy is “just not something that a lot of families have done particularly well. More families should be as strategic with their philanthropic efforts as they are with their investments.” In response to questions about the average annual donation of the typical family office, he agreed that “1 percent to 2 percent is likely more reflective than 2.5 percent.”

{kind=link}