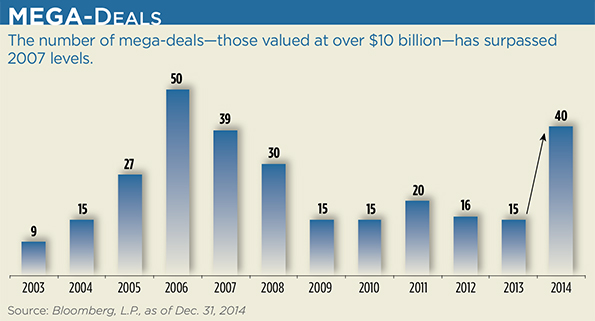

At a total of $3.6 trillion in transactions, 2014 was the most active year for mergers and acquisitions since just before the global financial crisis. This year is on track to surpass that, with deals totaling $1.9 trillion year-to-date through June 3, according to Invesco. Forty of the transactions that occurred last year were “mega-deals”—those valued at over $10 billion—the largest number of these deals since 2006. Typically this is a warning sign; many market observers see it as an omen we’re nearing the end of the credit cycle, and a market top.

“Historically, market tops have been preceded by very rapid growth and large speculative transactions that require aggressive financial assumptions,” said Tony Wong, head of global research at Invesco and author of a recent research report on M&A activity. “Many company management (teams) have decided they’d rather buy than build. They’ve moved more away from capex and looking at M&A as an easier path.”

Recent deals include: Intel buying chip maker Altera for $16.7 billion; semiconductor Avago agreed to buy Broadcom for $37 billion; Charter Communications said last month it plans to buy Time Warner Cable for $55.3 billion; and CVS Health Corp. will buy Omnicare, which provides prescription medicines to nursing and assisted living facilities, for $10.1 billion.

“That’s kind of a natural impulse for guys who have been running companies through three or four pretty good years, where their stock’s been going up and they’re generating pretty decent earnings and getting big bonuses,” said John Rubino, who manages the financial website DollarCollapse.com and co-author of The Money Bubble. “Their egos take over, and they start wanting to build empires.”

Rubino says there are a number of indicators that the market is at the peak of the cycle, but few speak as loudly as the surge in M&A activity.

“It’s a thing that indicates that rich people have way too much money, and they’re starting to do dumb stuff with it,” he said.

One characteristic of M&A activity near the market top is that more transactions are done for cash than equity. In these deals, the company either has to use existing cash on their balance sheet to finance the transaction, or they have to borrow in the market to pay for it. And if a company has to add a significant amount of debt, it reduces its credit-worthiness.The announcements are made with rosy assumptions about potential synergies; by some measures, valuations are stretched, there is more speculation and financial buyers like private equity firms are more active. Often, these waves of mergers end when money tightens, and it's followed by an increase in credit downgrades.

Less All-Cash Deals

But Wong suggests the end of the M&A boom may not be as dire as some believe. For one, the number of all-cash deals is down from previous years. In 2007, 70 percent of the deals were all-cash, while year-to-date it’s about 40 percent.

Another thing that’s different about this M&A environment is the composition of the buyers.

“The preponderance of transactions this year and 2014 as well has been lead by strategic buyers, rather than financial buyers,” Wong said. “These are companies looking either to defend their existing market positions; they’re looking at consolidating their area of the market; they’re trying to drive greater margin enhancement by taking out one of their competitors.”

In 2007, private equity was responsible for about half of the M&A volumes; today’s it’s less than 20 percent, Wong said. One reason we don’t see financial sponsors as active is because of the bank capital rules that came out Dodd-Frank, Wong said. There is much greater regulatory scrutiny and oversight around highly levered deals.

But Rubino believes M&A is looking more like it did in 2007—and not in a good way.

“The fact that they’re being funded one way or another, or the companies say they’re strategic rather than financial—that’s completely meaningless,” he said. “The fact is, corporations are taking on huge amounts of debt to do share buy backs and to pay dividends.”

As of the second quarter of 2014, global corporate debt levels were up 5.9 percent since 2007 to $56 trillion, according to McKinsey.

“These deals look so good on paper, and there are all these potential synergies. But when the market turns down, it turns out they overpaid by 50 percent. So synergies didn’t really matter because they overpaid so dramatically.”

Wong believes we could see more transactions this year in the telecomm, media and technology space, in the healthcare sector and in energy and commodities.

But trying to play the M&A market by buying companies believed to be prime takeover targets is a dangerous game.

“Rather than trying to participate in it, now would be the time to consider selling (the) stocks (of firms) participating in it,” Rubino said. “When you see lots of different things hitting records, it’s time to get defensive.”