By Brian Chappatta

(Bloomberg Opinion) -- Exchange-traded funds have never quite been a perfect fit for the bond market. In fact, some of the main selling points of ETFs — real-time pricing, instant liquidity and the ability to trade at a low cost — run counter to some of the core tenets of traditional fixed-income investing. The buy-and-hold types don’t need to know precisely where their portfolio is trading at any given time, nor do they have much reason to liquidate or trade frequently.

And yet money is pouring into the funds at an unprecedented pace. Perhaps it’s fast-money traders, or maybe it’s just so much easier to click a button and buy one than to purchase bonds individually. According to data compiled by Bloomberg Intelligence, fixed-income ETFs have experienced about $74 billion in inflows so far this year, on track for the biggest first half on record. In total, the funds have assets of almost $743 billion, with some standouts including the iShares 20+ Year Treasury Bond ETF, or TLT, and the iShares 7-10 Year Treasury Bond ETF, or IEF. Prices of both have climbed as benchmark U.S. yields have tumbled — TLT is up more than 11% in 2019.

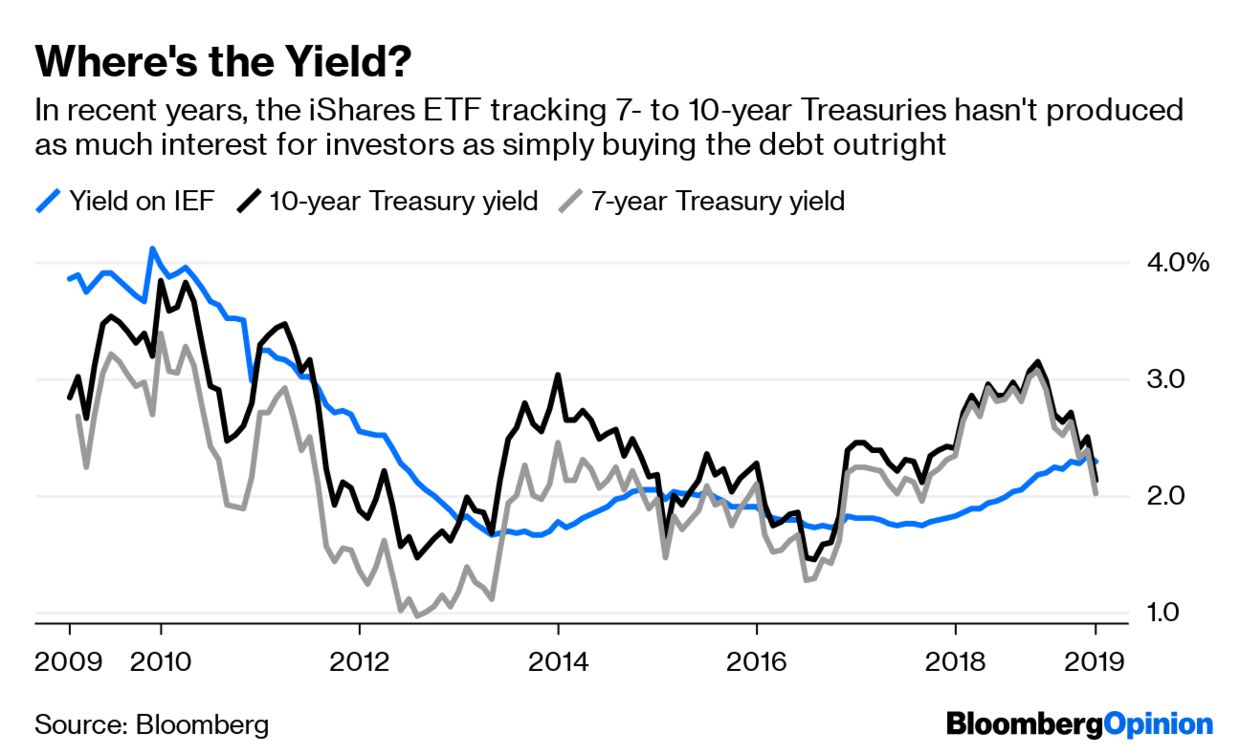

For those who owned TLT around the turn of the calendar year, it has clearly been a great ride. The question going forward, though, especially for those aforementioned buy-and-hold investors, is how it will hold up given that Treasury bond yields are within 50 basis points of their all-time lows. If interest rates rise sharply, investors could face a trillion-dollar wipeout. But even if they continue to fall, as most market watchers now expect, that can end up distorting the yield on an ETF in the future relative to the prevailing market level. Here’s a chart of IEF versus 7-year and 10-year Treasury yields (note the gap from roughly late 2016 up until recently):

Surely some investors might have wanted to lock in those elevated yields toward the end of the year but didn’t know how. Again, it’s far easier to push a button on a brokerage website or mobile app then it is to apply separately for a TreasuryDirect account or purchase a basket of diverse over-the-counter corporate securities.

It turns out there’s a happy medium, in a niche segment of the ETF universe that’s steadily raking in cash. Invesco Ltd.’s BulletShares and BlackRock Inc.’s iBonds are both suites of fixed-income ETFs that actually look and act like bonds.

The pitch is so straightforward it’s a bit surprising that the funds still remain relative unknowns. Invesco and BlackRock each have investment-grade corporate-bond ETFs with maturities from 2019 through 2028 — and in each of those funds, they buy only bonds with matching due dates. The idea is mainly that investors will construct a “ladder” by spreading their money across each of the funds, which will pay steady interest and ultimately return the net asset value. This is one of the most classic bond-buying strategies because individuals can reinvest principal in longer-dated debt if interest rates increase or pocket the funds and go elsewhere if yields dip too low. Invesco also offers high-yield and emerging-markets ETFs, while BlackRock has high-yield and municipal-bond funds.

“In an environment like this, where the perceived uncertainty is so high, clients take comfort in knowing that I can just forget about trying to figure out where rates are going,” said Jason Bloom, Invesco’s director of global macro ETF strategy. BulletShares, with about $11.2 billion in assets, “is solving a lot of the logistical problems that investors face today,” most notably the amount of time and transaction costs needed to amass a diversified portfolio of bonds one at a time.

Karen Schenone, a fixed-income product strategist at BlackRock, says she talks to new potential users of iBonds almost every day. The suite has grown to about $8 billion in assets, with $1.2 billion entering through the first five months of 2019. About $195 million came from direct platforms, she said, signaling growing acceptance among individual investors. Financial advisers were the early adopters as they sought to cut down on expenses and the headaches associated with buying small pieces of debt offerings.

“It’s an elegant solution and a more known investment result,” she said. “The estimated yield at the beginning is the total return you get at the end of it.”

This strikes at the core of what long-term, fixed-income investing is all about. In a world in which $13 trillion of debt has negative yields, it’s easy to forget that plenty of individuals look to buy bonds to align with life events and goals, like sending a child to college or purchasing a home. ETFs have revolutionized the ease with which people can invest in the equity markets, but passive ETFs with perpetual duration that are exposed to the most-indebted borrowers can’t quite mimic that traditional role of fixed income.

Of course, it’s becoming more difficult to make bonds work this way, given that global yields are so low. As I wrote last week, central banks are creating a horde of zombie investors who feel they have little choice but to plow into riskier and riskier assets to meet their return objectives. That’s partly how you end up with a situation like H2O Asset Management.

As long as interest rates remain positive in the U.S. — the iBonds Dec 2028 Term Corporate ETF yields more than 3% — these defined-maturity bond ETFs should continue to gain traction among the cohort of fixed-income traditionalists. It’s no secret that the bond market is evolving; high-yield ETFs might actually help with liquidity, there’s now a muni ETF that invests in other muni ETFs, and, crucially, electronic marketplaces are gaining more widespread acceptance. If an investor wants to allocate some money to fixed-income markets, there’s no shortage of options.

But “exposure” to bonds is not quite the same as investing in them. Defined-maturity ETFs are a useful way to bridge that divide. With markets and the Federal Reserve at a crossroads, laddering up could prove a way to stay balanced amid all the crosscurrents that Jerome Powell has warned about.

To contact the author of this story:

Brian Chappatta at [email protected]

To contact the editor responsible for this story:

Daniel Niemi at [email protected]