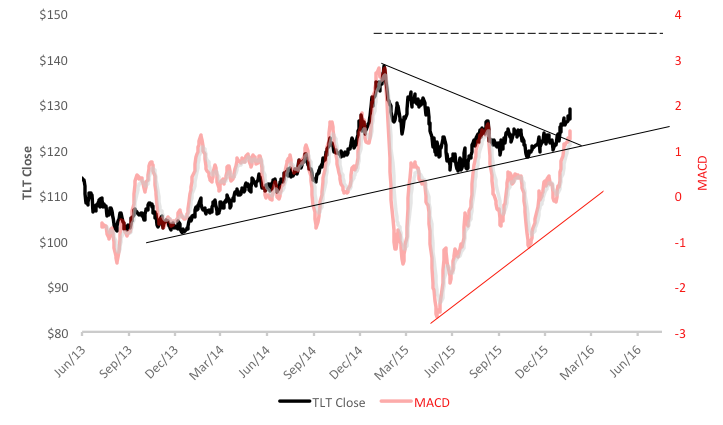

After all the harum-scarum with oil and equities, the Treasury bond market’s beginning to look a little pricey. Lots of people are stashing their loot in Uncle Sam’s mattress nowadays. You can see this especially reflected in the chart of the iShares 20+ Year Treasury Bond ETF (NYSE Arca: TLT) which tracks the long-dated segment on the Treasury yield curve. TLT Shares, now trading around $128, have broken to the upside of a consolidation area and are eyeing a technical advance to the $145 level. By technical I mean the move could be derailed by extraneous circumstances, like Fed curve balls or interplanetary war. Still, the chart’s pretty compelling:

Now, if I was a betting man, I’d say a 12 or 13 percent gain in a matter of a few months is interesting but not a screaming buy. After all, forking over $128 a share for a round lot can put a big dent in one’s wallet.

No, a betting man or woman can get a lot more bang for the buck using LEAPS: Long-term Equity AnticiPation Securities. LEAPS are option contracts with maturities stretching out years rather than merely weeks or months. Buying deep-in-the-money LEAPS calls can give you a fund share proxy for pennies on the dollar. “Deep in the money“ means contracts with strike prices at least 10 percent below TLT’s current market price. A January 2018 LEAPS call struck at 115 could, at the time this is being written, be purchased for $16 a share. The call gives you the right, but not the obligation, to buy 100 TLT shares at $115 a share at any time through the January 2018 expiration date.

The call’s delta – its sensitivity to TLT’s price movement – is currently .73, meaning the contract would likely appreciate 73 cents for every $1 uptick in the fund’s value. Today. But, if the call goes deeper in the money over time – meaning TLT rises further above the strike price – its delta will actually increase, making the contract behave more and more like fund shares themselves. Ultimately, at expiration, the delta will be 1.00 if the call remains in the money, or zero if it’s not.

Let’s say TLT rises to $134 by the end of June. Even with a moderate decline in volatility, the call could be worth $20 a share at a .85 delta. That’s a 25 percent gain. If you’d bought TLT shares instead, you’d make just 3 percent on the move.

And if you’re wrong? If a central bank knuckleball beans you or an Arquillian cruiser lights up New York, your LEAPS call could lose ground. Ultimately, in 2018, if TLT’s not above $115, it could expire worthless. That would mean a $16 loss. You’d suffer a similar dollar loss if you owned TLT shares at $112, assuming you bought them at today’s price. But then, the profit/loss picture is reversed: a 100 percent loss for the call; only a 13 percent hit for the fund shares.

For those betting on further yield erosion on the long end of the curve, at least in the near term, LEAPS could be the odds-on favorite. Now, where’s the $2 window?