In spite of what you may think, it’s really a great time to be in the oil business. That is, if you’re a refiner. The fund runners at Van Eck Global like refiners so much, in fact, they launched the Market Vectors Oil Refiners ETF (NYSE Arca: CRAK) last week. CRAK is a first-of-its-kind exchange-traded portfolio tracking more than two dozen refiners around the globe.

Refining, unlike other energy segments, generally does well when oil prices fall. Refiners do very well when crude plummets precipitously. It’s not hard to figure out why. The clue is in the Van Eck ETF’s ticker symbol.

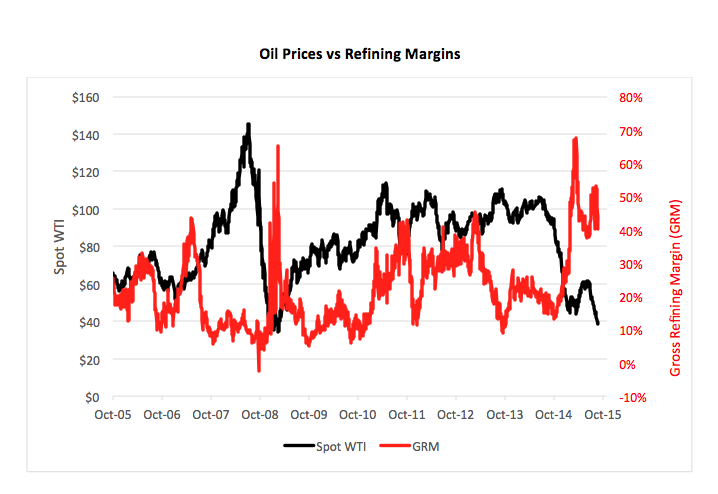

Refining operations live and die by the “crack spread” – the difference between crude oil input costs and the sale proceeds of refined products such as gasoline and diesel fuel. Cracking cheaper oil into not-so-cheap distillates makes for wider profit margins. And that’s been refiners’ formula for success this year.

Year to date, prices for spot WTI, the benchmark US crude oil grade, have sunk 26 percent. Meantime, wholesale prices for unleaded gasoline have eased just 15 percent while diesel prices have slipped 22 percent.

A typical refining benchmark is a “3-2-1” crack – three barrels of crude turned into the equivalent of two barrels of gasoline and one barrel of diesel fuel – meaning refiners are selling more expensive petrol than cheaper diesel.

Right now, the gross refining margin for a 3-2-1 operation is over 40 percent, well above its five-year average of 27 percent. These are, indeed, rich times for refiners, a condition not lost on Van Eck.

{kind=link}

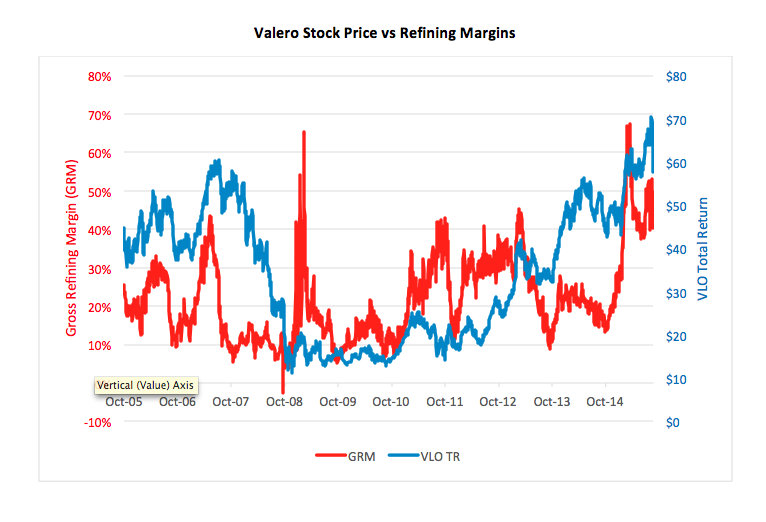

It’s a situation, too, noted by stockholders of independent refiners like Valero Energy Corp. (NYSE: VLO). VLO, accounting for eight percent of CRAK’s underlying index, is up 19 percent this year.

If you’re a believer in lower or stable crude prices going forward, CRAK could be a decent wager. Stocks like VLO, for the most part, move in step with refining margins. And, at about $18 a share, purchasing CRAK is less capital intensive than the $57 buy-in for VLO.

{kind=link}

Just keep in mind the relationships depicted in the charts above: crude oil prices and refining margins are negatively correlated while VLO (and, presumably, CRAK) is positively correlated to margins.

Brad Zigler is REP./WealthManagement's Alternative Investments Editor. Previously, he was the head of marketing, research and education for the Pacific Exchange's (now NYSE Arca) option market and the iShares complex of exchange traded funds.