Our recent article highlighted the stellar returns earned this year by exchange traded funds tracking crude oil futures. Contango, the inherent cost of holding these ETFs, was front and center in the article.

We pointed to three ETFs designed to curtail the deleterious effect of contango and offered to examine them in some detail in a future column. This is that column.

The oldest of the lot, launched in early 2007, is the Invesco DB Oil Fund (NYSE Arca: DBO), a portfolio that optimizes its forward roll with an algorithm that selects the contract month with the most advantageous yield over a 13-month horizon. That’s not to say that each roll will yield a positive result; it merely means that an expiring contract will be rolled into an eligible contract month presenting the smallest contango or the greatest inversion.

Just a few months younger than DBO, the United States 12-Month Oil Fund (NYSE Arca: USL) is the kid sister of the United States Oil Fund (NYSE Arca: USO). USO offers constant front-month exposure to the crude oil market while USL stretches its contract positions over each of the upcoming 12 delivery months. Thus, USL attacks the contango problem structurally rather than tactically.

Debuting in late 2016, the new kid on the block is the ProShares K-1 Free Crude Oil Strategy ETF (BATS: OILK). OILK differs from the older funds in two ways. First, the ProShares ETF is actively managed, allowing its portfolio runners free rein to select a forward roll target over the ensuing three delivery months. Second, OILK is organized as a ’40 Act fund that subjects its holders to a 20%/39.6% tax scheme on short-term/long-term capital gains. USO, USL and DBO are commodity pools that issue K-1 returns. Annual mark-to-market taxation at a blended 27.8% rate ensues for these older portfolios.

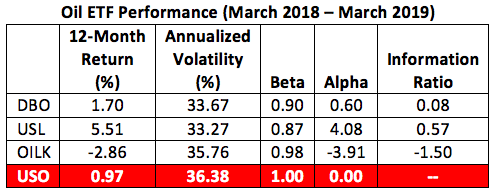

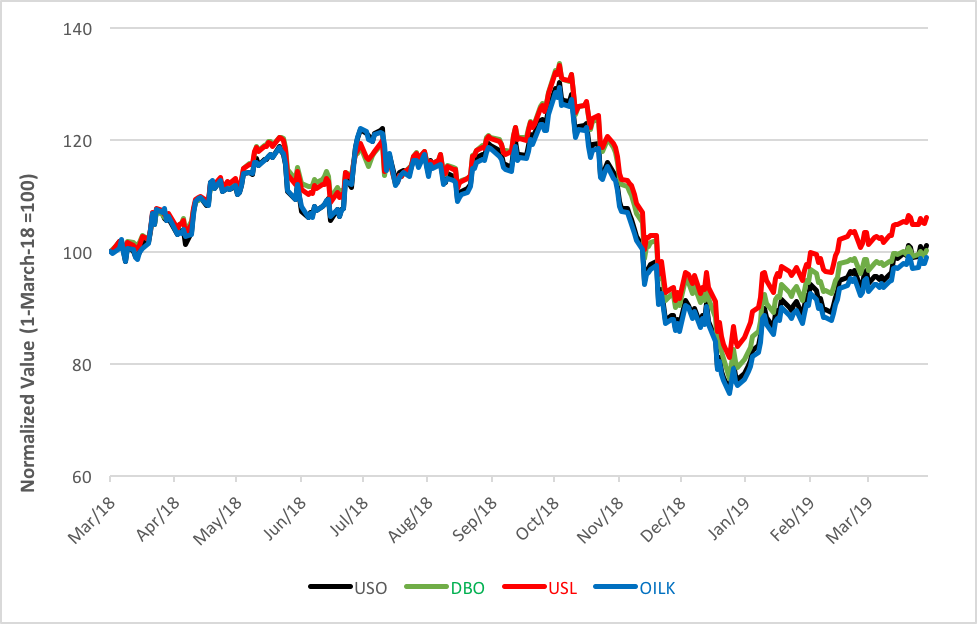

Oil ETF performance, to no one’s surprise, is driven by the shape of the futures curve. Over the past year, USL gained an advantage by mechanically rolling into a steadily diminishing contango as a bull market developed at the beginning of the year.

Each fund’s information ratio bespeaks the efficiency of its approach. The ratio measures the payback earned for taking active risk, using USO as a baseline. Spreading forward roll risk across the futures curve served USL well, while OILK’s three-month roll horizon has clearly been a constraint.

And what of the future? Technically, spot WTI crude seems ready to test the $75 level for a further $10 gain. And, as of this writing, futures have slipped into backwardation. If both the bull market and the inversion persist, the advantage could actually tip toward the front-month-loaded USO fund.

Historically, however, such an advantage has proved short-lived. Over the past decade, the contango fighters have handily outdone the USO fund, so it’s good to be prepared for the next market shift.

Brad Zigler is WealthManagement's alternative investments editor. Previously, he was the head of Marketing, Research and Education for the Pacific Exchange's (now NYSE Arca) option market and the iShares complex of exchange traded funds.