Clients generally have several key desires regarding their trust planning. These desires, prioritized differently by each client, are: some form of governance structure for the family trusts; privacy; control and flexibility regarding trust administration and investment management; family promotion of social and fiscal responsibility inter-generationally; and tax and asset protection benefits.1 Since the mid-1990s, modern trust structures, such as directed trusts, special purpose entities/trust protector companies (SPEs/TPCs) and private family trust companies (PFTCs), have allowed families to successfully integrate these key desires into their trust planning. Consequently, the amount of gifting to trusts by the wealthy has increased dramatically from 12.5 percent in 1995 to 40 percent currently.2

Despite this trend, it’s important to note that 70 percent of families typically name family members, business colleagues and friends as trustees of their trusts3 without the advantages of these modern trust structures, which limits their ability to integrate these key desires into their trust planning. As more families and their advisors familiarize themselves with the advantages and operation of these modern trust structures, their use and popularity will only continue to grow, as has been the case since the mid-90s.

One of the more popular modern trust structures is the modern PFTC, used by the ultra-wealthy (that is, families generally with net worths well in excess of $100 million or more). Wealthy families, both above and below the $100 million net worth threshold, also use directed trusts and SPEs/TPCs as trust structures that provide trust planning solutions to answer their key desires. There are many similarities among these three structures, allowing families at all net worth levels to accomplish their desired goals.

PFTC Formation

As previously mentioned, families have typically chosen family members, advisors and/or commercial trustees with whom they’ve had personal, professional or business relationships over the years as their trustees. PFTCs allow these individuals to still participate in the family operations while also providing them additional governance, structure and support, all while dramatically reducing their personal liability and providing many other key advantages.

A PFTC is generally a limited liability company (LLC) or corporate entity4 that’s typically 100 percent owned by the family and qualified to do business in the PFTC jurisdiction, usually after acceptance by the jurisdiction’s Division of Banking (DOB). The PFTC then typically works with the family office, often located in the client’s resident jurisdiction, via a service agreement to provide related services, such as investment advisory and management and asset allocation, as well as illiquid asset, real estate and private equity management.

PFTCs may be either regulated or unregulated. The regulated PFTC generally receives a charter, and the unregulated PFTC usually receives a license. The question of whether to establish a regulated or an unregulated PFTC is an important one. Many families select the regulated PFTC option to obtain the Securities and Exchange Commission (SEC) registration exemption,5 as well as help to prevent the ability to pierce the corporate veil. The formalities associated with the regulated PFTC, such as a charter, capital requirements,6 state audits, policy and procedures manuals and compliance all help to ensure that the PFTC is a properly functioning entity and trustee. Many unregulated PFTCs also follow many of the formalities of the regulated PFTCs to strengthen their position as viable trustee alternatives and hopefully prevent the ability to pierce the corporate veil. Other unregulated PFTCs simply have the corporate agent hold their license in a drawer without many, if any, formalities, which could prove to be potentially problematic.

Selecting a Jurisdiction

Typically, the PFTC is located in a jurisdiction with favorable PFTC laws, as well as favorable trust, asset protection and tax laws. Some of the more popular PFTC jurisdictions are Nevada, New Hampshire, South Dakota, Texas and Wyoming.7 Some of the newer jurisdictions enacting legislation are Florida, Ohio and Tennessee.8 When selecting a PFTC jurisdiction, many families typically consider the:

• jurisdiction’s PFTC laws;

• support of the PFTC state legislature and governor;

• experience and support of the jurisdiction’s DOB office in handling PFTCs

• important with regulated PFTCs for SEC exemption purposes

• whether a jurisdiction has an accredited DOB;9

• experience of a corporate agent in the PFTC jurisdiction to assist with the PFTC formation, ongoing operation, compliance and formalities;

• experience of a trustee agent in that jurisdiction to provide trust administration;

• trust, asset protection and tax laws of that jurisdiction;10

• dynasty trust/rule against perpetuity statutes;11 and

• economic conditions of the PFTC jurisdiction.12

Ownership Structure

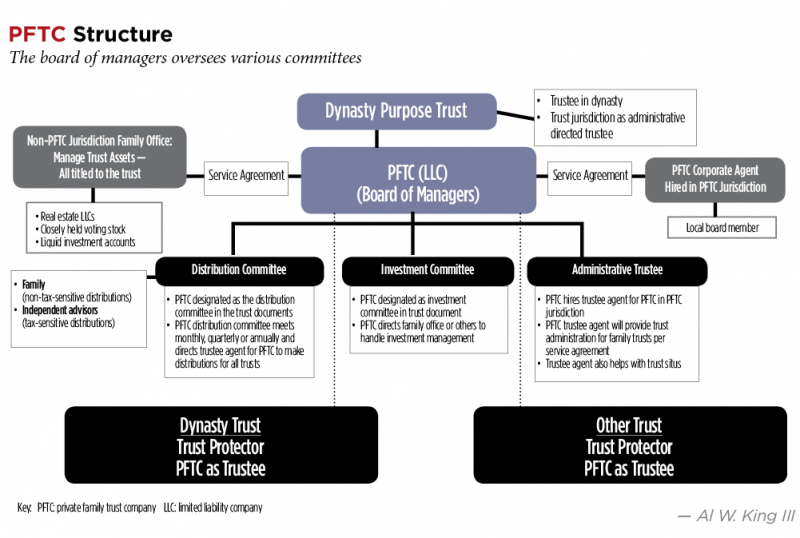

The PFTC ownership structure varies with each family. The most popular organizational entity for the PFTC is generally an LLC, which is usually owned by one or more of the following: (1) outright by the senior family member; (2) a purpose trust with dynasty provisions13 and no beneficiaries, whose sole purpose is to care for and perpetuate the PFTC; (3) non-purpose dynasty trusts with family member beneficiaries; or (4) family trusts. The internal governance of the PFTC is generally structured similar to a corporation with a board of managers/directors that specifically appoints and works with separate committees, each comprised of family members and their trusted advisors. Typically, the committees are responsible for trust distributions and trust investments. Sometimes, the investment and distribution committees are combined as one or even as part of the board of managers. (See “PFTC Structure,” p. 11.) The requisite number of board members varies among the PFTC jurisdictions,14 generally ranging from a minimum of three to a maximum of 12. Further, while a few of the PFTC jurisdictions may not require it, most families prefer to have at least one resident board member15 to provide a better nexus to the PFTC, which can prove to be very beneficial.

Situs Requirements

The PFTC formation jurisdiction will often require the regulated PFTC to have an office located there.16 Families will typically hire the services of a corporate agent in the PFTC situs jurisdiction to fulfill this PFTC requirement. Consequently, the corporate agent provides a local nexus and gives a family the minimum statutory contacts necessary for the jurisdiction’s PFTC application process, as well as for the ongoing operation of the PFTC. For example, a corporate agent in a regulated PFTC jurisdiction might maintain three contracts with a family office in that jurisdiction: (1) a lease for office and vault space; (2) a service agreement to answer the telephone, receive faxes, forward mail and provide service of process; and (3) an arrangement for the corporate agent to serve as the local PFTC director. These services generally provide the requisite contacts with the PFTC jurisdiction without burdening a family with the duties of seeking out, hiring and monitoring a staff in the PFTC jurisdiction, although many families do elect to hire staff in the PFTC jurisdiction.

Moreover, while a corporate agent will generally satisfy the statutory situs requirements of a PFTC, it may not be sufficient for maintaining a trust situs in the PFTC jurisdiction. If this added benefit is desired, some corporate agents can also act as a trustee agent to accomplish this end or, alternatively, the PFTC can hire a separate trustee agent, who’s independent of the corporate agent, to meet this objective. A trustee agent hired by the trustee PFTC can provide the necessary trust administration services in the PFTC jurisdiction to validate trust situs in the PFTC jurisdiction, allowing the family via its PFTC to benefit from the favorable trust, asset protection and tax laws of the PFTC jurisdiction, if properly structured. Alternatively, most regulated PFTC jurisdictions have reciprocity with other jurisdictions, thus possibly allowing the trust administration by the PFTC to be done in the family’s resident jurisdiction. This reciprocity usually only applies if the PFTC is regulated. However, taking advantage of such reciprocity will generally preclude the PFTC from taking advantage of the favorable trust, asset protection and tax laws of the PFTC jurisdiction, because the trust needs to be properly administered in the PFTC jurisdiction to accomplish this goal.

Formalities

It’s extremely important to exercise the proper formalities with regulated PFTCs regarding the PFTC’s ongoing operation. Generally, the key formalities include: (1) shareholder, board and committee meetings and minutes; (2) creation of and compliance with a policy and procedures manual; (3) annual trust account reviews; (4) trust investment policy statement reviews; (5) proper decision making and documentation regarding trust distributions and investments; and (6) PFTC jurisdiction’s DOB audits.

As a result of the PFTC being owned by the family and named as trustee for the family trusts, the family must take caution with the operation to avoid estate tax problems. While the Internal Revenue Service will no longer issue private letter rulings regarding the estate tax consequences of a family-owned PFTC, it has offered some guidance by issuing IRS Revenue Notice 2008-63 and determined that if structured and operated properly, a PFTC wouldn’t result in any negative estate tax consequences. Although not binding, prior PLRs provide some additional guidance.17

PFTC Advantages

The modern statutory landscape in many of the favorable PFTC jurisdictions has streamlined the formation and operation of the PFTC, providing a powerful trust planning option for families, while at the same time accommodating their key desires. Some of the key reasons that families establish PFTCs are:18

1. Exemption from SEC registration (regulated PFTCs only):

• SEC defers to the jurisdiction’s DOB to audit the PFTC

• Added family privacy; otherwise, SEC registration is public

• Ability to establish SEC-exempt business trusts and common trust funds

• An alternative to SEC registered collective investment vehicles/partnerships, subject to the 99 investors rule

2. Liability protection:

• Family acts as trustee with an LLC/PFTC entity owned by the family with directors and officers (D&O) liability and errors and omissions (E&O) insurance protection, versus family members serving individually as trustees with personal liability and without insurance

3. Provision for a resolution of successor trustee issues

4. Improvement in family governance with LLC/PFTC structure

5. Increased privacy regarding all trust related matters (whether regulated or unregulated)

6. More efficiency as families work with their own family office and outside product providers (that is, investment, insurance or custody) of their choice

7. Better informed and documented trust distribution and investment decisions

8. Increased ability to promote family values, emphasizing both fiscal and social responsibility within the family

9. Convenience and accessibility to the family

10. Efficiency: controls overhead and provides economies of scale

11. Enhanced ability to properly administer and operate illiquid family assets in the trust (that is, LLCs, family limited partnerships, real estate, oil and gas):

• Including assets with possible environmental issues

• Hotels with gambling interests (difficult for corporate or family trustee to register as gambling agent)

12. Allowance for holding large concentrations of either public or private stock without diversification

13. Flexibility with broad sophisticated asset allocations, such as the Yale and Harvard endowments that many families desire

14. Planning opportunities for fully deducting investment management fees19

15. If properly established and operated, the PFTC won’t be subject to estate tax inclusion20

16. If the PFTC is formed in a jurisdiction with favorable lending statutes and is regulated, then the PFTC will have all the powers of a money lending company depending on the jurisdiction’s statutes.

Alternatives to the PFTC

As discussed, the main purpose of PFTCs is to serve as trustee of a family’s trusts.21 Some families without PFTC structures use directed trusts to act similarly to PFTCs, with both investment and distribution committees comprised of family members and family advisors. Like PFTCs, directed trusts generally trifurcate the traditional corporate administrative trustee function: there’s a directed administrative corporate trustee in the directed trust situs providing the required trust administrative functions; this administrative corporate trustee takes direction from an investment and/or distribution committee usually comprised of family members and family advisors in the family’s resident jurisdiction. As with the PFTC, many families prefer directed trusts because they typically have confidence in their own family and family advisors to make proper decisions as fiduciaries for both the trust investments and distributions. Additionally, families can obtain the guidance and oversight of the directed administrative corporate trustee.

Another modern trust structure that operates to supplement a directed trust and as an alternative to the PFTC is an unregulated SPE/TPC. Generally, they’re LLCs and must be used in combination with the directed trust structure with a qualified directed administrative trustee. SPEs/TPCs are used for many of the key reasons PFTCs are used, such as governance, trustee succession issues and liability protection. As previously mentioned, it’s very difficult, if not impossible, to acquire individual liability insurance coverage for investment and distribution committee members and/or trust protectors of a directed trust or any personal trustees for that matter. However, some insurance companies will provide D&O and E&O coverage to an entity established specifically for these purposes, thus protecting the trust protector and the investment and distribution committee members.

As with a PFTC, an SPE/TPC, as a result of its corporate existence, will have the ability to continue without regard to any single individual fiduciary’s death, disability or resignation. The entity typically has bylaws allowing for additional members to be added or removed so that the entity can continue with the trust. These entities also have to be properly structured so as to avoid estate tax inclusion issues. Very few jurisdictions provide for the use of these entities: Delaware, Nevada, New Hampshire, South Dakota and Wyoming are the most popular jurisdictions. These entities aren’t PFTCs, although they provide some PFTC benefits. They have very limited defined duties. One SPE/TPC can generally serve for all of a family’s trusts, so that a separate entity isn’t needed for each family trust. SPEs/TPCs can’t generally hold themselves out to the public as PFTCs or serve more than one family. The SPE/TPC typically has quarterly board of manager meetings to make investment, distribution and other decisions for the family trusts. The operating agreements may indicate that the board of managers meetings will take place in a jurisdiction other than the family’s resident jurisdiction, for example, Florida, along with a vacation. Consequently, the combination of the directed trust and SPE/TPC provides a very cost-effective alternative to the PFTC for families, while also providing an answer to many of their key desires regarding their trust planning. For a comparative analysis and review of the PFTC and its powerful alternatives, see our chart at http://www.wealthmanagement.com/sites/wealthmanagement.com/files/king-table-final.pdf.

Endnotes

1. Al W. King III, “Selecting Modern Trust Structures and Administration Based Upon a Family’s Assets”, IPI Advisors Roundtable (Oct. 21, 2015).

2. G. William Domhoff, “Wealth, Income, and Power,” www2.ucsc.edu/whorulesamerica/power/wealth.html. Note that 40 percent of the top 10 percent of U.S. households are using trusts. This statistic is up from 12.5 percent in 1995. See also “Planning Opportunities Using Domestic Trust Jurisdictions,” Estate Planning Council of Westchester (Dec. 2, 2015). See also E.N. Wolff, The Asset Price Meltdown and the Wealth of the Middle Class (2012).

3. Al W. King III, “Modern Trusts Ease The Worries Of The Wealthy,” (June 16, 2015) http://insurancenewsnet.com/conference-post/modern-trusts-ease-the-worries-of-the-wealthy (an estimated 70 percent of wealthy families don’t use corporate trustees).

4. In addition to limited liability companies (LLCs), some families will structure their private family trust companies (PFTCs) as C corporations or as S corporations.

5. President Obama signed the Dodd-Frank Wall Street Reform and Consumer Protection Act (the Act) on July 21, 2010; See Securities and Exchange Commission (SEC) Rule 202(a)(11)(G)-1 (defines the “family office” exemption under the Act. Note that regardless of whether a family office falls under the definition, a PFTC will usually be deemed exempt from SEC registration).

6. For example, the capital requirements for a PFTC in the following states are: Nevada $300,000; New Hampshire $250,000; South Dakota $200,000; Texas $1 million (with discretion to lower to $250,000); and Wyoming $500,000.

7. See Nev. Rev. Stat Section 669A, N.H. Rev. Stat. Section 392-8 et seq., S.D. Codified Laws Section 51-6A64, Tex. Fin. Code Section 182.011, Wyo. Stat. Ann. 13-5.101 et seq. Generally, Nevada and Wyoming are the two most popular unregulated PFTC jurisdictions, and New Hampshire and South Dakota are the two most popular regulated PFTC jurisdictions.

8. See Tenn. Code Ann. Section 45-2-2001, Florida Stat. Ann. Section 662. On Dec. 9, 2015, the Ohio House of Representatives passed House Bill 229, by a vote of 84-8, enacting the Ohio Family Trust Company Act; the Ohio Senate is considering a companion bill.

9. Most jurisdictions are accredited by the Conference of State Bank Supervisors (CSBS). The CSBS’ mission is to assure that each jurisdiction’s banking authority meets a performance accreditation program to enhance their professionalism and their personnel, which in turn results in safe, sound and well regulated financial institutions. Of the key PFTC jurisdictions, Florida, Ohio, South Dakota, Tennessee and Wyoming are accredited, and New Hampshire and Nevada aren’t accredited; only four of the 50 states aren’t accredited. This accreditation may be crucial if a family is seeking to qualify from SEC exemption via a regulated PFTC.

10. Daniel G. Worthington and Mark Merric, “Which Situs is Best in 2016?” Trusts & Estates (January 2016), at p. 61.

11. See ibid. Many wealthy families generally prefer to locate a PFTC in a jurisdiction with a rule of perpetuities statute that follows Murphy v. Commissioner, 71 T.C. 671 (1979), in which the Internal Revenue Service acquiesced. Following the Murphy approach is crucial for both the dynasty purpose trust without beneficiaries owning the PFTC, as well as the various family dynasty trusts with family beneficiaries and the PFTC as trustee. Many jurisdictions don’t follow the Murphy approach, and this may present a significant risk for the perpetual PFTC.

12. Weak economic conditions of a PFTC jurisdiction could affect future tax policy of that jurisdiction.

13. Al W. King III, “Trusts Without Beneficiaries—What’s the Purpose?” Trusts & Estates (February 2015), at p. 11.

14. For example, New Hampshire requires a minimum of three directors, Nevada is silent, South Dakota requires a minimum of three and a maximum of 12 directors and Wyoming requires a minimum of five directors.

15. Families tend to have one resident director because without one, it’s dangerous for potential piercing of corporate veil claims. New Hampshire requires none, Nevada requires one resident officer, South Dakota requires one resident director and Wyoming is silent.

16. It’s generally best to have an office in a PFTC jurisdiction, particularly with a regulated PFTC. Generally, a qualified corporate agent can provide an office. Typically, the PFTC won’t receive regulated charter without an office.

17. See Private Letter Ruling 200546055 (Aug. 2, 2005), PLR 200548035 (Aug. 2, 2005) and PLR 200523003 (March 8, 2005).

18. Al W. King III, “Unique Modern Trust Structures for Family Offices,” IPI Advisors Roundtable, San Francisco (September 2014); See also Al W. King III, Pierce McDowell III and Matthew Tobin, “Private Family Trust Companies, and Other Modern Trust Structures,” Family Office Exchange Member Event, New York (September 2012).

19. See Treasury Regulations Section 1.167-4(d), requiring that investment fees be separated out from the overall trustee fee and subject to the 2 percent adjusted gross income limitation (final regulations issued May 9, 2014, previously IRS Notice 2008-32, which was issued after Knight v. Comm’r, 552 U.S. 181 (2008)). Potential planning opportunities may exist to deduct the investment fees, for example, the combination of a C corporation and investment partnership that works great with a PFTC.

20. IRS Revenue Notice 2008-63; 2008-31 IRB (Aug. 4, 2008). Addresses income, gift, estate and generation-skipping transfer tax consequences in situations in which family members create PFTCs to serve as trustee of family member trusts of which the family members are grantors or beneficiaries. The IRS ruled that there were no negative tax consequences, if properly structured. See also PLR 200546055 (Aug. 2, 2005), PLR 200548035 (Aug. 2, 2005), PLR 200523003 (March 8, 2005).

21. See supra note 1. See also Al W. King III, “Tips From the Pros: Drafting Modern Trusts,” Trusts & Estates (December 2015), at p. 12.