The estate-planning process is difficult for many of our clients. Clients usually have a lot at stake financially and emotionally when they engage an estate planner. The fact that others often have an intense interest in the outcome of estate planning doesn’t make planning any easier for the client or, for that matter, the estate planner.

Further complicating matters is that there’s usually a wide gap between the knowledge of estate planning that the estate planner possesses compared to that of the client. This disparity adds to the client’s perplexity because it can create feelings of helplessness and dependence.

What does this wide gap in knowledge mean? The estate planner is in a unique position of confidence, looked to as “one who knows.”1 There are legal and psychological burdens that come with this position. What makes this even more difficult is that the client often cedes the power over the process to the estate planner. How many times have your clients asked you, “What do you think I should do?” Estate planners risk fashioning themselves as rescuers, the client’s knight in shining armor. There’s also a seductive opportunity for the estate planner to take on a role as omniscient and omnipotent, which is a grave error that many estate planners make.

Proper Role

Consider the following question: What’s the estate planner’s role in the estate-planning process? To do exactly what the clients say that they want? To educate clients? To be a zealous advocate for the clients? To be the messenger of mortality? To assist clients in transmitting their property with the lowest possible tax consequences? To help clients put together a legally binding estate plan that can withstand attack by disgruntled third parties?

It’s probably some or all of the above. Surely, the estate planner should refrain from being just a pawn of the client. However, the estate planner who focuses on the transfer of property with minimum tax consequences is abdicating part of his counseling responsibility to his client. There’s a big difference between being an estate planner in the truest sense of the term and an estate or tax technician. Despite the misgivings of the late trusts and estates attorney Joseph Trachtman of Hughes, Hubbard & Reed in New York and Professor Thomas Shaffer of Notre Dame Law School in Indiana about the term “estate planner” (instead of the term “lawyer”),2 being an estate planner is a far nobler calling than “estate technician,” as the term now applies to non-lawyers as well.

Good Estate-Planning Result

Every estate planner and client should be in pursuit of a good estate-planning result, whatever that is for that particular client. What’s a good estate-planning result? While estate planners certainly can quibble with the answer to this question, it’s been shown that good results don’t happen nearly as often as they should.3 Probate and trust litigation is on the rise, as people discover that Mark Twain was correct: You never really know someone until you share an inheritance with them. Elder financial abuse also is sharply up, which inevitably leads to undue influence claims. Why? And, what can we estate planners do about it? We can do a lot if we placed more emphasis on our counseling function.

I define a “good estate-planning result” as one in which property is properly transmitted as desired, and family relations among the survivors aren’t harmed during the estate-planning and administration process.

Notice that conspicuously absent from this definition is any mention of taxes. Taxes have always been the easiest piece of the estate-planning puzzle, yet the overwhelming majority of estate planners still focus their attention almost solely on the tax piece, probably because it’s easiest to solve and easiest to demonstrate quantifiable, tangible results.4 This misfocus has contributed to several problems for planners and clients alike.

Over focus on taxes has resulted in the commoditization of estate-planning services, as estate planners joust over who’s developed or who uses the best tax planning mousetrap, which has led to a sharp increase in do-it-yourself one-size-fits-all estate planning. For the myopic tax crowd, the jig is up, courtesy of Congress, which has essentially repealed federal transfer taxes for all but a few thousand people.

The Path

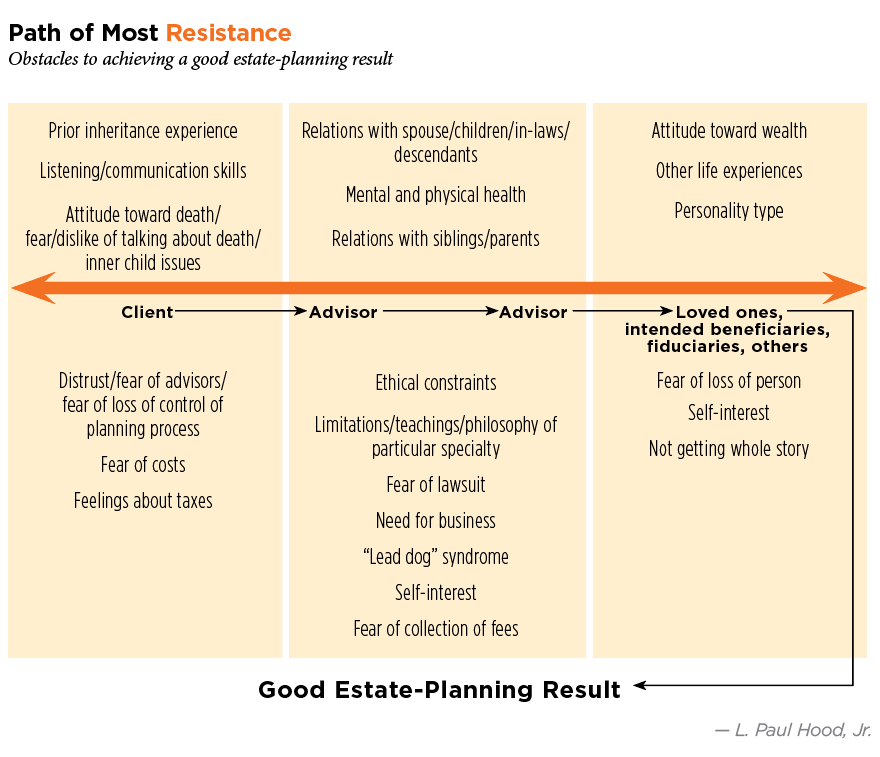

The model, entitled the “Path of Most Resistance” (the Path), p. 54, represents an attempt, feeble and amateurish as it may be, to depict why a good estate-planning result is so hard to achieve by focusing attention on the obstacles in its path. I began tinkering with creating such an explanatory model back in the mid-to-late 1990s, and it’s evolved a bit over time. However, its basic structure has remained intact since its inception.

As the Path illustrates, there are several players in the estate-planning play. I realize that most clients have more than two estate-planning professionals or advisors assisting them, but the larger point is that having more than one advisor itself creates potential obstacles in the path toward a good estate-planning result. Space and complexity of illustration caused me to use two advisors as a surrogate for the reality that the client may have three or more advisors who are attempting to render services to the client and the client’s family. The same is true for the last category of receivers and others, when one is used as a placeholder for as many as the client has to consider. I purposely chose to use only one client even though spouses often do joint estate planning because each individual must separately negotiate the obstacles in the path of a good estate-planning result.5

Fiduciaries and trust protectors are included in either the intended beneficiaries or advisor categories. In this era of increasing slicing and dicing of fiduciary duties in vehicles like directed trusts, the role of fiduciary and trust protector can be vastly different from situation to situation.

In the Path, the items above the orange arrow represent views and common experiences in the past with life and estate matters among all of the players. The items below the orange arrow are witnessed in each of the respective players in the estate-planning play. The Path is intended to illustrate that many things must happen for a good estate-planning result to occur. That is, there are lots of moving parts and opportunities for the process to go awry. The Path also illustrates that the planning process can go backwards too if the wrong events occur at the wrong time.

Behind the Scenes

Some past experiences are common to all of the players in the estate-planning play. These are set out above the orange line.

Prior inheritance experience. Past personal experience as an inheritor, fiduciary or beneficiary can go a long way toward informing one’s views on wills, trusts, probate and estate-planning advisors. This past experience applies to estate planners too. People who’ve survived a contested trust and estate matter often are more guarded, even jaded a bit, by the experience. People who have no experience with trusts and estates matters are frightened of them, often because of horror stories that they’ve heard from others. Nevertheless, this past experience impacts how people think.

Tip: Pre-death intergenerational communication can go a long way to reducing rancor in trust and estate administration in large part by properly setting the expectations of the receivers. Once the client has died, the purposeful estate plan will be administered with complete transparency and frequent communication to minimize things going off the rails.

Listening/communication skills. Most people think that they’re better listeners than they are.6 Some people are more verbal than others, while others are more visual. Because a significant part of communication is body language,7 it’s very important to watch the other conversant’s body language.8 We all have different styles and levels of skill in both listening and communication.9 It behooves an estate planner to be familiar with listening and communication styles so that he can better serve his clients and work collaboratively with other estate planners.

Tip: The purposeful estate planner should maintain solid eye contact with the clients during the interview, particularly during times of tension or points when there’s some uncertainty, angst or disagreement.

Attitude toward death/fear or dislike of talking about death. Human beings are unique in being able to think about death, but most people would rather not think about it—their own or that of anyone else. Some people simply can’t consciously contemplate their own demise, which can be an obstacle in estate planning. Again, estate planners aren’t immune to this; most estate planners are just as reluctant to discuss a client’s future death as the client himself because this discussion reminds the estate planner of his own mortality.10

Tip: Consider taking the lead on being vulnerable and discussing death openly and honestly. It’s okay not to like talking about death and be fearful of it, but fears faced out in the light tend to dissolve or be significantly reduced.

Inner child issues. Many people can trace or at least attribute a problem to something in their childhood. Author John Bradshaw11 has written extensively about how childhood wounds manifest themselves as we age. It’s important for estate planners to understand that some adult actions, particularly actions that seem negative or over reactionary, may have their genesis in childhood, particularly in working with family businesses.

Tip: Practice mindfulness and being more self-aware of your feelings and past. If an interaction or exchange with a client or another player brings up feelings within you, first label those feelings and then attempt to find their source.

Relations with spouses/children/in-laws/descendants. When I happily reported the birth of my first child to one of my mentors in estate planning, the late Gerry LeVan, he told me that he was halfway toward becoming a good estate planner, but that he wouldn’t become a good estate planner until his first grandchild was born. Gerry was right. Indeed, after the birth of my first child, I began looking at documents that I was drafting differently and shifted many of my default provisions quite a bit, just because of the birth. My son’s birth made me a better estate planner because I could now more readily empathize with parents. Some people have precarious relationships with family members, and divorce often creates more acrimony as the former spouses often force their loved ones to take sides.

Tip: Again, self-awareness of your own feelings and past experiences can go a long way toward identifying and dealing with feelings.

Mental and physical health. It’s undeniable that the health—mental and physical—of everyone in the estate-planning play impacts the estate-planning process. People who’ve had brushes with death often are far more appreciative of each day of life than those who’ve been healthy for their entire lives. Mental health issues often lurk in the shadows of codependency and enabling, when some family members look after other family members, often to the detriment of both, and apologize and cover for the sick family member. This is particularly rampant when a family member suffers from drug and alcohol addiction.

Tip: We’re all different and have different past experiences. Status of our physical and mental health significantly impacts our bandwidth and outlook on life. Age factors in here as well. Be aware of your feelings about physical and mental health, which often are informed by your past experiences.

Relations with siblings/parents. Clearly, one’s relationships with one’s own siblings and parents, whether living or dead, have an effect on how one views relations of others with their siblings and parents. Contrast the “one big happy family,” whose members truly love and respect each other, both the good and the bad, with the dysfunctional family whose communications have broken down, and the members have taken sides and gone into battle station mode.

Tip: Be aware of these relationships and how they’ve informed your views on estate planning for your clients.

Attitude toward wealth. Some people inherit significant wealth or are raised in affluent homes, while others grow up under less fortunate circumstances. These experiences often affect attitudes about wealth. Some are jealous, while others are oblivious to what other people’s experiences are regarding wealth. Some people understand the value of hard work and savings, while others feel entitled to wealth. Inheritors may not view their wealth as their own because they didn’t create it. Contrast that with the individual who created the wealth, whose very persona often is inextricably intertwined with that wealth.12

Tip: It’s important to figure out how the family came into their wealth because that will give clues as to how the wealth is perceived and how it will be administered and passed on, especially if the wealth wasn’t created in your client’s generation.

Other life experiences. This catch-all category can include bankruptcy, termination of employment, being a defendant in a lawsuit, jail, tax problems and divorce. The purposeful estate planner won’t forget that these potentialities may be present and impact the client’s decisions.

Tip: Your initial client questionnaire must ask some broad general life experiences questions, because, for example, the client who’s gone through a nasty divorce or a bankruptcy may be far more guarded than the client who hasn’t had these experiences.

Personality type. While everyone is unique in some respects, there are recognized personality patterns.13 Some personality types blend well with others, while other types don’t.

Tip: Make yourself familiar with personality types, because this knowledge will prove invaluable in getting through to clients of all types. Again, self-awareness is the key.

The Client

Clearly, the star of our play is the client. As stated earlier, some clients have significant experience with estate planning, but for many, this trek is a maiden voyage.

Distrust/fear of advisors/fear of loss of control of planning process. Clients often are novices in dealing with advisors, although some may have significant experience. Fear of loss of control of the estate-planning process keeps many more from tending to their planning than most estate planners realize.

Tip: The key is humility on your part and the willingness to let the client be in control of the process. I realize that this tact flies in the face of some sales training that teaches how to gain control and eliminate objections. However, the purposeful estate planner will insist that the client be in full control of the estate-planning process, with the estate planner acting as guide and counselor.

Fear of costs. Given that many estate-planning clients possess little experience in dealing with advisors, it isn’t unusual to see people put off their estate planning simply out of fear of the cost.

Tip: Don’t live and die by the time sheet, which was a terrible development because it attempted to quantify value through increments of time. The problem is that value and time aren’t co-linear. A planner can render splendid advice in minutes that saves a client millions of dollars. On the other hand, spending five hours at your hourly rate on a routine will drafting assignment isn’t going to make a client very happy unless the bill is significantly adjusted downward. Talk about fees up front and periodically. Put things in writing. Use flat fee arrangements when appropriate.

Feelings about taxes. While the federal estate tax under current law applies to a very few, although a number of states still have a significant estate tax, feelings about estate taxes often occupy a client’s mind. Some people are hell bent on paying no estate tax, while others recognize that they won’t personally ever have to pay their own estate taxes.

Tip: Most estate planners are pretty quick to point out that typically, no federal estate tax will be due (no doubt in some substantial part to their excellent work), so nothing further need be said here.

The Advisor

As stated earlier, the Path depicts two advisors but isn’t intended to imply that a client may not have more than two. The more advisors, the greater the risk of more problems because when more people are involved, they bring more personal experiences and baggage into the situation.

Don’t misinterpret what I’m saying here: The client should have as many advisors as he feels is necessary or appropriate. I’m a big believer in referrals and collaboration simply because it was my experience that clients get better service and a better estate plan. However, having more advisors creates a situation that must be watched and managed. I’ve seen estate-planning engagements fall apart because the advisors were incapable of cooperating and collaborating, which is a bad result for the client and can add to the negative experiences that the client will take to the next advisor, if any.

Ethical constraints. Each of the estate-planning subspecialties have their own ethical rules and conventions. These ethics rules impact subspecialties differently. The legal ethics rules insert some additional complexities in the estate-planning process, particularly in the areas of confidentiality and conflicts of interest. It’s imperative that the planner’s engagement letter permits complete and total access to all of a client’s advisors.

Tip: Make sure that the engagement letter casts a wide net over the people with whom you may communicate to allow you to communicate with those third parties. That list could include children or other descendants, family business employees, lawyers, CPAs, investment advisors, fiduciaries (trustees, etc.), financial planners, life insurance agents, wealth psychologists and, in some cases, access to the client’s treating physician.

Limitations/teachings/philosophy of particular subspecialty. Each estate-planning subspecialty brings its own mindset and philosophy into an estate-planning engagement. This often is clearly reflected in the factfinders of a particular subspecialty, which tend to focus more attention on the areas covered by that particular subspecialty. For example, lawyer factfinders tend to focus attention on property, while life insurance factfinders might focus attention on life insurance. Moreover, different advisors in the same subspecialty may have vastly different philosophies about estate planning. It’s critical that advisors check their egos and biases at the door before getting down to work with an open mind and collaboratively on a client’s situation.

Tip: Try true collaboration just once. If it goes right, you’ll never want to work any other way again. With collaboration comes diversity of professional backgrounds, educational and experiential pedigrees; different manners of training; and significant knowledge about a certain aspect of the client’s estate plan. This diverse strength of the group exceeds the strength of the sum of its individual members. This excess is called synergy.

Fear of lawsuit. Every professional advisor lives in some fear of being sued by a client. Estate-planning advisors practice defensively to minimize the risk of lawsuits. Some of these defensive actions negatively impact the relationship with a client, particularly when the client doesn’t appreciate the risk of a course of action that the advisor recommends.

Tip: Again, one thing that most estate planners do well is practice defensively. I can only repeat nationally recognized estate-planning attorney Howard Zaritsky’s sage and timeless advice to simply be nice.14 To everyone. Lawyers are notorious for not being nice.

Need for business. Many advisors constantly search for new business. In a way, this is the flipside of the fear of lawsuit discussed above. Some estate planners are better at giving safe “yes” answers to clients, who always want to hear “yes” and loathe hearing “no.” Unfortunately, some estate planners spend an inordinate amount of time telling clients “no” when there’s a safe “yes” answer that simply requires fresh thinking.

Tip: The safe strategy is to view potential clients cautiously in that they could be either an opportunity or a curse. Some clients are more trustworthy than others; some clients are more aggressive than others. Sometimes, estate planners who are worried about their level of business will take in just about any client, when a more selective policy makes far more sense.

“Lead dog” syndrome. Some advisors, particularly those with some product to sell, are trained to gain control of a situation. This behavior often conflicts with other advisors, especially those who also desire to be in charge of the client’s estate planning. When advisors joust for the desired position of quarterback on the estate-planning team, it can delay or even end the planning.

Tip: Be a good example to those with whom you’re supposed to be collaborating by keeping your ego in check and inviting them to do the same.

Self-interest. Let’s face it, advisors are in business for themselves and have families to feed or employees to pay. Even though just about every subspecialty of estate planning has ethical responsibilities to clients, it would be foolhardy to expect advisors not to act in their own self-interest at some point in an engagement.

Tip: Put the interests of your client first.

Fear of collection of fees. This fear differs greatly from subspecialty to subspecialty. When an advisor commences an engagement without having first secured payment for services, this fear can impact how much work the advisor will do before being assured of being compensated, which can impact the venture toward the good estate-planning result.

Tip: It’s perfectly acceptable to require a client who’s asking for a lot of work to be done to put up a retainer in good faith to cover the work.

Loved Ones/Intended Beneficiaries

This category includes those who believe that they’ll receive something from the client at death.

Fear of loss of person. Most people who have a potential interest in a client’s estate have a relationship with the client. Quite often, these people fear the client’s death as much or even more so than the client or the client’s advisors. In fact, I’ve witnessed this fear be so palpable that, when expressed, it ended the client’s estate planning because the mere notion of the client’s death was too great to bear for the family member. The family member’s horror at the mere notion of the client’s death was triggered by the family member’s fear of loss of the client. The family member acted out much like an infant whose parent leaves his side.

Tip: Address fears and feelings head on with transparency. Intergenerational communication is important in the quest for a good estate-planning result.

Self-interest. As with the advisors, we should expect people in this category to act or argue out of self-interest. There’s nothing inherently wrong with looking out for one’s best interests until it crosses the line and becomes either undue influence or even outright misappropriation.

Tip: Many lay fiduciaries make big mistakes by failing to see the difference between owning property outright and holding the legal title to that property in trust and as trustee for the benefit of someone else. This is when the estate planner must clearly and, if need be, forcefully, inform the client that being a fiduciary is a potential source of great liability.

Not getting the whole story. I’ve found that intergenerational estate planning is best when the client communicated the estate plan and the reasons for it to the potential receivers during the client’s lifetime. Nevertheless, it was far more common for clients to keep quiet about their estate plans during lifetime, despite my advice to the contrary. Some of the saddest and most unfortunate situations I’ve ever witnessed was when a deceased parent left a smaller amount to a child than what the parent gave to the child’s siblings without explaining why this was done.

Quite often, this unfortunate and inadvisable practice leads to post-death administration difficulties as relationships among the survivors are torn asunder, including litigation. However, the larger problem is the psychological damage that it does to the child, who’s left to wonder for the rest of his life whether his parent loved him as much as the parent loved the siblings, because many people believe that the relative bequest level is the ultimate final barometer of love, even though this isn’t true in the vast majority of cases.

Tip: It’s been said before, but it bears repeating: Intergenerational estate planning is best.

Note that this is the first installment of a three-part article about the human side of estate planning. In the second installment, I’ll introduce three psychological phenomena that shroud every day estate planning. In the third, I’ll explore mortality salience (reminders about death), other fears that clients experience in estate planning, concluding with an introduction of two tools that might assist estate planners with their clients: motivational interviewing and appreciative inquiry.

Endnotes

1. Louis H. Hamel, Jr. and Timothy J. Davis, “Transference and Countertransference in the Lawyer-Client Relationship: Psychoanalysis Applied in Estate Planning,” 25 Psychoanalytic Psychology, at pp. 590-601 (2008).

2. Thomas L. Shaffer, Death, Property, and Lawyers (Dunellen Press 1970), at pp. 1-2.

3. In a study conducted by Roy Williams and Vic Preisser, of 3,250 wealthy families, research indicated a mere 30 percent success rate in keeping wealth in a family, which equated to global research finding the same percentage of success. See Roy Williams and Vic Preisser, Preparing Heirs: Five Steps to a Successful Transition of Family Wealth and Values (Robert D. Reed Publishers 2003).

4. Akin to a Jenny Craig before and after picture/testimonial, most estate planners proudly crow over how much tax their brilliant planning has saved and bill accordingly.

5. This perhaps sidesteps the inherent ethical issues attendant to representing a couple jointly. In the “Path of Most Resistance,” p. 54, spouses are each considered separate clients. This should by no means be considered an endorsement of the legal ethics decision to represent a couple as separate clients, because I’m uncertain that this tact may be safely done by a lawyer.

6. See, e.g., Michael P. Nichols, The Lost Art of Listening (The Guildford Press 2009).

7. Dr. Albert Mehrabian, author of Silent Messages, conducted several studies on nonverbal communication. He found that 7 percent of any message is conveyed through words, 38 percent through certain vocal elements and

55 percent through nonverbal elements (facial expressions, gestures, posture, etc).

8. See generally Jo-Ellan Dimitrius and Mark Mazzarella, Reading People (Random House 1998).

9. See generally Benedict Carey, How We Learn (Random House 2014).

10. Shaffer, supra note 2, at pp. 115 and 118.

11. John Bradshaw, Homecoming: Reclaiming and Championing Your Inner Child (Bantam 1990).

12. Jean Paul Sartre, Being and Nothingness (1943): “The totality of my possessions reflects the totality of my being. I am what I have. What is mine is myself.”

13. See, e.g., Isabel Briggs Myers and Peter B. Myers, Gifts Differing: Understanding Personality Types (Davies-Black 1995) and David Keirsey and Marilyn Bates, Please Understand Me: Character & Temperament Types (Prometheus Nemesis Book Company 1984).

14. Howard Zaritsky, “Eight Basic Rules of Practical Practice,” set forth in The Tools & Techniques of Estate Planning 18th Ed. (National Underwriter 2017), at p. 118.