By Dean Curnutt

(Bloomberg Prophets) --Diversification is at the heart of prudent risk management. Since no two securities move perfectly in tandem, an investor can mitigate volatility by gaining exposure to a variety of securities and asset classes. Today’s markets, characterized by pricey assets and extremely low volatility, provide little margin for error and require investors to think carefully about not just security selection but also about how portfolio components interact with one another.

Recent history shows that misplaced correlation assumptions can lead to a far more benign assessment of risk than the one that ultimately materializes. The stakes are high. Almost every traditional metric points to a stock market that is on the expensive side. Valuations are even less appealing in the sovereign-bond universe, as Treasury 10-year yields barely outstrip inflation. Warren Buffett recently said stocks are “still attractive compared to bonds.” If this is the prevailing logic among enough investors, then equity markets are vulnerable to a sudden sell-off in bond prices just like during the 2013 taper tantrum.

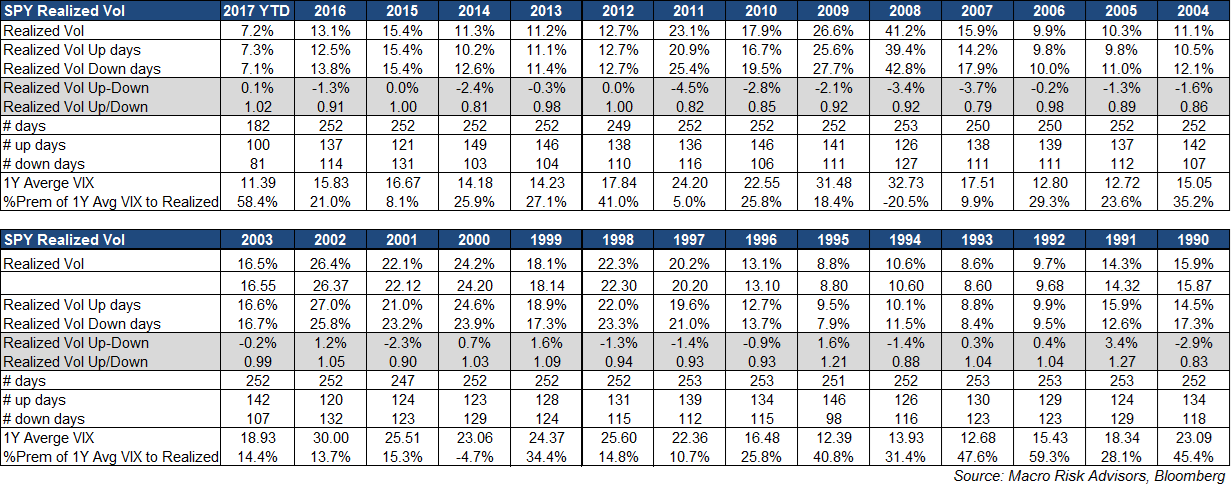

Among the many factors weighing on the VIX index -- including a muted business cycle characterized by low growth and inflation and a market-minded Federal Reserve -- the most basic explanation is the dramatic decline in realized volatility of the S&P 500 Index. The correlation between the VIX and concurrent one-month realized volatility averages a robust 80 percent. The table below tells the story about the breathtaking plunge in realized volatility at the equity index level in 2017.

The bigger question is: Why is realized volatility so low? An important driver is the extremely low level of correlation of daily returns among stocks. Over the past year, the average level of correlation among stocks in the S&P 500 is just 19 percent. During episodes of market turbulence -- when stocks can move in near-lockstep, such as in 2008 and 2011 -- the correlation of returns can surge past 75 percent. But even in normally functioning markets, average stock correlation is around 40 percent.

In isolation, a decline of 20 correlation points (from 40 to 20) trims the realized volatility of the index by about 5 points. The damper that low correlation puts on volatility illustrates the degree to which portfolio risk is tied not just to the volatility of its components, but also to how the individual securities interact.

Just as the VIX is being weighed down by realized volatility, the market pricing of correlation is being suppressed by the substantially low level of realized correlation. By comparing the pricing of an option on the S&P 500 to the average prices for options on the equities that comprise the index, one can derive the “implied correlation” for index options. This measure stands at 23 percent for three-month options, a level not seen in at least 20 years. It is the joint expectation that not only will the equities that make up the S&P 500 exhibit low volatility but also that their returns will have exceedingly low correlation that results in option costs comparable to the pre-crisis period.

Is it prudent to assume that both low stock volatility and low correlation are here to stay? Macroeconomic uncertainty can make stocks more volatile and more highly correlated at the same time. As a result of the 2011 “dual shock” of the European sovereign-debt crisis and the U.S. debt-ceiling showdown, the volatility of Exxon Mobil and Microsoft more than doubled in August from the first seven months of the year. In addition, the correlation of these stocks, averaging 50 percent through July 2011, surged to as high as 88 percent during August.

Because common sources of macro risk -- including the Fed, energy prices, geopolitics, inflation shocks, regulatory change, sovereign risk, elections and fiscal-policy dysfunction -- can affect both single stock volatility and the correlation among stocks at the same time, the benefits of diversification can slip away, leaving portfolios exposed to more volatility than anticipated.

Another correlation assumption that must receive constant attention is the one between stock and bond returns. Even though the S&P 500 is up 11.5 percent this year and the iShares 20+ Year Treasury Bond exchange-traded fund has gained 7.6 percent, their returns are strongly negatively correlated on a daily basis. The combination of two assets that deliver positive returns but have negative correlation is not only very rare, it’s nirvana for a portfolio of stocks and bonds.

A simple portfolio with 50 percent exposure to the S&P 500 and 50 percent to the iShares ETF has delivered an annualized return of 16 percent with just 5 percent volatility in 2017. Even though the Fed has deftly convinced the market that its balance-sheet unwind will be uneventful, we should appreciate the degree to which the joint valuation of stock and bond prices is in uncharted territory and that an undoing of the “risk on/risk off” framework carries significant implications for portfolio risk.

There is an old saying that “There are no bad securities, only bad prices.” The modern-day risk manager might embrace an aphorism that better reflects today’s more complex, asset-intertwined risk dynamics: “There are no bad securities, only bad correlations.” Investors need to carefully examine the assumptions relating to the interaction of assets in their portfolios and understand that correlation relationships can change quickly, especially when markets become more volatile.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Dean Curnutt is the CEO of Macro Risk Advisors, a firm that provides global market risk analysis and execution for institutional investors. He was formerly managing director and head of equity sales-trading at Banc of America Securities.

To contact the author of this story: Dean Curnutt at [email protected] To contact the editor responsible for this story: Robert Burgess at [email protected]

For more columns from Bloomberg View, visit Bloomberg view