(Bloomberg) -- When I started out as a strategist more than 30 years ago, I had the arrogance of youth, a long-term investing horizon and less wealth to worry about. Those three qualities worked well then, but not so much now.

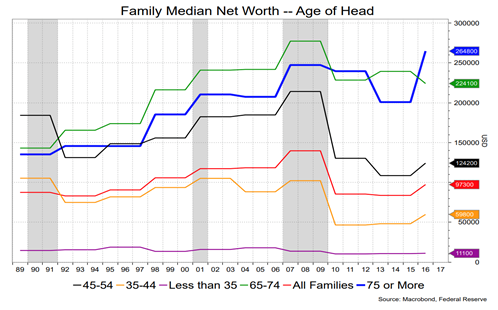

I have the wealth to enable a comfortable retirement—at the moment. What I don’t have is the time left to sleep easily at night in the event the stock market enters a serious bear market. I’m not alone: those aged 55 and older are a larger portion of the population than they’ve ever been. We’re 35 percent of the country and growing. Compare that to 27.4 percent in 2000 and 31 percent in 2008. I'll get back to those years in a bit.

When you consider the recent gyrations in equities in the context of the aging population, logic follows that folks facing or in retirement will be much more defensive in their behavior than in the past. If that means they will be quicker to get out of equities in the next downturn and stay out, their impact will be felt for a long time. That's especially true given where wealth lies. Older people have it but neither the time nor mindset to recover from a bear market no matter how many times they hear their stockbroker utter encouraging words such as, "despite short-term market gyrations, it's important to maintain a long-term perspective, based on your goals and financial plan.”

My camp—the baby boomers—is unlikely to see a surge in interest rates that will provide a comfortable return of, say, 5 percent to 6 percent in long-term, safe municipal debt securities. Total returns in the bond market are going to be modest—forever.

My generation has been here before in an economic sense. Approaching 2000, we all knew the dot-com-fueled Nasdaq Composite Index was blowing up into a bubble, but greed and a belief that we were smarter than everyone else kept us riding the momentum until we wished we hadn’t. But then we were 40 or 45 years old, and arguably had 20 to 25 working years left to make up for the momentary loss. Bothered, yes, but younger and with time on our side.

All went well, especially the value of our homes. We didn’t worry about meek wage gains because our wealth was growing. Plus, if we needed money we could just borrow it—almost no questions asked. We may have looked askance at rising government deficits, but that would be someone else’s problem down the road.

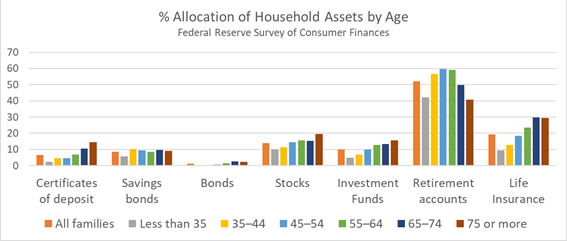

Then came 2008. We were a bit older and dealing with our second—and vastly more serious—crisis in 10 years. That gets you thinking, and explains why the baby boomers joined in late to this bull market. We are approaching 60 at the least and most are well beyond that age. We can’t count on many more years to make up for another stock market rout. The chart below shows that those 55 and older have the highest allocation to stocks, funds and CDs than any other age group. They have the wealth and need to keep it because they don't have the same time horizon as in past bear markets.

Depending on where you live, home values may not have recovered in real terms, wage gains have been lame and maybe you're starting to think about those deficits and worrying if they'll affect Social Security or Medicare entitlements. Heaven forbid you lose your job before 65 and have to obtain medical coverage on your own. We’re still waiting for President Donald Trump to fulfill his election promises: “We're going to have insurance for everybody. We're going to have a healthcare that is far less expensive and far better.”

The bottom line is that the sort of market turmoil we’re experiencing will have a longer-term impact on investor behavior, as well as confidence and consumption habits, than we’ve ever seen. It has to if we’ve learned anything over the course of our working and investing careers. To many people, the standard stockbroker advice over the years to maintain a long-term perspective based on your goals and financial plans sounds downright cautionary today.

David Ader is chief macro strategist at Informa Financial Intelligence. He was the No. 1 ranked U.S. government bond strategist by Institutional Investor magazine for 10 years.

To contact the author of this story: David Ader at [email protected]

For more columns from Bloomberg View, visit bloomberg.com/view