By Sarah Ponczek and Elena Popina

(Bloomberg) --In nature, things are cyclical. If only it were as clear cut in stocks.

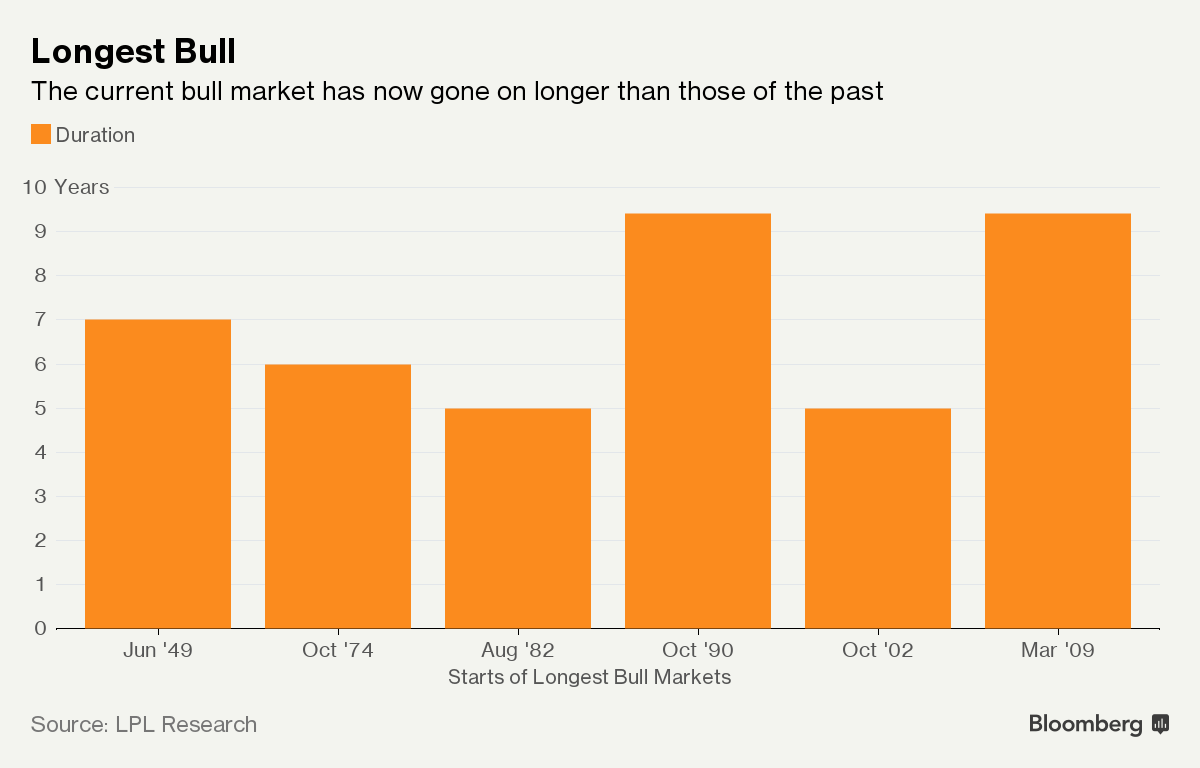

Alive for 3,453 days, the bull market in the S&P 500 today becomes the longest ever recorded by some measures. Through credit crisis and Trump tweet, the rally that began at the pit of the financial crisis has returned almost 20 percent a year for 9 1/2 years. About $23 trillion in value has been created as thousands of bearish predictions fell flat.

The question is everywhere: is it early or late? Does the passage of time incubate excesses that ensure a rally’s demise? Or does older mean stronger and harder to scare?

What follows is a look at frameworks for deciding whether the advance in U.S. stocks is somehow doomed by the calendar. In a bull run fueled by easy money and investors heady with the rush of earnings growth above 20 percent, the state of the patient is by most accounts sound.

“No bull market comes with an expiry date like a time-stamp on a milk bottle or on a crate of eggs,” said John Stoltzfus, the chief investment strategist at Oppenheimer & Co. “Bull markets live and die by both economic and corporate fundamentals.”

Never Forever

First, the bear case, which in large part amounts to the observation that never before has a bull market gone on forever. It’s more than that, skeptics say: the longer stocks go up, the worse grow diseases that will one day claim the run’s life. Valuations soar, standards weaken, skepticism gives way to mindlessness. Years pass and the lessons of old traumas slip away.

“As the expansion expands, people now start to think we may never have a recession, which actually encourages more risk taking and more borrowing,” Srinivas Thiruvadanthai, research director at the Jerome Levy Forecasting Center in Mt. Kisco, New York, said by phone. “It also encourages euphoria, thereby laying the seeds for the demise.”

Check the fundamentals

The message is a broken record that’s been playing all year: the fundamentals are strong. Earnings growth is running at the highest rate in eight years and the U.S. economy just hit 4 percent growth, the fastest since 2014. Yes, macro headwinds such as trade, tariffs, and emerging market currency routs make headlines. But as long as earnings hold up and the underpinnings of the economy remain strong, it’s nuts to bet against stocks.

“A 9-year-plus bull market is undoubtedly old, but we don’t think that means it’s necessarily near an end,” said John Lynch, chief investment strategist at LPL Financial, and Ryan Detrick, the firm’s senior market strategist. “The underlying positives from fiscal policy, government spending, strong corporate earnings, and improving confidence should extend this economic cycle for at least another year, maybe more.”

To Bank of America strategists including Savita Subramanian, the firm’s head of U.S. equity and quantitative strategy, the cycle ins’t over. Rather, the market now resides somewhere between what they classify as mid and late-cycle, as supported by the return of sales growth and a pick-up in capex. The S&P 500 is expected to boost fixed investment spending by 15 percent over the next year, the fastest pace since 2012 according to Bloomberg Intelligence.

Stealth bears

Another reason the record doesn’t spell the end? While the advance since March 2009 might be unbroken by a 20 percent fall, it’s endured too many traumas to be considered one long rally. Although neither drop exceeded 15 percent, the S&P 500 went through two 10 percent corrections around the time of the 2015 yuan devaluation. In May 2015 and February 2016, the Russell 2000 and energy companies in the S&P 500 each suffered retreats of more than 20 percent, respectively.

“We had Japan problems, we had China problems, and we had an earnings recession in 2015,” Brian Belski, BMO chief investment strategist, said on Bloomberg Television. “We’ve forgotten all of this because we just look at the headlines. I’m so tired of this late-cycle talk. Why can’t we just invest?”

Belski also points out the importance of acknowledging that different areas and sectors can suffer corrections at different times. It’s not a uniform market.

“I look at the 11 sectors of the S&P 500 or the Russell, and in those 11 sectors I can see early-cycle, mid-cycle, late-cycle,” he said. “Why are we applying this blanket conclusion to everything? That’s the biggest issue right now with investors. We can’t stop ourselves from trying to diagnose the top.”

Different times

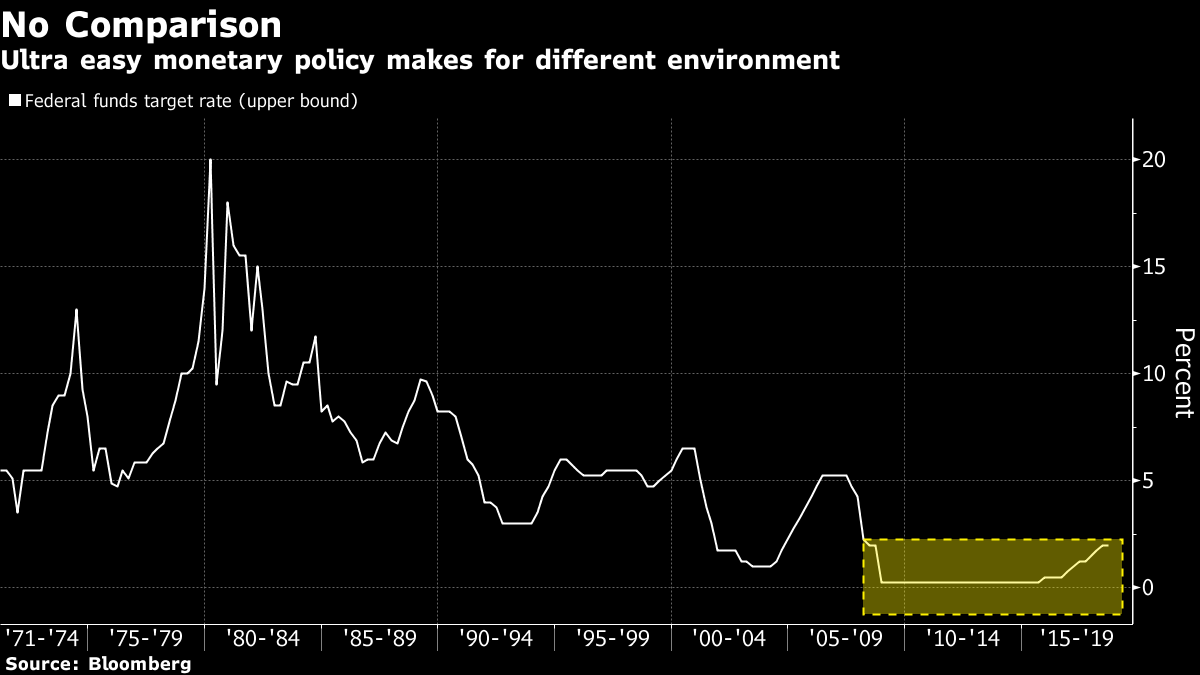

Some say figuring out exactly where we are in the cycle is a moot point, as the bull market of the 21st century is not comparable to those of decades prior. About 10 years of persistently low interest rates and quantitative easing make this time around different from any others of the past.

“Go back 10 years ago, we were in trouble, the world was in trouble, and what saved us ultimately was QE, and that was something the world had never seen,” Paul Richards, president of Medley Global Advisors, told Bloomberg Television. “Every model failed to get this thing right. Now that you look at the length of the cycle, the technicians kick in, technicals have never had to factor in QE.”

What investors should expect is more volatility as the market rolls further along, grappling with positives such as fiscal stimulus and the notion of where we stand in the cycle, according to Richards. Alongside heightened volatility, interests rates are rising, the yield curve is flattening, and signs of inflation are breaking through.

“Are there more challenges to a bull market that’s been in existence for a long time than there would be if we were more early on? The answer is yes,” Ernie Cecilia, chief investment officer at Bryn Mawr Trust Co., said by phone. “The risks rise at later stages of a bull market, but in and of itself, the age of the bull market alone is not a harbinger of recession.”

--With assistance from Jonathan Ferro.To contact the reporters on this story: Sarah Ponczek in New York at [email protected] ;Elena Popina in New York at [email protected] To contact the editors responsible for this story: Jeremy Herron at [email protected] Chris Nagi