The holiday season is upon us, which means all eyes are going to be on the retail sector for the next few weeks. One-fifth of all retail spending in the U.S. happens during the holidays. For some retailers the period between Thanksgiving and Christmas can account for 40% of their yearly revenue. ETFs can be a good, low cost way to get exposure to the retail sector.

Just like Santa, New Constructs keeps track of everything these ETFs are up to, and we’ve made our list and checked it twice. Our predictive rating for ETFs is based on total annual costs and ourstock ratings of their holdings. Our analysts dig through the financial footnotes of over 3,000 Form 10-K’s a year, so we’ve done our due diligence on the holdings of the ETFs we cover.

Let’s see which retail-focused ETFs have been naughty or nice.

Naughty: Direxion Daily Retail Bull 3x Shares (RETL)

RETL is getting a lump of coal in its stocking for holding bad stocks and charging investors high fees. 61% of the stocks held by RETL earn our Neutral-or-worse rating. What’s worse, RETL charges total annual costs of 1.06% to investors, the highest of any of the 184 sector ETFs we cover.

In addition, RETL’s leveraged triple long strategy, which seeks to return 300% of the Russell 1000 Retail index every day, can be risky for investors. If retail sales fall short, RETL can be hit hard, as it was last year when it lost 12% of its value during the month of December. RETL has returned 122% to investors so far this year, but its poor holdings, high fees, and risky strategy give it too much downside potential for the holiday season.

Naughty: Market Vectors Retail ETF (RTH)

RTH, at least, charges low fees to investors, but its holdings are still not up to snuff. Like RETL, 60% of the stocks held by RTH earn our Neutral-or-worse rating. RTH lands itself on the naughty list and earns our Dangerous rating.

Lump Of Coal in RETL and RTH

Amazon (AMZN) is one of my least favorite stocks held by RTH and RETL and earns my Dangerous rating. As I highlighted back in May, the growth expectations implied by AMZN’s stock price are immense. AMZN’s current valuation of ~$388/share implies 25% growth in operating profit (NOPAT) for the next 20 years. The issue for AMZN is its NOPAT margin, which has declined from 7% in 2004 down to 1% last year. Now that AMZN is no longer the only game in online retail, it has to keep prices down to stay competitive, which limits its profit growth potential. AMZN can keep growing revenues all it wants, but without profits it can’t create value for shareholders.

AMZN is the largest of holding of both RTH and RETL. It makes up 9% of RTH’s assets and 15% of RETL’s.

Nice: PowerShares Dynamic Retail (PMR)

PMR makes it onto the nice list with a Neutral rating. 72% of the stocks held by PMR earn a Neutral-or-better rating. Its total annual costs of 0.66% are on the high end for an ETF but not as offensive as many others. Since only three out of the 184 ETFs we cover currently earn an Attractive rating, Neutral is the best investors can hope for in most sectors.

The biggest drawback for PMR is that it only has $39 million in assets. I recommend investors avoid any ETF with less than $100 million to ensure proper liquidity. PMR has nice holdings, but it’s not as good a choice for investors as the other entry on the nice list.

Nice: State Street SPDR S&P Retail ETF (XRT)

The biggest ETF on our list is also the nicest. With $1.4 billion in assets, XRT is more than ten times larger than the other three retail ETFs combined. 61% of its assets are in Neutral-or-better rated stocks, so its portfolio is not quite as strong as PMR. However, XRT’s total annual costs of 0.39% are lower. Our predictive rating gives both ETFs a Neutral rating, and in the end the superior liquidity of XRT gives it the edge.

The TJX Companies (TJX) is one of my favorite stocks owned by XRT and earns my Attractive rating. While many brick and mortar retailers have struggled in recent years, TJX has thrived. The company has grown NOPAT by 12% compounded annually over the past decade. The recentrelaunch of the online store for T.J. Maxx should provide a further boost to revenues.

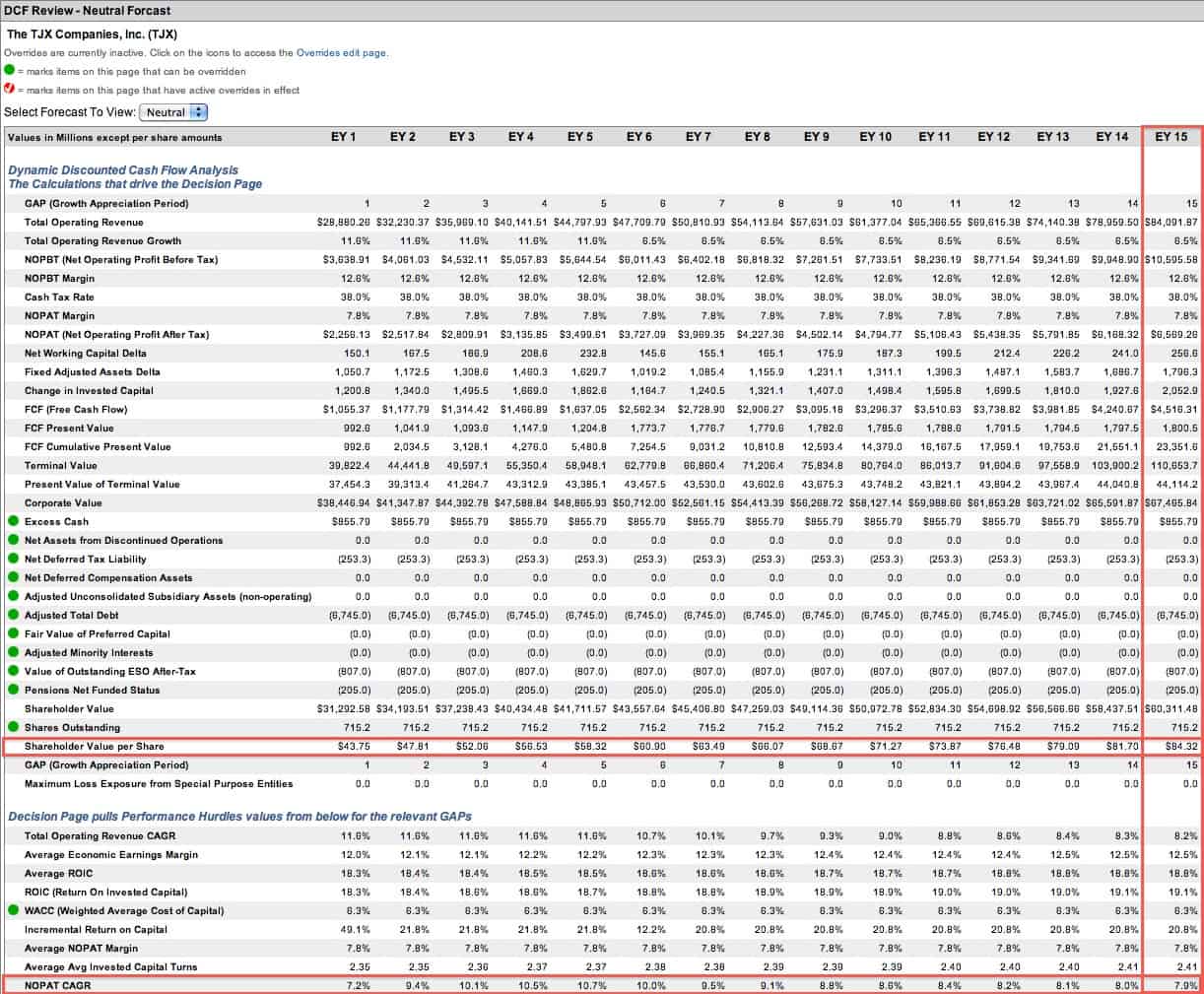

TJX is not as cheap as some of its competitors, but the company’s strong financial results make the stock well worth its valuation. At ~$61/share, the market expects TJX to grow NOPAT by 10% compounded annually for the next six years. Six years is an awfully short growth appreciation period. If we give TJX credit for 15 years of growth at a slightly lower 8% growth rate, the stock is worth $84 today, a 38% premium to its current valuation.

{kind=link}

{kind=link}

The fact that XRT and PMR, our two top rated ETFs, only earn a Neutral rating is slightly disappointing. 20 out of the 124 retail stocks we cover (22% of the market cap) earn an Attractive-or-better rating. One would hope that at least one retail ETF could put together an Attractive portfolio. If you’re set on a retail ETF, XRT is our pick, but investors might be better off buying individual stocks like TJX instead.

More details on the retail sector are in our 4Q13 Best & Worst ETF in the Consumer Discretionary Sector report. You can see all our 4Q13 Best & Worst Sector Fund reports here. Our 4Q13 Sector Ratings are here.

Sam McBride contributed to this article.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.