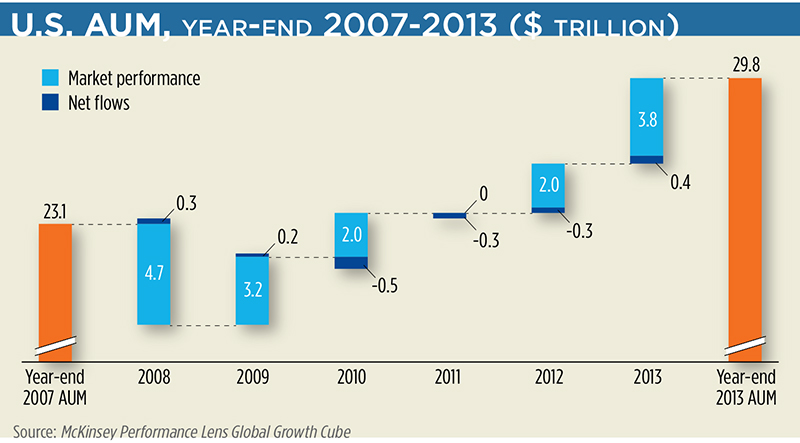

The global asset management industry had a rosy year, with total assets under management up 12 percent in 2013 to a high of $64 trillion, and up 7 percent through mid-2014, according to a new McKinsey report. But in the U.S., net inflows have hovered at 1 percent a year since 2012, down from an average 3 percent net flow rate from 2002 to 2007.

“When the next market correction hits, growth will once again become dependent on net flows, which have been anemic in recent years,” McKinsey said in its report, called “The New Imperatives: Gaining an Edge in North American Asset Management.”

Prior to 2005, strong net inflows were driven in part by a shift from non-managed money, such as bank accounts and term deposits, to managed money, such as mutual funds, said Fabrice Morin, partner in McKinsey’s wealth and asset management practice.

“Some of the high net flows we’ve seen in the past have been driven by shifts to managed assets, and we can’t expect this to last forever,” Morin said. “This low net flows environment, we could be in that environment for a while.”

McKinsey points to four categories where net new flows are heavily concentrated: passive strategies and ETFs, active specialties, multi-asset strategies and alternatives. In fact, 172 percent of net flows went to these four categories in 2013. Alternatives commanded 98 percent of net new revenues in 2013.

Top-quartile firms, which had twice the operating margin and revenue growth of other firms over the last three years, have a greater share of assets in these four categories.

In the U.S., traditional asset classes, such as domestic equity, core fixed income and money markets, accounted for 35 percent of total AUM. But these categories generated negative net flows of 28 percent in the U.S. That trend is expected to continue over the next five years, McKinsey says.

North American asset managers got a nice boost from financial performance, with 2013 pre-tax operating margins rising to 32 percent and profits hitting a record $34 billion, up 18 percent from 2007, the report found.

But at the same time, since 2008, costs have gone up faster than revenues. Across the industry, costs were up 10 percent, or $7 billion, in 2013, with the largest increases in sales and marketing, and operations and technology. In North America, costs grew 29 percent since 2007.

“We’re seeing an environment that requires a lot more compliance, a lot more investments on the side of the asset managers on platforms,” Morin said. “The technology spend is not only driven by compliance, legal and risk. It’s also driven by the fact that the products are complexifying. So multi-asset class products require, in some cases, different platforms, more complex operations.”

Morin said asset managers need to be very thoughtful about where to play in the marketplace. It will be more important for them to shift product development and distribution and marketing activities toward areas that are in demand.