Last week’s investment roller coaster was something we had been expecting—U.S. stocks delivered their usual bout of seasonal volatility right on cue. For now, recent spread widening in high-yield bonds and leveraged bank loans seems to be over, and it also appears that equities have regained their footing after a turbulent week.

With the anticipated seasonal pattern of higher volatility in September and October now largely fulfilled, we anticipate more positive seasonal factors over the next two months. Over the last 68 years, the S&P 500 has averaged monthly gains of 0.9 percent in October, followed by even stronger increases of 1.2 percent in November and 1.8 percent in December.

The current dark cloud that hangs over Europe is a serious threat and something that investors should closely monitor. If the anticipated seasonal strength—which is typically driven by an influx of cash into pension funds that their managers are keen to put to work—is not forthcoming, investors should seriously question how much further the current bull market can run. As of now, we remain cautiously optimistic as we await some crucial economic data.

High-Yield Poised for Rebound?

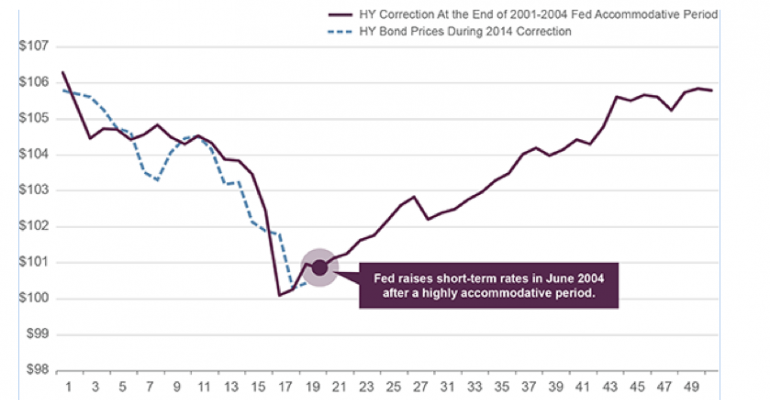

The high-yield sell-off during the third quarter follows the pattern seen in 2004. After the Federal Reserve first signaled a withdrawal of accommodation in 2004, the Credit Suisse High-Yield Index fell in the 20 weeks leading up to the June hike before resuming its bull run through the end of the year. This year, prices fell in the months leading up to the October end of quantitative easing, which marks the start of less accommodative monetary policy. If history repeats itself, high-yield bond prices should rebound in the fourth quarter.

{kind=link}

Source: Credit Suisse. Data as of 10/22/2014. Average price for Credit Suisse High-Yield Index excludes defaults.

This material is distributed for informational purposes only and should not be considered as investing advice or a recommendation of any particular security, strategy or investment product. This article contains opinions of the author but not necessarily those of Guggenheim Partners or its subsidiaries. The author’s opinions are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC. ©2014, Guggenheim Partners. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information.

Scott Minerd is Chairman of Investments and Global Chief Investment Officer at Guggenheim Partners