We expect a limited return environment may persist in 2016 and the year as a whole may look similar to 2015. High valuations, steady economic growth, and the lingering threat of Federal Reserve (Fed) rate hikes may keep pressure on bond prices in 2016. We do not envision a recession developing, which we believe is ultimately needed for a sustained move higher in bond prices.

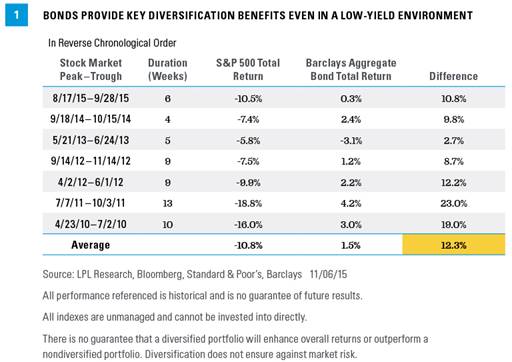

A bond routine should nonetheless be maintained and plays a vital role in suitable investors’ portfolios despite prospects of low returns. Over the past 12 years, high-quality bonds provided a key buffer during periods of stock market weakness. Specifically, high-quality bonds outperformed stocks by more than 13%, on average, when the broad stock market declined by 5% or more over a period of three or more weeks. This relationship has held even during the very low-yield environment of the past five years, when the average yield of the 10-year Treasury was merely 2.5% [Figure 1] and the performance disparity was still a notable 12.3%. While the average absolute return from bonds was low, risk mitigation was still notable.

Planning Ahead

A simple 2016 scenario analysis using existing yields and characteristics of the broad Barclays Aggregate Bond Index shows the potential diversification benefits offered by high-quality bonds [Figure 2]. Even a small 0.25% decline among intermediate Treasury yields may produce a gain of 4.6%, and if interest rates fall further, gains would increase from there.

However, our expectation is that average intermediate-term Treasury yields rise by approximately 0.25% to 0.50%, with a lesser probability of a possible 0.75% increase, as three main challenges facing bonds persist: high valuations, steady economic growth, and the prospect of Fed rate hikes. These three factors, prevalent at the start of 2015, conspired to produce low returns in 2015. All three are expected to continue and are likely to influence the bond market once again in 2016, by exerting upward pressure on bond yields and downward pressure on bond prices. Our interest rate expectations correspond to a range of high-quality bond total returns from a modest loss to a small gain of 1.8%; thus, our “flat” return expectation.

Finding Value in Your Routine

High-yield bonds may be a beneficiary of sticking to a plan. Roiled by a renewed decline in oil prices and overseas growth concerns during the third quarter of 2015, high-yield bond prices weakened as default fears increased. The energy sector was the primary driver of high-yield weakness during the third quarter of 2015, and prices reversed some of what we viewed as an overly severe reaction. As of November 23, 2015, the average yield spread of high-yield bonds was approximately 6.4%, above the historic average of 5.8%, despite low defaults.

Much of the bad news regarding the high-yield energy sector is likely factored into current pricing. Defaults increased in 2015 and are likely to increase further in 2016, but market pricing suggests an overly pessimistic outcome in our view. The implied default rate for the energy sector is a staggering 16% over a one-year time horizon. Although energy issuers have contributed to rising defaults, the current annualized rate of energy-related defaults is 5% and, in our view, is unlikely to reach the high end of market implied expectations.

We continue to find high-quality municipal bonds attractive due to still cheap valuations relative to Treasuries, with most top-quality issuers yielding slightly more than comparable maturity Treasuries. The relative strength of U.S. Treasuries over the second half of 2015 put municipal valuations on more attractive footing. Bear in mind, municipal bonds will take their cues from the Treasury market, but more attractive valuations can provide a buffer against rising interest rates in addition to an attractive level of after-tax yields.

The municipal market is on track to post limited overall debt growth in 2015 but any meaningful increase is unlikely. States and municipalities battle with still tight budgets that will likely keep bond issuance for new infrastructure projects limited. Net supply of the municipal bond market is likely to see only limited growth once again in 2016, which should provide support to prices. However, like taxable bonds, municipal bonds are likely to witness a low-return environment as well and not escape the challenges facing all bond investors in 2016.

Anthony Valeri is an Investment Strategist for LPL Financial

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values and yields will decline as interest rates rise, and bonds are subject to availability and change in price.

Government bonds and Treasury bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

Corporate bonds are considered higher risk than government bonds but normally offer a higher yield and are subject to market, interest rate, and credit risk as well as additional risks based on the quality of issuer coupon rate, price, yield, maturity, and redemption features.

High-yield/junk bonds are not investment-grade securities, involve substantial risks, and generally should be part of the diversified portfolio of sophisticated investors.

Municipal bonds are subject to availability, price, and to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rate rise. Interest income may be subject to the alternative minimum tax. Federally tax-free but other state and local taxes may apply.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Barclays U.S. Aggregate Bond Index is a broad-based flagship benchmark that measures the investment-grade, U.S. dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS, and CMBS (agency and non-agency).