By Katie Linsell

(Bloomberg) --In the corporate-bond market, even a few billion doesn’t get you a seat at the table.

And Najib Nakad is so tired of settling for the scraps left by giants, he hardly bothers to bid for new issues anymore.

“We are too small to have any hope of an allocation,” said Nakad, who helps oversee about 2 billion euros ($2.5 billion) as chief portfolio manager at Hof Hoorneman Bankiers in the picturesque Dutch town of Gouda. “It just goes to the big guys."

Investors like Nakad, 52, who have complained for decades about going up against the bankers that put bond deals together may finally be getting some relief.

Digital disruption, which has changed the face of trading equities, currencies and some government debt, is arriving at one of the last bastions of resistance: the syndicate desk, where corporate bonds are priced and distributed. Selling new issues is a linchpin of investment banks’ profitability. Bond arranging generated about $14 billion for the eight largest banks in the first three quarters of 2017, more than double the haul from equity underwriting, according to data compiled by Bloomberg Intelligence.

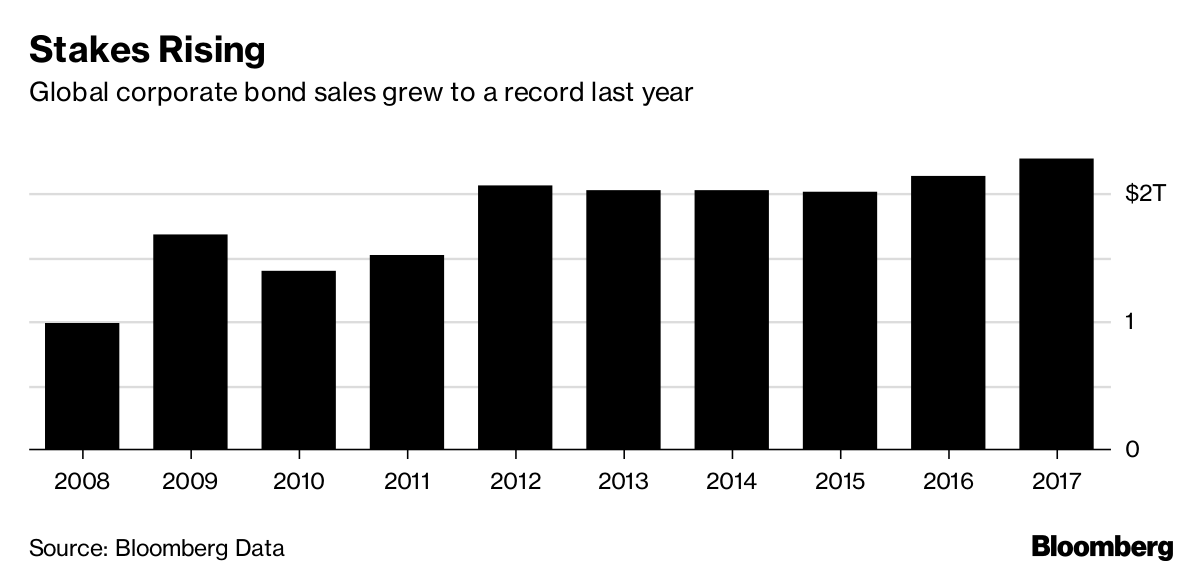

The stakes have soared after a binge that saw companies sell an unprecedented $18 trillion of bonds since 2008, in the aftermath of the crisis that drove benchmark borrowing costs to zero.

Europe is proving particularly fertile ground for digital primary markets because there’s more competition among banks, and electronic trading is more popular than in the U.S. Regulators are paying attention too: Starting this month, syndicate bankers must justify at least the top 20 percent of allocations for regulators under Europe’s revised rulebook known as the Markets in Financial Instruments Directive.

And wherever you are, whether you’re a borrower or a lender, a salesman or a syndicate banker, your world is facing upheaval, with the human factor becoming less significant. Whether it succumbs is another matter, particularly since some of the biggest arrangers have yet to go all in.

If this sounds familiar, it’s because it is. More than a decade ago, at the height of the dot-com boom, the market for initial public offerings was exposed as a den of conflicts and profiteering that was due for change. And while Spotify, owner of the world’s largest paid music service, is planning to go public via a direct listing, the market hasn’t really changed all that much.

“The underwriters have discretion to allocate shares and it’s also true in bonds,” said Jay Ritter, a professor at the University of Florida’s business school who has been covering the IPO market for more than three decades. “That discretion can be used for good or bad.”

New Platforms

The digital platforms still account for just a fraction of orders in the new issue market and they’re mainly in the business of facilitating communications. But advocates and specialists say their growth is unstoppable. Here are a few of the new entrants to the market:

Ipreo, a technology provider jointly owned by a unit of Goldman Sachs Group Inc. and Blackstone Group LP, started allowing investors to directly post their bond orders to banks electronically last year in a system called Investor Access.

Neptune Networks, which is owned by 19 banks and publishes trading levels to subscribers, has been asked by investors and lenders to create a system for new issues. No decision has been taken yet, according to Chief Executive Officer Grant Wilson. There’s also Overbond, a Toronto-based origination and execution platform that connects investors and companies for bond sales. Another system, Origin, makes it easier for banks to find issuers starting with Europe’s 300 billion-euro market for private placements known as medium-term notes.

Ipreo, Neptune, Overbond and Origin said their approaches are collaborative, evolving and constructive. Bloomberg LP, the parent of Bloomberg News, provides services that facilitate bond ordering and distributes information on new debt offerings.

Minnows vs. Whales

Ipreo keeps a record of investors’ bids for bonds and the allocations they receive. That could help regulators investigate whether bonds are fairly disseminated, Andrew Falco, head of fixed income trading at $324 billion firm Fidelity International, said at a conference in Amsterdam in November.

That kind of transparency could handicap the giants that hold sway in the corporate bond market.

When Verizon Communications Inc. sold a record $49 billion of bonds in 2013 via Barclays Plc, Bank of America Corp., JPMorgan Chase & Co. and Morgan Stanley, more than 15 percent of the eight-part offering went to Pacific Investment Management Co. while BlackRock Inc. came away with about 10 percent. After the deal, the U.S. Securities and Exchange Commission launched an investigation into whether Wall Street banks give certain clients preferential treatment in bond sales.

Spokeswomen for Pimco and BlackRock declined to comment on the bond allocations the firms receive.

Getting allocations at the point of sale can make the difference between a good year or a bad one for a money manager.

You also don’t want to be the fund that’s lumbered with a dud. Take Adidas AG: when the sporting-goods maker last sold bonds in 2014, small investors were left on the hook because there wasn’t enough interest from bigger firms, according to Anthony Peters, a strategist who has observed the market for more than 30 years. The notes slid about two cents on the euro in initial trading.

Salespeople

Some of the digital systems threaten to take over salespeople’s most time-consuming tasks: informing investors of upcoming offerings, taking their orders and telling them their allocations.

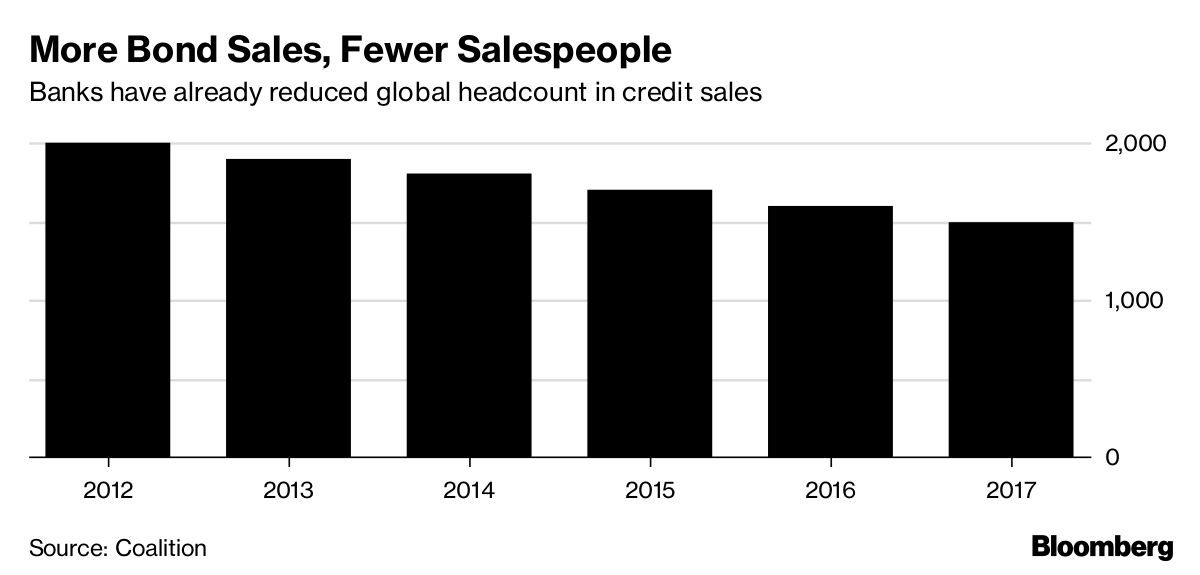

By performing the most mundane jobs, digitization could free up people for more complex tasks like discussing trading strategies, advocates say. It could also mean job cuts for cost-conscious employers. The 12 largest investment banks already reduced their global credit salesforce by 25 percent in about five years through mid-2017 to 1,500 people, according to analytics provider Coalition Development Ltd.

“Why have a sales guy if you can just order bonds directly on a new issue?” said Tim Hall, global head of debt capital markets at Credit Agricole SA for nine years until 2016.

Treasurers

Corporate borrowers are already innovating to cut costs. Some are using blockchain technology to sell a cross between bonds and loans known as Schuldschein. And while some still depend on banks’ for their advice and extra services, others want to cut down on fees by using electronic auctions instead of syndicating notes.

Auctions are regularly used in the government bond market, especially so-called Dutch auctions where investors submit orders to buy through primary dealers and the borrower’s treasury team fills orders starting with the highest prices first. The borrower doesn’t generally pay any bank fees.

Syndicate Desks

The largest bond arrangers have the most to lose if frequent borrowers increasingly opt for electronic auctions, shrinking the role of the syndicate managers—described in Michael Lewis’s “Liar’s Poker” as “omniscient, omnipotent, omnivorous”.

“We are keeping a wary eye on what this could mean for revenue generation going forward,” Marc Tempelman, former vice chairman of Global Capital Markets at Bank of America said at a conference in Luxembourg last year.

That may be why, at least in the case of Ipreo’s Investor Access, some key banks haven’t signed up, including Bank of America, Barclays, Citigroup Inc., Credit Suisse Group AG, Deutsche Bank AG, JPMorgan and Morgan Stanley, according to people familiar with the matter. Spokespeople from these banks declined to comment on their participation.

“There is a risk of disintermediation in new issues and it’s something that the banking industry needs to be conscious of,” said Armin Peter, global head of debt syndicate at UBS Group AG in London. “There must be a certain fear of automation.”

--With assistance from Alison Williams, Tom Beardsworth, Stephen Spratt, Viren Vaghela, Patricia Suzara and Matt Robinson.To contact the author of this story: Katie Linsell in London at [email protected] To contact the editor responsible for this story: Abigail Moses at [email protected] James Hertling