If you haven’t done a check-up on your clients’ retirement health care costs lately, it’s a good time to update the numbers. Medicare’s premiums and out-of-pocket costs will jump over the next several years due to rising health care costs and changes in the program made by Congress.

After several years of minimal health care inflation, higher costs started showing up in the 2015 data. The projected health care expense in retirement for a married couple with median drug expenses jumped 7.5 percent to $158,000 in 2015 from 2014, according to the Employee Benefit Research Institute (EBRI).

Paul Fronstin, director of EBRI’s health research and education program, cautions planners against relying on the median figures, however. “If you plan to the median you have a 99 percent chance of being wrong,” he says. “Half of us will live longer and half won’t make it to average —so then the question is, how wrong are you?”

To be 90 percent sure, a married couple would need $259,000 in lifetime retirement expenses. A couple with high drug expenses (the 90th percentile) would need $392,000, up 20 percent from last year. (EBRI’s figures include premiums for Medicare Parts B and D and Medigap, plus out-of-pocket drug expenses.)

Here’s a breakdown of the underlying trends driving those numbers.

Part B

Monthly premiums for Medicare Part B, which covers outpatient services, have been flat at $104.90 for the past three years. But premiums are projected to rise roughly 6 percent annually for the near term, according to HealthView Services, a company that develops health care cost-projection software.

The impact of higher Part B premiums on clients will vary, depending on their Social Security filing status and income. For anyone receiving Social Security benefits, an increase in the Part B premium is calibrated with Social Security’s cost-of-living adjustment (COLA). Their Part B premium can’t be increased beyond a point that would yield a net reduction in Social Security benefits—the so-called “hold harmless” rule.

That rule created a chaotic situation this year after it became clear that no Social Security COLA was awarded due to the economy’s low inflation—and that Part B premiums would be jumping. Seventy percent of Medicare beneficiaries fall into the “hold harmless” group, so the remaining 30 percent will carry the burden of the higher premiums—and the math here is especially unfavorable: By law, enrollees shoulder 25 percent of total projected Part B program costs. In a year where Social Security beneficiaries are held harmless, the entire increase is billed to the remaining Medicare population. Initially, it appeared that 70 percent of enrollees would pay $104.90 next year, with the remainder shouldering a whopping 52 percent increase, to $159.30.

Congress alleviated some of the pain by reducing that number to just 15 percent, or $120.70, plus a $3 monthly surcharge, as part of the budget agreement passed in

late October.

Who is in this vulnerable group?

- Anyone who is delaying their filing for Social Security benefits.

- Federal retirees who participated solely in the older Civil Service Retirement System and therefore don’t receive Social Security benefits.

- State government workers, most of whom participate in defined-benefit pension plans and are not covered by Social Security during their tenure as state employees.

- Low-income “dual-eligible” seniors who receive Social Security and also participate in both Medicare and state-run Medicaid programs. Their premiums are absorbed by state Medicaid budgets.

- Anyone enrolling in Medicare for the first time next year.

- Higher-income beneficiaries already subject to an income-adjusted Part B premium.

Prescription Drug Prices

Volatility in Part B premiums should settle down next year, assuming more normal inflation. But prescription drug plan (PDP) costs are on a longer-range upward march. HealthView projects 8 percent annual compounded increases over the near term.

For 2016, PDP costs will rise at the fastest clip in five years, driven mainly by the rising use and cost of specialized drugs designed to fight catastrophic illnesses.

Medicare officials said in July that the average premium for a basic Medicare Part D prescription-drug plan next year would hold steady at $32.50 per month. But the 10 most popular plans—which include basic plans and those offering enhanced coverage—will see premiums rise an average of 8 percent next year, according to Avalere Health, a consulting and research firm. Five of the most popular plans will see double-digit increases. That’s a big change from recent years; average premiums for the top 10 have been flat or down a bit in each of the past four years. The average PDP premium in 2016 will be more than $40 for the first time in the program’s history.

In fact, the projections are higher than the growth in Part B or Part A (for hospitalization costs), says Juliette Cubanski, associate director of the Program on Medicare Policy at the Kaiser Family Foundation.

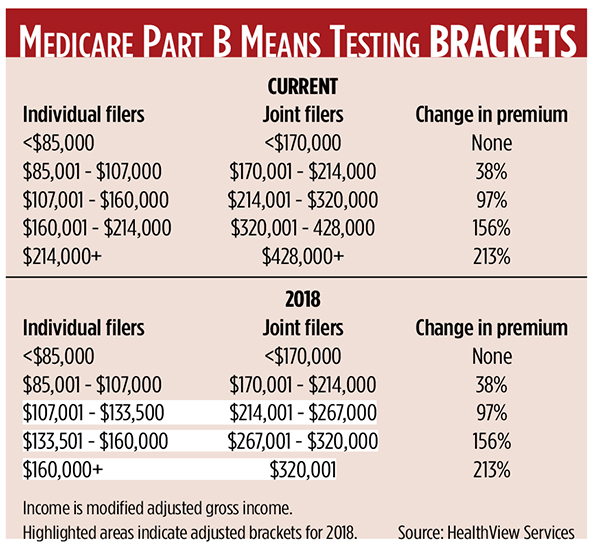

High-Income Surcharge Bracket Revisions

As noted above, high-income seniors are among the groups not protected under the COLA “hold harmless” provision. That means their already-higher Part B premiums will also rise 15 percent in 2016. Enrollees in the initial income threshold $85,000 modified adjusted gross income (MAGI) for an individual tax return and $170,000 for a joint return) will pay $169 monthly, compared with $146 this year. In the highest income bracket, the monthly premium will jump to $386 from $335.70 this year.

Longer-range high-income surcharges will undergo a structural change that will also increase costs. This results from the “doc fix” signed into law earlier this year, which resolved a long-standing problem with Medicare payment rates to physicians.

The law boosts payments to doctors, and pays for it—in part—by tapping high-income seniors.

Starting in 2018, the Part B premium surcharges shift in a way that will add a higher percentage of costs to Medicare beneficiaries with a MAGI between $133,500 and $214,000 (twice that for couples). Those with an income of $133,000 to $160,000 would pay 65 percent of total premium costs, rather than 50 percent today, and those with an income between $160,000 and $214,000 would pay 80 percent, rather than today’s 65 percent. (See chart.)

More seniors with relatively high MAGIs will be pulled into surcharge territory in coming years. The Affordable Care Act freezes inflation adjustments to the income brackets through 2020. The Kaiser Family Foundation estimates that the share of Medicare beneficiaries paying the surcharges will rise from 5 percent in 2013 to 9.6 percent in 2019 and will then fall back a bit as inflation adjustments resume.

Medigap First-Dollar Coverage

The “doc fix” legislation also revises the Medigap policies that many seniors purchase as supplemental coverage to their traditional Medicare benefit.

Starting in 2020, supplemental Medigap plans will no longer cover the annual Part B deductible for new enrollees. That will mean changes for Medigap C and F plans, the two most popular choices and the only ones that cover Part B deductibles.

The goal is to give seniors more “skin in the game,” which conservatives have long argued would lower costs by making patients think twice about using medical services if they know they must pay something for all services they use.

It’s debatable whether this is wise policy. A new study finds that people who pay higher deductibles simply use less health care and don’t always make the best decisions about when to see the doctor.

Ron Mastrogiovanni, HealthView’s president and CEO, expects further changes in first-dollar coverage over the next couple of years. “Statistics show that pre-retirees with high-deductible policies and retirees who are not covered by a comprehensive supplemental plan utilize the system less than those with comprehensive coverage,” he says. “Short term, that would help Medicare finances, but who knows what the long-term impact would be on the system.”

Cubanski notes that premiums on the affected Medigap plans should decline to reflect the decreased coverage. “Since the cost-benefit is changing, the premiums should come down a bit, but we’ll have to wait and see,” she says.