More writedowns on the way.

Since the ending of the credit bubble in the summer 2007, the major brokerage firms and banks have been dealing with the accounting aftermath. To minimize (or hide) the damage they did to their own balance sheets, these firms have been using “Level 3” accounting standards — a GAAP-approved method (Generally Accepted Accounting Principles) to account for hard-to-value assets. Level 3 assets are essentially assets for which no market price exists, and, therefore, are valued at whatever level the financial institution deems most reflective of underlying value.

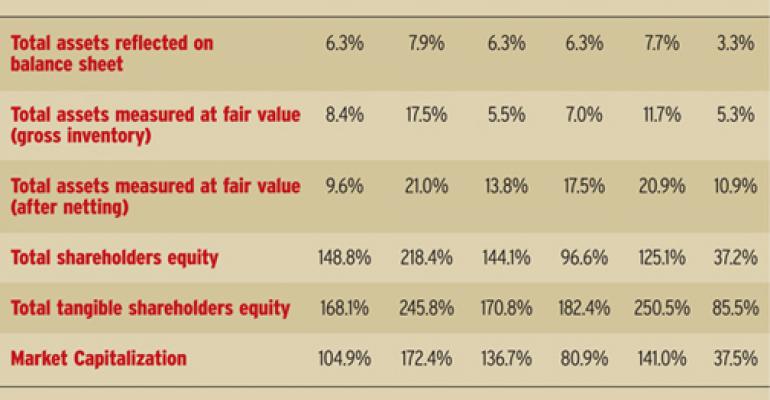

Table 1 lists the gross (un-hedged) exposure of these firms to these assets before recent capital infusions. The best way to look at this is to consider the hit these firms would take to total value if these assets are marked down. For example, looking at Citigroup's exposure makes it clear why the regulators felt the need to step in.

Again, Level 3 essentially allows banks to mark illiquid assets at whatever price they want. As the accompanying chart indicates, these marks make up a large percentage of the net value of financial firms listed below, ranging from 85 percent of tangible equity at Bank of America to approximately 250 percent of tangible equity at Morgan Stanley and Citigroup. In other words, most of our nation's-largest financial institutions would be insolvent if they were forced to write these assets to zero.

That is an unlikely scenario, but even much smaller writedowns would wreak havoc on both the balance sheets of these firms and the financial markets at large. When and how this situation resolves itself is unclear (TARP or no TARP), but advisors and their clients should brace themselves for further writedowns of unknown size at some future date. It won't be pretty.