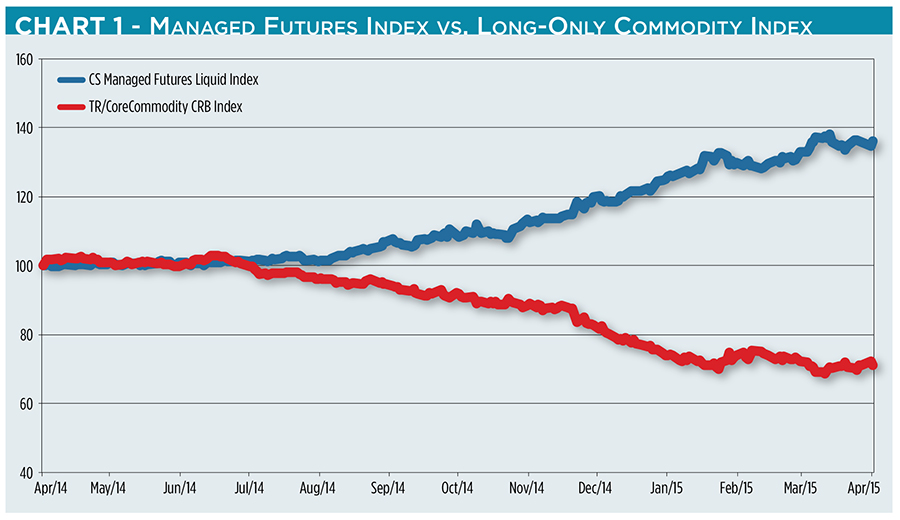

Take a look at Chart 1. Does it make you think of anything? How about baseball? Recall the words of Yankee great and master of malaprops Yogi Berra: “When you come to a fork in the road, take it.” Looking at the fork here, Yogi could very well have been proffering advice to futures fund investors this year.

The chart contrasts the 12-month performance of two different futures investing strategies: active management versus long-only buy-and-hold.

{kind=link}

Investors taking the managed futures fork are a much happier lot than those opting for passive strategies. Why? The price of crude oil, a hefty component of most commodity futures benchmarks, has been nearly halved since last year’s Independence Day. Agricultural futures, heavily represented in the equal-weighted Thomson Reuters/CoreCommodity CRB Index, are down nearly 20 percent. Futures funds unconstrained by long-only mandates were free to short the oil and ag markets; funds tracking indexes like the CRB were obliged to be bulls all the way down.

No surprise, then, that managed futures (the actively managed futures portfolios) top this year’s list of hedge fund strategies. The Credit Suisse Managed Futures Liquid Index is up 11 percent through the first week in April, beating long/short, event-driven, global macro and merger arbitrage strategies by substantial margins.

The Credit Suisse benchmark isn’t a composite of actual hedge fund returns. Instead, it’s a volatility-controlled, momentum-following strategy utilizing the most liquid derivatives and securities in the equities, fixed income, commodities and currency markets. In other words, the index performs like a hypothetical fund manager hewing to a strictly defined—and transparent—strategy.

In the real world of managed futures, fund runners have more latitude in strategy selection and risk management. Their tactics tend to be opaque. But we can gain a little insight by applying some key performance metrics.

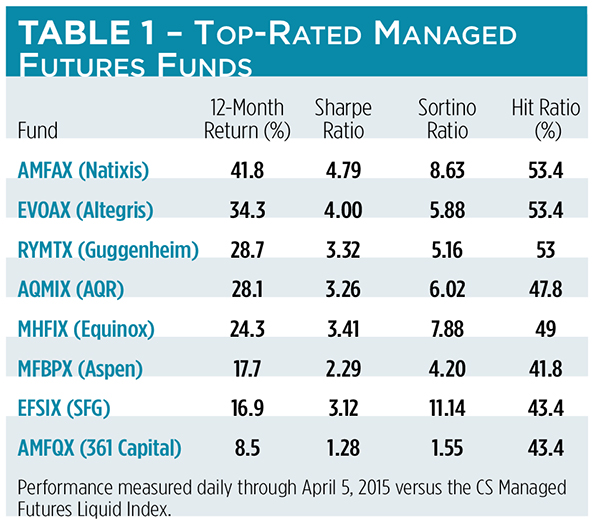

First, let’s look at total returns. Among Morningstar’s 4- and 5-star mutual funds, only one, the Natixis ASG Managed Futures Strategy Fund (OTC: AMFAX) has outdone the Credit Suisse index over the past 12 months. That’s not to say the other funds didn’t offer handsome profits to their customers. After all, the nine-fund universe (see Table 1) gained an average 29 percent on an asset-weighted basis. It’s just that the Credit Suisse bogey was 36 percent.

No Returns Without Risk

AMFAX managers pursue an absolute return strategy while seeking to add value through volatility management. The fund runners use proprietary quantitative models to identify price trends, looking for momentum plays. Stylistically, then, the fund is very much like the Credit Suisse benchmark. Similar in style, yes, but better in execution.

Returns don’t come without risk. A fund may outdo its benchmark for a given period, but at what cost? The risk undertaken to produce outsized gains could, in a subsequent time period, generate crippling losses. Measures of risk-adjusted return tell investors if they’re making deals with devils. The Sharpe ratio, for example, measures how many units of reward are earned for each unit of risk undertaken. In this metric, risk is defined as the standard deviation of returns, or volatility. A Sharpe ratio of “1” indicates a good payback for the risk assumed; a reading of “2” is better. Outstanding performance would be signaled by a ratio of “3” or better.

AMFAX’s Sharpe ratio, at 4.79, handily outdoes the Credit Suisse benchmark’s 3.63 reading. But, as you can see in the table, the Natixis fund wasn’t the only portfolio with a superior risk-adjusted return. The Altegris Futures Evolution Strategy Fund (OTC: EVOAX) chalked up an index-beating “4” on the Sharpe meter. EVOAX utilizes a multimanager approach, concentrating on trend-followers, balanced by an allocation to a fixed income strategy.

Both the Natixis and Altegris funds use fixed income allocations to enhance returns and, most especially, to dampen portfolio volatility. Fund managers are often thought to have a love-hate relationship with volatility. Truth be told, they love volatility. They love upside volatility. Investors do too. Judging a fund on a metric utilizing standard deviation, which considers all volatility as a detriment, may not credit a manager for taking the right kind of risk.

{kind=link}

The Sortino ratio essentially gauges returns on the basis of downside risk avoidance. Like the Sharpe ratio, a higher reading denotes better performance. When fund returns are normally distributed—that is, on a bell-shaped curve—the Sharpe and Sortino ratios will be closely aligned. Skewed returns cause the ratios to diverge.

The Path to Alpha

The Credit Suisse benchmark boasts a 5.34 Sortino ratio over the last 12 months. Five of Morningstar’s top-rated funds bettered the index, indicating some robust risk management systems at work. Most notable, though, is the 11.14 value for the Solutions Fund Group Futures Strategy Fund (OTC: EFSIX), an example of risk management overkill. The fund’s strict absolute return mandate kept its Sortino ratio high but its total return relatively low.

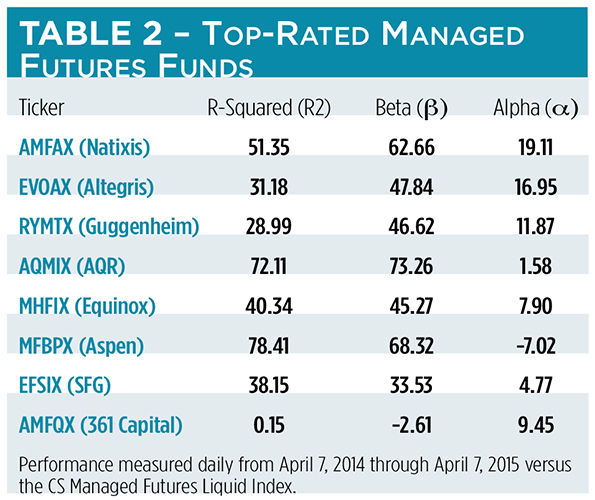

The 361 Capital Managed Futures Strategy Fund (OTC: AMFQX) earned the lowest Sortino quotient, as well as the lowest Sharpe ratio and total return. These results stem from the fund’s unique investment strategy. AMFQX invests solely in U.S. stock index futures, so turnover is light. The fund’s beta, in fact, is negative versus the Credit Suisse benchmark—a characteristic exhibited by no other fund in the universe. (See Table 2.) Another distinction: AMFQX follows a countertrend, rather than a trend-following, algorithm. And once a trade is signaled, fund managers go all in. The fund is always 100 percent invested—long, short or in cash—at any given point.

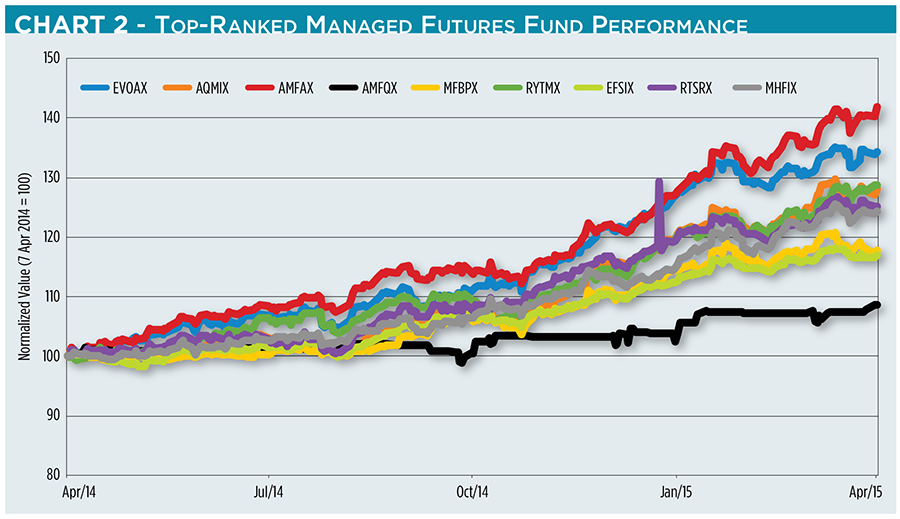

Three of the best-performing portfolios earned hit ratios—a very granular measure of outperformance—in excess of 50 percent. The ratio represents the percentage of days in which each fund beat the Credit Suisse benchmark. The path to alpha is most often paved with a high hit ratio. Alpha, the pot of gold at the end of a fund-runner’s rainbow, measures a portfolio’s risk-adjusted performance relative to its benchmark.

The lowest hit ratio is owned by the Aspen Managed Futures Strategy Fund (OTC: MFBPX) which, predictably, earned negative alpha over the last 12 months. Clues to the fund’s performance are found in its high R-squared and beta coefficients. Beta tracks a fund’s volatility versus the benchmark, while R-squared denotes the degree to which fund price movements are explained by wobbles in the index.

The Aspen portfolio itself tracks an eponymous benchmark—the Aspen Managed Futures Beta Index—that aims to replicate the performance of a broad universe of commodity trading advisors. Even factoring in the MFBPX expense ratio and tracking error, we can glean that the Credit Suisse index is a more aggressive construct.

Oddly enough, Yogi Berra wouldn’t opine on the performance of these funds or the odds of persistence. We’re left to speculate if the Natixis portfolio will top the table next season, or if the 361 Capital fund will start belting homers. Perhaps it’s best that we just remember what Yogi said about prognostication: “The future ain’t what it used to be.”