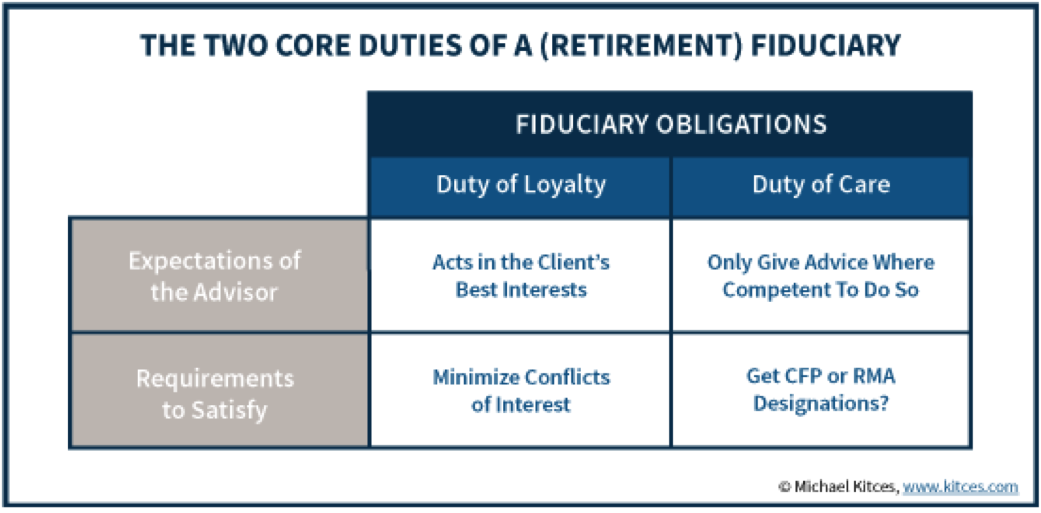

In the wrangling over the fiduciary rule, regulators and financial institutions have overwhelmingly focused on the duty of loyalty, which requires advisors give non-conflicted advice. But the duty of loyalty represents only half the equation. To truly protect investors, the fiduciary rule needs to address the duty of care.

The duty of care requires advisors to exercise an appropriate level of skill and diligence. Without the duty of care, the duty of loyalty is nearly worthless. An advisor who tries to act in your best interest, but doesn’t have the skill or diligence to do so, can cause just as much harm as a conflicted advisor.

Despite this fact, there’s almost no evidence of significant resources invested in the enforcement—or even the definition—of the duty of care by regulators. A few thought leaders have stepped into the void, but without more guidance, it’s hard to know where the goal posts will be.

Duty of Care: Too Big to Fulfill?

Michael Kitces weighed in on the potentially devastating class-action lawsuit risks faced by financial institutions if they do not fully address the duty of care back in January. “Financial institutions could face a class-action lawsuit … for systemically breaching the fiduciary duty of care by not sufficiently training their advisors,” he wrote.

On the heels of that article, our open letter to the DOL specifically asked for guidance on how to fulfill the duty of care in its third FAQ on the ruling. Neither that FAQ, nor the one released last week, addressed the duty of care.

This ambiguity creates a big question mark for firms that want to protect themselves from liability. Kitces proposes one potential solution: Requiring all advisors to get CFP or RMA designations.

Currently, only about 20 percent of all financial advisors have a CFP. Credentialing the other 80 percent would represent an enormous amount of time and effort, especially since only about 60 percent of those who sit for the CFP exam pass. The choice between undertaking this massive effort or being exposed to potentially devastating class-action lawsuits is a horrible one for any financial institution.

No Answer Is the Worst Answer

Given this conundrum, you’d imagine that regulators would want to provide clarity for institutions and advisors. Instead, the DOL has been vague in its comments about the duty of care. The only recent reference we found is in the first FAQ, where it cites the prudent-man standard, which states that a fiduciary will act:

“…with the care, skill, prudence, and diligence under the circumstances then prevailing that a prudent man acting in a like capacity and familiar with such matters would use in the conduct of an enterprise of a like character and with like aims.”

This hypothetical “prudent man” represents an impossibly vague standard for advisors and investors. Cases such as GIW Industries, Inc., v Trevor, Stewart, Burton, & Jacobsen Inc. and Donovan v. Mazzola have brought a little clarity to the concept, but much ambiguity remains.

We are not sure why the DOL, and now the SEC, have not provided more guidance on how they will regulate and enforce the duty of care. Perhaps regulators and industry players see fulfillment of the rule as too big a problem to solve at this time. Perhaps the status quo feels more secure. After all, if almost no one is fulfilling the duty of care, then maybe no one has to.

That sort of thinking is understandable in the face of the potentially enormous, if not impractical, task of getting official designations like the CFP or RMA for all financial advisors who need to meet a fiduciary standard of care.

It’s also understandable that firms might turn a blind eye toward the duty of care based on hope that a repeal or weakening of the fiduciary rule will insulate them from responsibility to fulfill it. While a regulatory rollback of this sort is possible, it does not absolve financial institutions from having to prove to discerning constituents that they have the competency to provide a fiduciary level of service.

As we wrote in “Fiduciary Rule Delayed, but Its Impact Remains,” the debate around the fiduciary rule has already transformed the industry. Clients now want to know if their advisor provides a fiduciary level of service. Firms that can’t prove they can fulfill the duty of care will lose clients to those that can.

Making the Problem Smaller

Given the logistical and cost challenges of credentialing tens of thousands of advisors, we propose another approach for financial institutions to fulfill the duty of care. Our approach is vastly less expensive in terms of logistics and implementation. Rather than trying to accredit the advisors, we propose giving them research that enables them to fulfill the duty of care.

This research would probably be necessary even if every advisor earned a CFP or RMA. As Kitces wrote in his post, “It’s the combination of competency education, and a prudence process, that is necessary for an advisor to substantiate that he or she actually met the fiduciary duty of care.” In other words, even if you have all the credentials in the world, you still need research to make informed investment decisions.

Research that fulfills the duty of care is not that hard to define. We think it is self-evident that research with the following qualities would equip an advisor to provide prudent advice:

- Comprehensive. It should reflect all relevant publicly available information (i.e. all 10-Ks and 10-Qs), including the footnotes and MD&A.

- Objective. Investors deserve unbiased research.

- Transparent. Investors should be able to see how the analysis was performed and the data behind it.

- Relevant. There must be a tangible, quantifiable connection to investment performance.

The average client would probably be surprised to learn that these criteria are not required for investment research.

Research of this quality may not have been possible at scale in the past, but today’s technology makes it possible. Machine learning and natural language processing allow computers to do the heavy lifting of reading financial filings and analyzing data on the back end, freeing up human advisors to focus on their client’s individual needs.

In another recent Nerd’s Eye View post, "What Cyborg Chess Can Teach Us About the Future of Financial Planning," Derek Tharp posits that the best advisors in the future will be those who are the best at leveraging technology. That idea certainly applies to the human advisors working with robo-analysts. The robo-analysts’ research makes advisors more effective than either a standalone human or a robo advisor, in the same way that a human chess player aided by a machine is better than either one on its own.

What Should a Prudent Man or Institution Do?

More thought leaders are beginning to turn attention to the duty of loyalty. MarketWatch’s retirement columnist, Robert Powell, recently echoed the concern over the lack of attention to the duty of care. He highlights Jeffrey Levine’s suggestion that financial institutions undertake a team-oriented approach to advice to ensure they have access to the different pockets of expertise needed to provide truly comprehensive advice.

However, until we get more guidance from regulators, we cannot be sure of the expertise needed to fulfill the duty of care.

We agree and also believe that technology is key to the practical and cost-effective fulfillment of the duty of care. More of the biggest names in the financial industry (see "At BlackRock, Machines Are Rising Over Managers to Pick Stocks") are now embracing technology to leverage machines in the investment-research process. Technology may be the only solution to the dual mandate for financial institutions: cut costs and fulfill the fiduciary duty of care.

Providing research as described above to advisors rather than undertaking a massive training effort is more cost-effective in the short term and better for investors in the long term. Regardless of one’s level of training, high-quality research is necessary for really fulfilling fiduciary duties. It is only natural that we leverage technology to support human efforts in this area, just as we have in so many other parts of modern society.

Regulators can aid this transition by providing clarity to everyone involved on how to fulfill the duty of care. Investors, clients, advisors and analysts deserve the latest in technology to get the diligence required to make prudent investment decisions.

David Trainer is the founder and president of New Constructs, an independent investment-research firm.