It seems the bond market is telling us something but if you want to hear it you’ll need to bend your ear toward the junk bond spread.

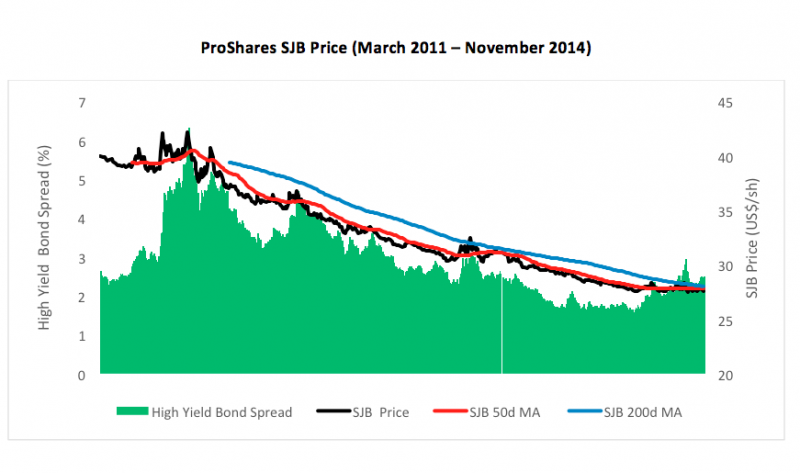

High yield, or junk, bonds are the canaries in our economic coal mine. Often, changes in the spread between junk bond and ten-year Treasury yields prefigure gyrations in the equity market. And, with just a glance at the price action in the ProShares Short High Yield ETF (NYSE Arca: SJB), you can essentially track and trade the spread.

{kind=link}

SJB aims to deliver the unlevered inverse (-1x) of the daily performance of the Markit iBoxx $ Liquid High Yield Index. Simply put, buying the ProShares fund is a bet against junk bonds.

Since its launch in 2011, SJB has virtually mirrored the high yield spread. As you can see in the chart above, the spread and the ETF’s price have been on an uninterrupted slide for the past three years. That is, till now.

Now there’s bottoming action in SJB and in the spread. SJB has bounced off the $27.50 level a number of times and, as of Monday, finally broke above its 50- and 200-day moving averages for the first time. The yield spread, meantime, has backed up 20 basis points.

So, what’s all this mean? A couple of things come to mind.

Junk behaves more like stocks than bonds, mostly due to the debt’s low claim priority on earnings and liquidation proceeds – just above that of common equity in most cases. The junk and equities markets are normally well correlated, though wobbles on the debt side often act as “tells” to behind-the-scenes troubles, giving bond watchers a bit of an edge.

The yield spread widens as the risk of default rises as typically occurs when when the economy is in trouble. Back in December 2008, for example, the spread ballooned to nearly 14 percent. And we all know what happened to stocks back then.

We’re obviously nowhere near 2008 levels. The yield spread’s now just north of two percent. But conditions can change in short order. Presently, the spread’s at the same level as it was in mid-July 2007. Forty trading days later, the spread had climbed 124 basis points, or 54 percent. And the stock market? In that same time the S&P 500 dipped six percent.

Brad Zigler is former head of marketing and research for the Pacific Exchange's (now NYSE Arca) option market and the iShares complex of exchange traded funds.